calibration helper for ATM cap More...

#include <caphelper.hpp>

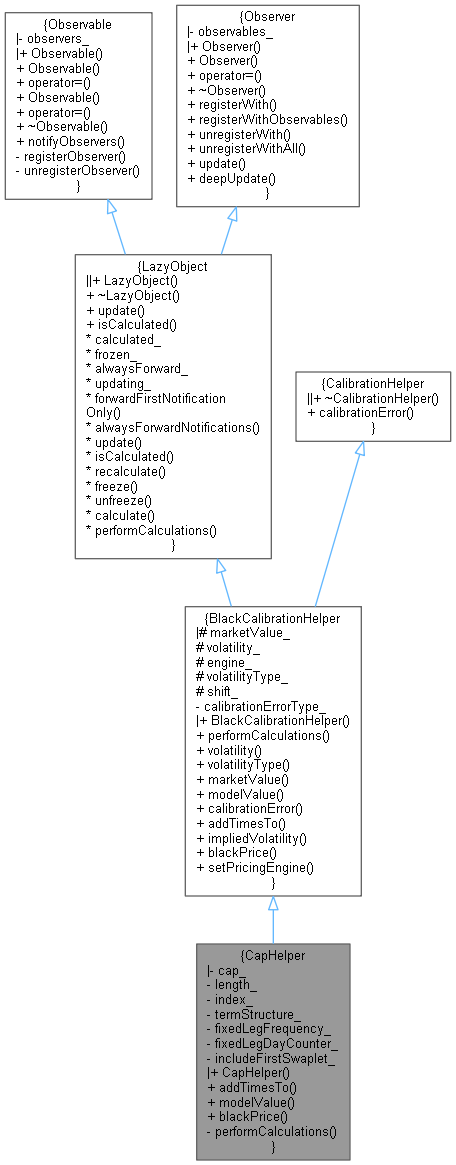

Inheritance diagram for CapHelper:

Inheritance diagram for CapHelper: Collaboration diagram for CapHelper:

