#include <optionletstripper.hpp>

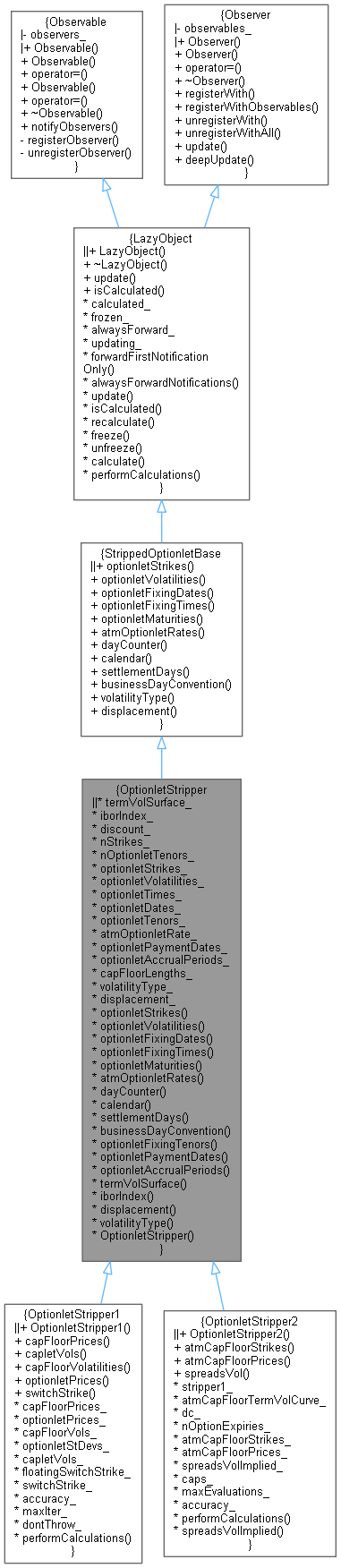

Inheritance diagram for OptionletStripper:

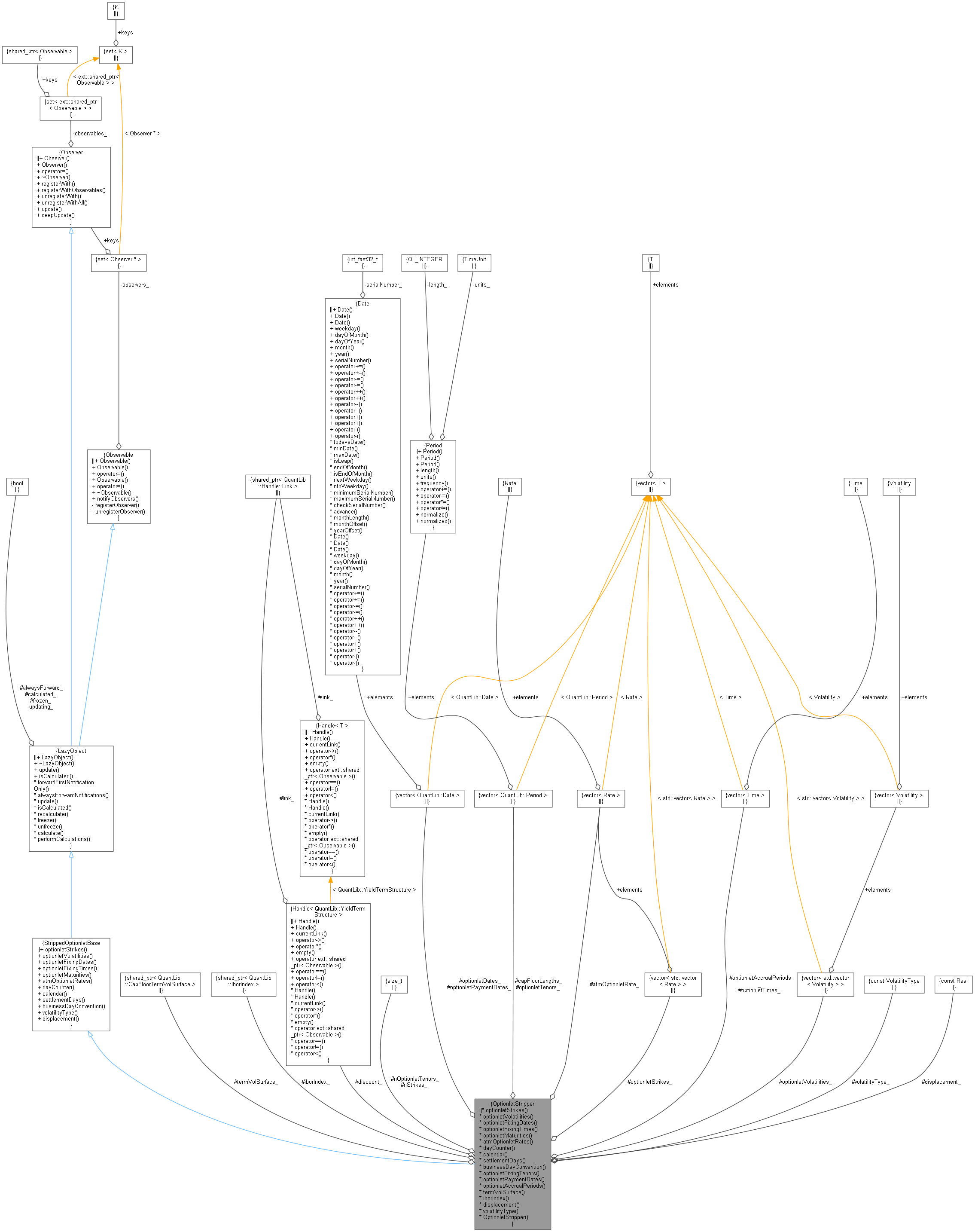

Inheritance diagram for OptionletStripper: Collaboration diagram for OptionletStripper:

