Pricing engine for barrier options using analytical formulae. More...

#include <suowangdoublebarrierengine.hpp>

Inheritance diagram for SuoWangDoubleBarrierEngine:

Inheritance diagram for SuoWangDoubleBarrierEngine: Collaboration diagram for SuoWangDoubleBarrierEngine:

Collaboration diagram for SuoWangDoubleBarrierEngine:

Public Member Functions | |

| SuoWangDoubleBarrierEngine (ext::shared_ptr< GeneralizedBlackScholesProcess > process, int series=5) | |

| void | calculate () const override |

| Public Member Functions inherited from GenericEngine< DoubleBarrierOption::arguments, DoubleBarrierOption::results > | |

| PricingEngine::arguments * | getArguments () const override |

| const PricingEngine::results * | getResults () const override |

| void | reset () override |

| void | update () override |

| Public Member Functions inherited from PricingEngine | |

| ~PricingEngine () override=default | |

| virtual arguments * | getArguments () const =0 |

| virtual const results * | getResults () const =0 |

| virtual void | reset ()=0 |

| virtual void | calculate () const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Member Functions | |

| Real | strike () const |

| Time | residualTime () const |

| Volatility | volatility () const |

| Rate | riskFreeRate () const |

| DiscountFactor | riskFreeDiscount () const |

| Rate | dividendYield () const |

| DiscountFactor | dividendDiscount () const |

| Real | D (Real X, Real lambda, Real sigma, Real T) const |

Private Attributes | |

| ext::shared_ptr< GeneralizedBlackScholesProcess > | process_ |

| const int | series_ |

| CumulativeNormalDistribution | f_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from DoubleBarrierOption::engine | |

| bool | triggered (Real underlying) const |

| Protected Attributes inherited from GenericEngine< DoubleBarrierOption::arguments, DoubleBarrierOption::results > | |

| DoubleBarrierOption::arguments | arguments_ |

| DoubleBarrierOption::results | results_ |

Detailed Description

Pricing engine for barrier options using analytical formulae.

The formulas are taken from "Barrier Option Pricing", Wulin Suo, Yong Wang.

- Tests:

- the correctness of the returned value is tested by reproducing results available in literature.

Definition at line 42 of file suowangdoublebarrierengine.hpp.

Constructor & Destructor Documentation

◆ SuoWangDoubleBarrierEngine()

|

explicit |

Definition at line 28 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function:

Member Function Documentation

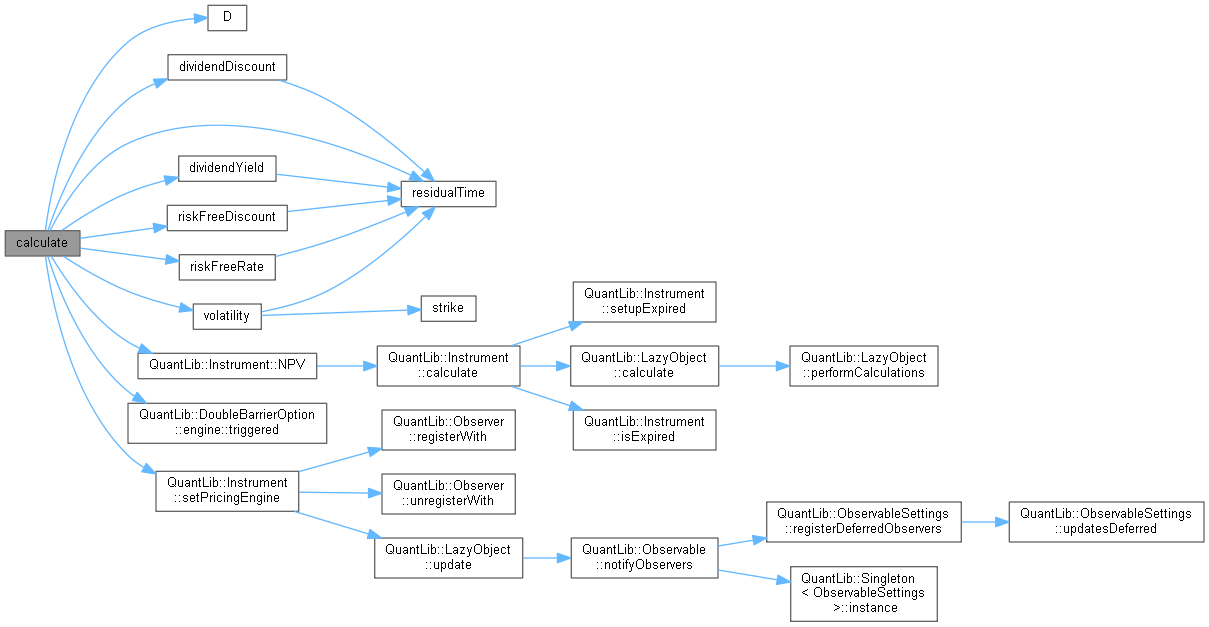

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

Definition at line 34 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function:

◆ strike()

|

private |

Definition at line 133 of file suowangdoublebarrierengine.cpp.

Here is the caller graph for this function:

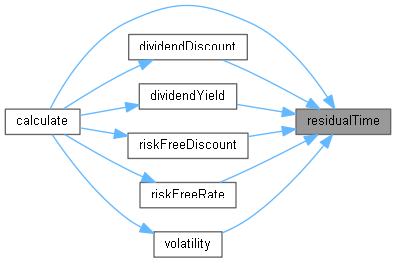

◆ residualTime()

|

private |

Definition at line 140 of file suowangdoublebarrierengine.cpp.

Here is the caller graph for this function:

◆ volatility()

|

private |

Definition at line 144 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ riskFreeRate()

|

private |

Definition at line 148 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ riskFreeDiscount()

|

private |

Definition at line 153 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendYield()

|

private |

Definition at line 157 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ dividendDiscount()

|

private |

Definition at line 162 of file suowangdoublebarrierengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ D()

Definition at line 166 of file suowangdoublebarrierengine.cpp.

Here is the caller graph for this function:

Member Data Documentation

◆ process_

|

private |

Definition at line 49 of file suowangdoublebarrierengine.hpp.

◆ series_

|

private |

Definition at line 50 of file suowangdoublebarrierengine.hpp.

◆ f_

|

private |

Definition at line 51 of file suowangdoublebarrierengine.hpp.