Bachelier-Black-formula cap/floor engine. More...

#include <bacheliercapfloorengine.hpp>

Inheritance diagram for BachelierCapFloorEngine:

Inheritance diagram for BachelierCapFloorEngine: Collaboration diagram for BachelierCapFloorEngine:

Collaboration diagram for BachelierCapFloorEngine:

Private Attributes | |

| Handle< YieldTermStructure > | discountCurve_ |

| Handle< OptionletVolatilityStructure > | vol_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from GenericEngine< CapFloor::arguments, CapFloor::results > | |

| CapFloor::arguments | arguments_ |

| CapFloor::results | results_ |

Detailed Description

Bachelier-Black-formula cap/floor engine.

Definition at line 36 of file bacheliercapfloorengine.hpp.

Constructor & Destructor Documentation

◆ BachelierCapFloorEngine() [1/3]

| BachelierCapFloorEngine | ( | Handle< YieldTermStructure > | discountCurve, |

| Volatility | vol, | ||

| const DayCounter & | dc = Actual365Fixed() |

||

| ) |

Definition at line 31 of file bacheliercapfloorengine.cpp.

Here is the call graph for this function:

◆ BachelierCapFloorEngine() [2/3]

| BachelierCapFloorEngine | ( | Handle< YieldTermStructure > | discountCurve, |

| const Handle< Quote > & | vol, | ||

| const DayCounter & | dc = Actual365Fixed() |

||

| ) |

Definition at line 40 of file bacheliercapfloorengine.cpp.

Here is the call graph for this function:

◆ BachelierCapFloorEngine() [3/3]

| BachelierCapFloorEngine | ( | Handle< YieldTermStructure > | discountCurve, |

| Handle< OptionletVolatilityStructure > | vol | ||

| ) |

Definition at line 50 of file bacheliercapfloorengine.cpp.

Here is the call graph for this function:

Member Function Documentation

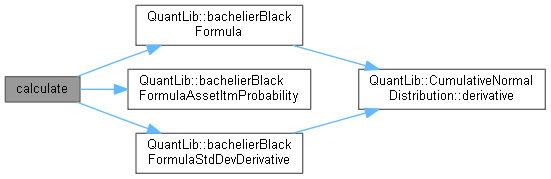

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

Definition at line 62 of file bacheliercapfloorengine.cpp.

Here is the call graph for this function:

◆ termStructure()

| Handle< YieldTermStructure > termStructure | ( | ) |

Definition at line 47 of file bacheliercapfloorengine.hpp.

◆ volatility()

| Handle< OptionletVolatilityStructure > volatility | ( | ) |

Definition at line 48 of file bacheliercapfloorengine.hpp.

Member Data Documentation

◆ discountCurve_

|

private |

Definition at line 50 of file bacheliercapfloorengine.hpp.

◆ vol_

|

private |

Definition at line 51 of file bacheliercapfloorengine.hpp.