Collaboration diagram for OptionletStripper:

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| virtual const std::vector< Rate > & | optionletStrikes (Size i) const =0 |

| virtual const std::vector< Volatility > & | optionletVolatilities (Size i) const =0 |

| virtual const std::vector< Date > & | optionletFixingDates () const =0 |

| virtual const std::vector< Time > & | optionletFixingTimes () const =0 |

| virtual Size | optionletMaturities () const =0 |

| virtual const std::vector< Rate > & | atmOptionletRates () const =0 |

| virtual DayCounter | dayCounter () const =0 |

| virtual Calendar | calendar () const =0 |

| virtual Natural | settlementDays () const =0 |

| virtual BusinessDayConvention | businessDayConvention () const =0 |

| virtual VolatilityType | volatilityType () const =0 |

| virtual Real | displacement () const =0 |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| virtual void | performCalculations () const =0 |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

StrippedOptionletBase specialization. It's up to derived classes to implement LazyObject::performCalculations

Definition at line 41 of file optionletstripper.hpp.

Constructor & Destructor Documentation

◆ OptionletStripper()

|

protected |

Member Function Documentation

◆ optionletStrikes()

Implements StrippedOptionletBase.

Definition at line 79 of file optionletstripper.cpp.

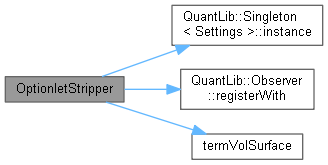

Here is the call graph for this function:

◆ optionletVolatilities()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 89 of file optionletstripper.cpp.

Here is the call graph for this function:

◆ optionletFixingDates()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 102 of file optionletstripper.cpp.

Here is the call graph for this function:

◆ optionletFixingTimes()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 107 of file optionletstripper.cpp.

Here is the call graph for this function:

◆ optionletMaturities()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 112 of file optionletstripper.cpp.

◆ atmOptionletRates()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 126 of file optionletstripper.cpp.

Here is the call graph for this function:

◆ dayCounter()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 132 of file optionletstripper.cpp.

◆ calendar()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 136 of file optionletstripper.cpp.

◆ settlementDays()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 140 of file optionletstripper.cpp.

◆ businessDayConvention()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 144 of file optionletstripper.cpp.

◆ optionletFixingTenors()

| const vector< Period > & optionletFixingTenors | ( | ) | const |

Definition at line 98 of file optionletstripper.cpp.

◆ optionletPaymentDates()

| const vector< Date > & optionletPaymentDates | ( | ) | const |

◆ optionletAccrualPeriods()

| const vector< Time > & optionletAccrualPeriods | ( | ) | const |

◆ termVolSurface()

| ext::shared_ptr< CapFloorTermVolSurface > termVolSurface | ( | ) | const |

◆ iborIndex()

| ext::shared_ptr< IborIndex > iborIndex | ( | ) | const |

Definition at line 153 of file optionletstripper.cpp.

◆ displacement()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 157 of file optionletstripper.cpp.

◆ volatilityType()

|

overridevirtual |

Implements StrippedOptionletBase.

Definition at line 161 of file optionletstripper.cpp.

Member Data Documentation

◆ termVolSurface_

|

protected |

Definition at line 74 of file optionletstripper.hpp.

◆ iborIndex_

|

protected |

Definition at line 75 of file optionletstripper.hpp.

◆ discount_

|

protected |

Definition at line 76 of file optionletstripper.hpp.

◆ nStrikes_

|

protected |

Definition at line 77 of file optionletstripper.hpp.

◆ nOptionletTenors_

|

protected |

Definition at line 78 of file optionletstripper.hpp.

◆ optionletStrikes_

|

mutableprotected |

Definition at line 80 of file optionletstripper.hpp.

◆ optionletVolatilities_

|

mutableprotected |

Definition at line 81 of file optionletstripper.hpp.

◆ optionletTimes_

|

mutableprotected |

Definition at line 83 of file optionletstripper.hpp.

◆ optionletDates_

|

mutableprotected |

Definition at line 84 of file optionletstripper.hpp.

◆ optionletTenors_

|

protected |

Definition at line 85 of file optionletstripper.hpp.

◆ atmOptionletRate_

|

mutableprotected |

Definition at line 86 of file optionletstripper.hpp.

◆ optionletPaymentDates_

|

mutableprotected |

Definition at line 87 of file optionletstripper.hpp.

◆ optionletAccrualPeriods_

|

mutableprotected |

Definition at line 88 of file optionletstripper.hpp.

◆ capFloorLengths_

|

protected |

Definition at line 90 of file optionletstripper.hpp.

◆ volatilityType_

|

protected |

Definition at line 91 of file optionletstripper.hpp.

◆ displacement_

|

protected |

Definition at line 92 of file optionletstripper.hpp.