#include <optionletstripper1.hpp>

Inheritance diagram for OptionletStripper1:

Inheritance diagram for OptionletStripper1: Collaboration diagram for OptionletStripper1:

Collaboration diagram for OptionletStripper1:

Public Member Functions | |

| OptionletStripper1 (const ext::shared_ptr< CapFloorTermVolSurface > &, const ext::shared_ptr< IborIndex > &index, Rate switchStrikes=Null< Rate >(), Real accuracy=1.0e-6, Natural maxIter=100, const Handle< YieldTermStructure > &discount={}, VolatilityType type=ShiftedLognormal, Real displacement=0.0, bool dontThrow=false) | |

| const Matrix & | capFloorPrices () const |

| const Matrix & | capletVols () const |

| const Matrix & | capFloorVolatilities () const |

| const Matrix & | optionletPrices () const |

| Rate | switchStrike () const |

| Public Member Functions inherited from OptionletStripper | |

| const std::vector< Rate > & | optionletStrikes (Size i) const override |

| const std::vector< Volatility > & | optionletVolatilities (Size i) const override |

| const std::vector< Date > & | optionletFixingDates () const override |

| const std::vector< Time > & | optionletFixingTimes () const override |

| Size | optionletMaturities () const override |

| const std::vector< Rate > & | atmOptionletRates () const override |

| DayCounter | dayCounter () const override |

| Calendar | calendar () const override |

| Natural | settlementDays () const override |

| BusinessDayConvention | businessDayConvention () const override |

| const std::vector< Period > & | optionletFixingTenors () const |

| const std::vector< Date > & | optionletPaymentDates () const |

| const std::vector< Time > & | optionletAccrualPeriods () const |

| ext::shared_ptr< CapFloorTermVolSurface > | termVolSurface () const |

| ext::shared_ptr< IborIndex > | iborIndex () const |

| Real | displacement () const override |

| VolatilityType | volatilityType () const override |

| virtual const std::vector< Rate > & | optionletStrikes (Size i) const =0 |

| virtual const std::vector< Volatility > & | optionletVolatilities (Size i) const =0 |

| virtual const std::vector< Date > & | optionletFixingDates () const =0 |

| virtual const std::vector< Time > & | optionletFixingTimes () const =0 |

| virtual Size | optionletMaturities () const =0 |

| virtual const std::vector< Rate > & | atmOptionletRates () const =0 |

| virtual DayCounter | dayCounter () const =0 |

| virtual Calendar | calendar () const =0 |

| virtual Natural | settlementDays () const =0 |

| virtual BusinessDayConvention | businessDayConvention () const =0 |

| virtual VolatilityType | volatilityType () const =0 |

| virtual Real | displacement () const =0 |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

LazyObject interface | |

| Matrix | capFloorPrices_ |

| Matrix | optionletPrices_ |

| Matrix | capFloorVols_ |

| Matrix | optionletStDevs_ |

| Matrix | capletVols_ |

| bool | floatingSwitchStrike_ |

| Rate | switchStrike_ |

| Real | accuracy_ |

| Natural | maxIter_ |

| bool | dontThrow_ |

| void | performCalculations () const override |

Detailed Description

Helper class to strip optionlet (i.e. caplet/floorlet) volatilities (a.k.a. forward-forward volatilities) from the (cap/floor) term volatilities of a CapFloorTermVolSurface.

Definition at line 44 of file optionletstripper1.hpp.

Constructor & Destructor Documentation

◆ OptionletStripper1()

| OptionletStripper1 | ( | const ext::shared_ptr< CapFloorTermVolSurface > & | termVolSurface, |

| const ext::shared_ptr< IborIndex > & | index, | ||

| Rate | switchStrikes = Null<Rate>(), |

||

| Real | accuracy = 1.0e-6, |

||

| Natural | maxIter = 100, |

||

| const Handle< YieldTermStructure > & | discount = {}, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| Real | displacement = 0.0, |

||

| bool | dontThrow = false |

||

| ) |

Definition at line 37 of file optionletstripper1.cpp.

Member Function Documentation

◆ capFloorPrices()

| const Matrix & capFloorPrices | ( | ) | const |

◆ capletVols()

| const Matrix & capletVols | ( | ) | const |

◆ capFloorVolatilities()

| const Matrix & capFloorVolatilities | ( | ) | const |

◆ optionletPrices()

| const Matrix & optionletPrices | ( | ) | const |

◆ switchStrike()

| Rate switchStrike | ( | ) | const |

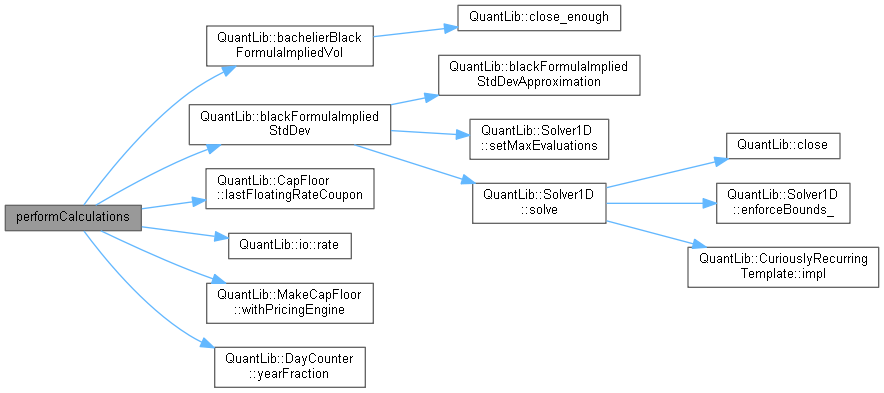

◆ performCalculations()

|

overridevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Implements LazyObject.

Definition at line 60 of file optionletstripper1.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ capFloorPrices_

|

mutableprivate |

Definition at line 68 of file optionletstripper1.hpp.

◆ optionletPrices_

|

private |

Definition at line 68 of file optionletstripper1.hpp.

◆ capFloorVols_

|

mutableprivate |

Definition at line 69 of file optionletstripper1.hpp.

◆ optionletStDevs_

|

mutableprivate |

Definition at line 70 of file optionletstripper1.hpp.

◆ capletVols_

|

private |

Definition at line 70 of file optionletstripper1.hpp.

◆ floatingSwitchStrike_

|

private |

Definition at line 72 of file optionletstripper1.hpp.

◆ switchStrike_

|

mutableprivate |

Definition at line 74 of file optionletstripper1.hpp.

◆ accuracy_

|

private |

Definition at line 75 of file optionletstripper1.hpp.

◆ maxIter_

|

private |

Definition at line 76 of file optionletstripper1.hpp.

◆ dontThrow_

|

private |

Definition at line 77 of file optionletstripper1.hpp.