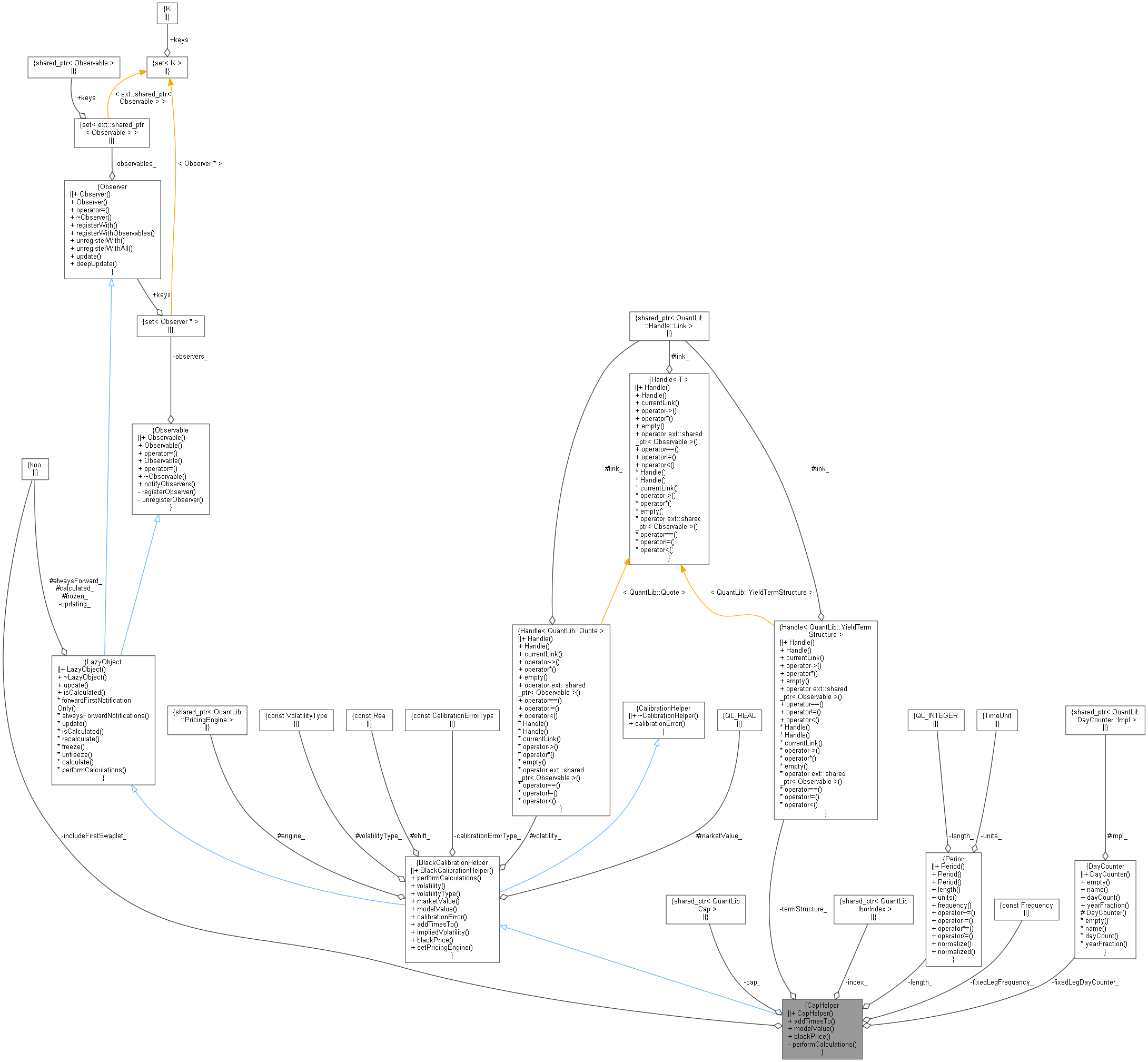

Collaboration diagram for CapHelper:

Public Member Functions | |

| CapHelper (const Period &length, const Handle< Quote > &volatility, ext::shared_ptr< IborIndex > index, Frequency fixedLegFrequency, DayCounter fixedLegDayCounter, bool includeFirstSwaplet, Handle< YieldTermStructure > termStructure, BlackCalibrationHelper::CalibrationErrorType errorType=BlackCalibrationHelper::RelativePriceError, VolatilityType type=ShiftedLognormal, Real shift=0.0) | |

| void | addTimesTo (std::list< Time > ×) const override |

| Real | modelValue () const override |

| returns the price of the instrument according to the model More... | |

| Real | blackPrice (Volatility volatility) const override |

| Black or Bachelier price given a volatility. More... | |

| Public Member Functions inherited from BlackCalibrationHelper | |

| BlackCalibrationHelper (Handle< Quote > volatility, CalibrationErrorType calibrationErrorType=RelativePriceError, const VolatilityType type=ShiftedLognormal, const Real shift=0.0) | |

| void | performCalculations () const override |

| Handle< Quote > | volatility () const |

| returns the volatility Handle More... | |

| VolatilityType | volatilityType () const |

| returns the volatility type More... | |

| Real | marketValue () const |

| returns the actual price of the instrument (from volatility) More... | |

| virtual Real | modelValue () const =0 |

| returns the price of the instrument according to the model More... | |

| Real | calibrationError () override |

| returns the error resulting from the model valuation More... | |

| virtual void | addTimesTo (std::list< Time > ×) const =0 |

| Volatility | impliedVolatility (Real targetValue, Real accuracy, Size maxEvaluations, Volatility minVol, Volatility maxVol) const |

| Black volatility implied by the model. More... | |

| virtual Real | blackPrice (Volatility volatility) const =0 |

| Black or Bachelier price given a volatility. More... | |

| void | setPricingEngine (const ext::shared_ptr< PricingEngine > &engine) |

| Public Member Functions inherited from LazyObject | |

| LazyObject () | |

| ~LazyObject () override=default | |

| void | update () override |

| bool | isCalculated () const |

| void | forwardFirstNotificationOnly () |

| void | alwaysForwardNotifications () |

| void | recalculate () |

| void | freeze () |

| void | unfreeze () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from CalibrationHelper | |

| virtual | ~CalibrationHelper ()=default |

| virtual Real | calibrationError ()=0 |

| returns the error resulting from the model valuation More... | |

Private Member Functions | |

| void | performCalculations () const override |

Private Attributes | |

| ext::shared_ptr< Cap > | cap_ |

| const Period | length_ |

| const ext::shared_ptr< IborIndex > | index_ |

| const Handle< YieldTermStructure > | termStructure_ |

| const Frequency | fixedLegFrequency_ |

| const DayCounter | fixedLegDayCounter_ |

| const bool | includeFirstSwaplet_ |

Additional Inherited Members | |

| Public Types inherited from BlackCalibrationHelper | |

| enum | CalibrationErrorType { RelativePriceError , PriceError , ImpliedVolError } |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from LazyObject | |

