Pricing engine for compound options using analytical formulae. More...

#include <analyticcompoundoptionengine.hpp>

Inheritance diagram for AnalyticCompoundOptionEngine:

Inheritance diagram for AnalyticCompoundOptionEngine: Collaboration diagram for AnalyticCompoundOptionEngine:

Collaboration diagram for AnalyticCompoundOptionEngine:

Public Member Functions | |

| AnalyticCompoundOptionEngine (ext::shared_ptr< GeneralizedBlackScholesProcess > process) | |

| void | calculate () const override |

| Public Member Functions inherited from GenericEngine< CompoundOption::arguments, CompoundOption::results > | |

| PricingEngine::arguments * | getArguments () const override |

| const PricingEngine::results * | getResults () const override |

| void | reset () override |

| void | update () override |

| Public Member Functions inherited from PricingEngine | |

| ~PricingEngine () override=default | |

| virtual arguments * | getArguments () const =0 |

| virtual const results * | getResults () const =0 |

| virtual void | reset ()=0 |

| virtual void | calculate () const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Attributes | |

| CumulativeNormalDistribution | N_ |

| NormalDistribution | n_ |

| ext::shared_ptr< GeneralizedBlackScholesProcess > | process_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from GenericEngine< CompoundOption::arguments, CompoundOption::results > | |

| CompoundOption::arguments | arguments_ |

| CompoundOption::results | results_ |

Detailed Description

Pricing engine for compound options using analytical formulae.

The formulas are taken from "Foreign Exchange Risk", Uwe Wystup, Risk 2002, where closed form Greeks are available. (not available in Haug 2007). Value: Page 84, Greeks: Pages 94-95.

- Tests:

- the correctness of the returned value is tested by reproducing results available in literature.

Definition at line 42 of file analyticcompoundoptionengine.hpp.

Constructor & Destructor Documentation

◆ AnalyticCompoundOptionEngine()

|

explicit |

Definition at line 56 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function:

Member Function Documentation

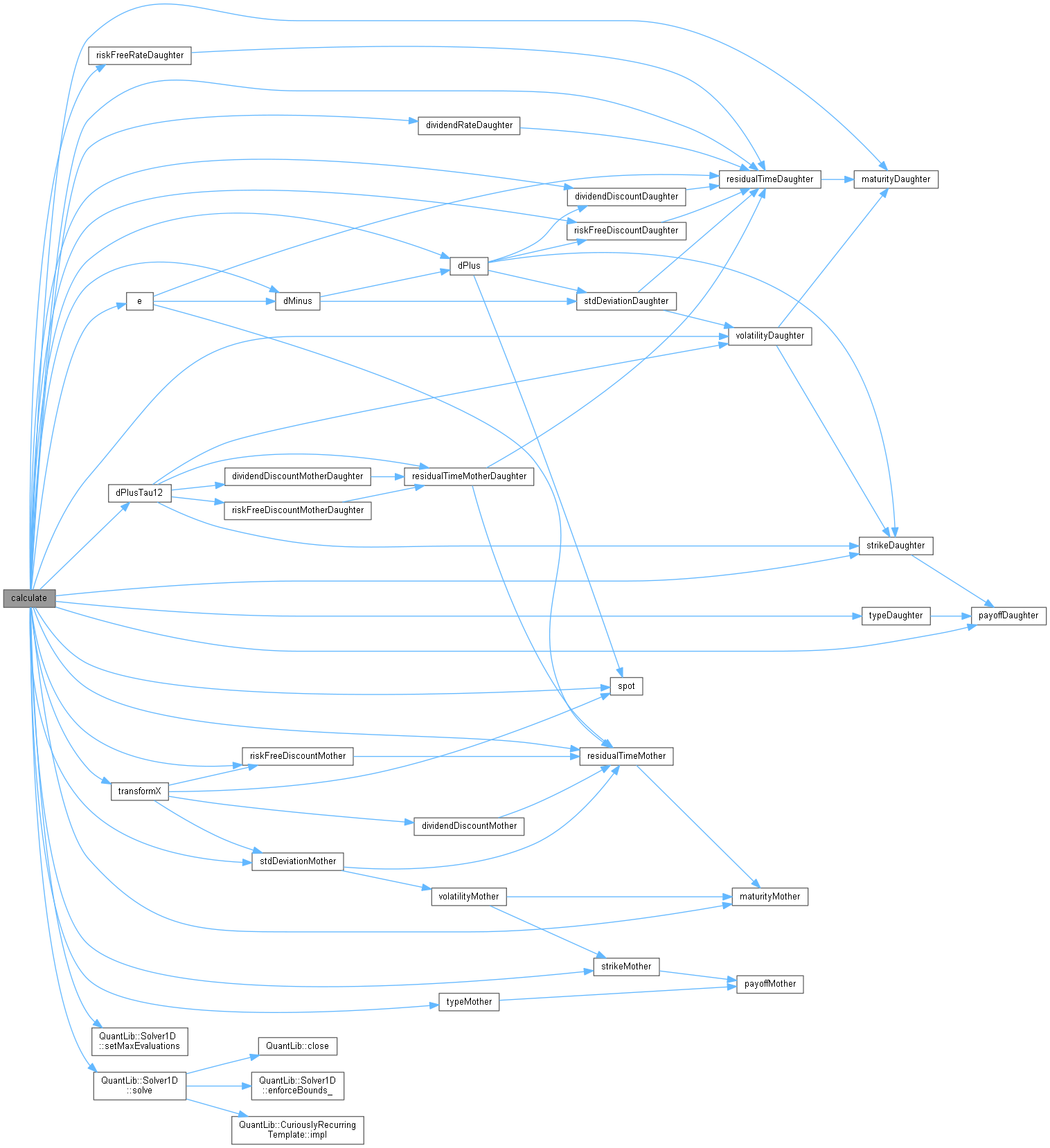

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

Definition at line 62 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function:

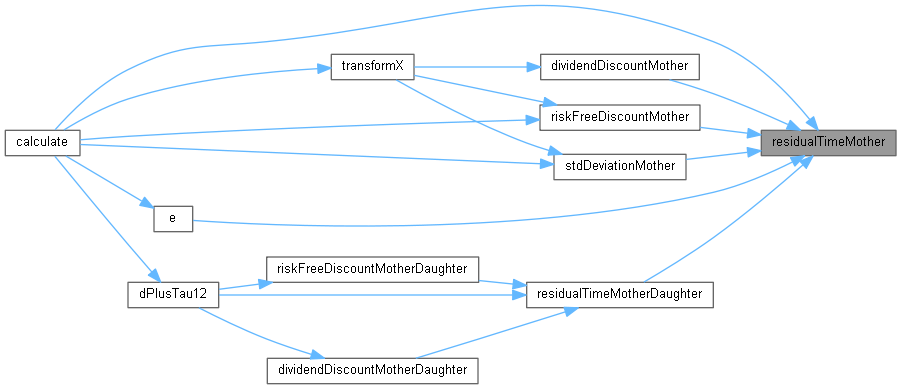

◆ residualTimeMother()

|

private |

Definition at line 171 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ residualTimeDaughter()

|

private |

Definition at line 167 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ residualTimeMotherDaughter()

|

private |

Definition at line 175 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ maturityMother()

|

private |

Definition at line 163 of file analyticcompoundoptionengine.cpp.

Here is the caller graph for this function:

◆ maturityDaughter()

|

private |

Definition at line 159 of file analyticcompoundoptionengine.cpp.

Here is the caller graph for this function:

◆ dPlus()

|

private |

Definition at line 249 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dMinus()

|

private |

Definition at line 255 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dPlusTau12()

Definition at line 259 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dMinusTau12()

|

private |

◆ strikeDaughter()

|

private |

Definition at line 221 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ strikeMother()

|

private |

Definition at line 217 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ spot()

|

private |

Definition at line 265 of file analyticcompoundoptionengine.cpp.

Here is the caller graph for this function:

◆ volatilityDaughter()

|

private |

Definition at line 180 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ volatilityMother()

|

private |

Definition at line 186 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ riskFreeRateDaughter()

|

private |

Definition at line 269 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendRateDaughter()

|

private |

Definition at line 275 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ stdDeviationDaughter()

|

private |

Definition at line 191 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ stdDeviationMother()

|

private |

Definition at line 195 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ typeDaughter()

|

private |

Definition at line 150 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ typeMother()

|

private |

Definition at line 155 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ transformX()

Definition at line 281 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ e()

Definition at line 291 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ riskFreeDiscountDaughter()

|

private |

Definition at line 225 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ riskFreeDiscountMother()

|

private |

Definition at line 229 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ riskFreeDiscountMotherDaughter()

|

private |

Definition at line 233 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendDiscountDaughter()

|

private |

Definition at line 237 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendDiscountMother()

|

private |

Definition at line 241 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendDiscountMotherDaughter()

|

private |

Definition at line 245 of file analyticcompoundoptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ payoffMother()

|

private |

Definition at line 210 of file analyticcompoundoptionengine.cpp.

Here is the caller graph for this function:

◆ payoffDaughter()

|

private |

Definition at line 201 of file analyticcompoundoptionengine.cpp.

Here is the caller graph for this function:

Member Data Documentation

◆ N_

|

private |

Definition at line 49 of file analyticcompoundoptionengine.hpp.

◆ n_

|

private |

Definition at line 50 of file analyticcompoundoptionengine.hpp.

◆ process_

|

private |

Definition at line 51 of file analyticcompoundoptionengine.hpp.