| virtual void | calculate () const |

| Protected Attributes inherited from BlackCalibrationHelper | |

| Real | marketValue_ |

| Handle< Quote > | volatility_ |

| ext::shared_ptr< PricingEngine > | engine_ |

| const VolatilityType | volatilityType_ |

| const Real | shift_ |

| Protected Attributes inherited from LazyObject | |

| bool | calculated_ = false |

| bool | frozen_ = false |

| bool | alwaysForward_ |

Detailed Description

calibration helper for ATM cap

Definition at line 35 of file caphelper.hpp.

Constructor & Destructor Documentation

◆ CapHelper()

| CapHelper | ( | const Period & | length, |

| const Handle< Quote > & | volatility, | ||

| ext::shared_ptr< IborIndex > | index, | ||

| Frequency | fixedLegFrequency, | ||

| DayCounter | fixedLegDayCounter, | ||

| bool | includeFirstSwaplet, | ||

| Handle< YieldTermStructure > | termStructure, | ||

| BlackCalibrationHelper::CalibrationErrorType | errorType = BlackCalibrationHelper::RelativePriceError, |

||

| VolatilityType | type = ShiftedLognormal, |

||

| Real | shift = 0.0 |

||

| ) |

Member Function Documentation

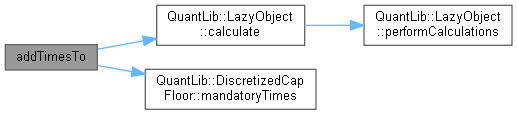

◆ addTimesTo()

|

overridevirtual |

Implements BlackCalibrationHelper.

Definition at line 51 of file caphelper.cpp.

Here is the call graph for this function:

◆ modelValue()

|

overridevirtual |

returns the price of the instrument according to the model

Implements BlackCalibrationHelper.

Definition at line 63 of file caphelper.cpp.

Here is the call graph for this function:

◆ blackPrice()

|

overridevirtual |

Black or Bachelier price given a volatility.

Implements BlackCalibrationHelper.

Definition at line 69 of file caphelper.cpp.

Here is the call graph for this function:

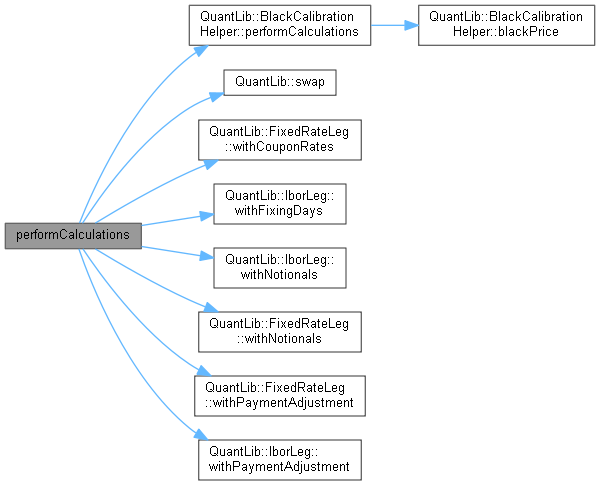

◆ performCalculations()

|

overrideprivatevirtual |

This method must implement any calculations which must be (re)done in order to calculate the desired results.

Reimplemented from BlackCalibrationHelper.

Definition at line 91 of file caphelper.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ cap_

|

mutableprivate |

Definition at line 55 of file caphelper.hpp.

◆ length_

|

private |

Definition at line 56 of file caphelper.hpp.

◆ index_

|

private |

Definition at line 57 of file caphelper.hpp.

◆ termStructure_

|

private |

Definition at line 58 of file caphelper.hpp.

◆ fixedLegFrequency_

|

private |

Definition at line 59 of file caphelper.hpp.

◆ fixedLegDayCounter_

|

private |

Definition at line 60 of file caphelper.hpp.

◆ includeFirstSwaplet_

|

private |

Definition at line 61 of file caphelper.hpp.