Black volatility (smile) surface. More...

#include <blackvolsurface.hpp>

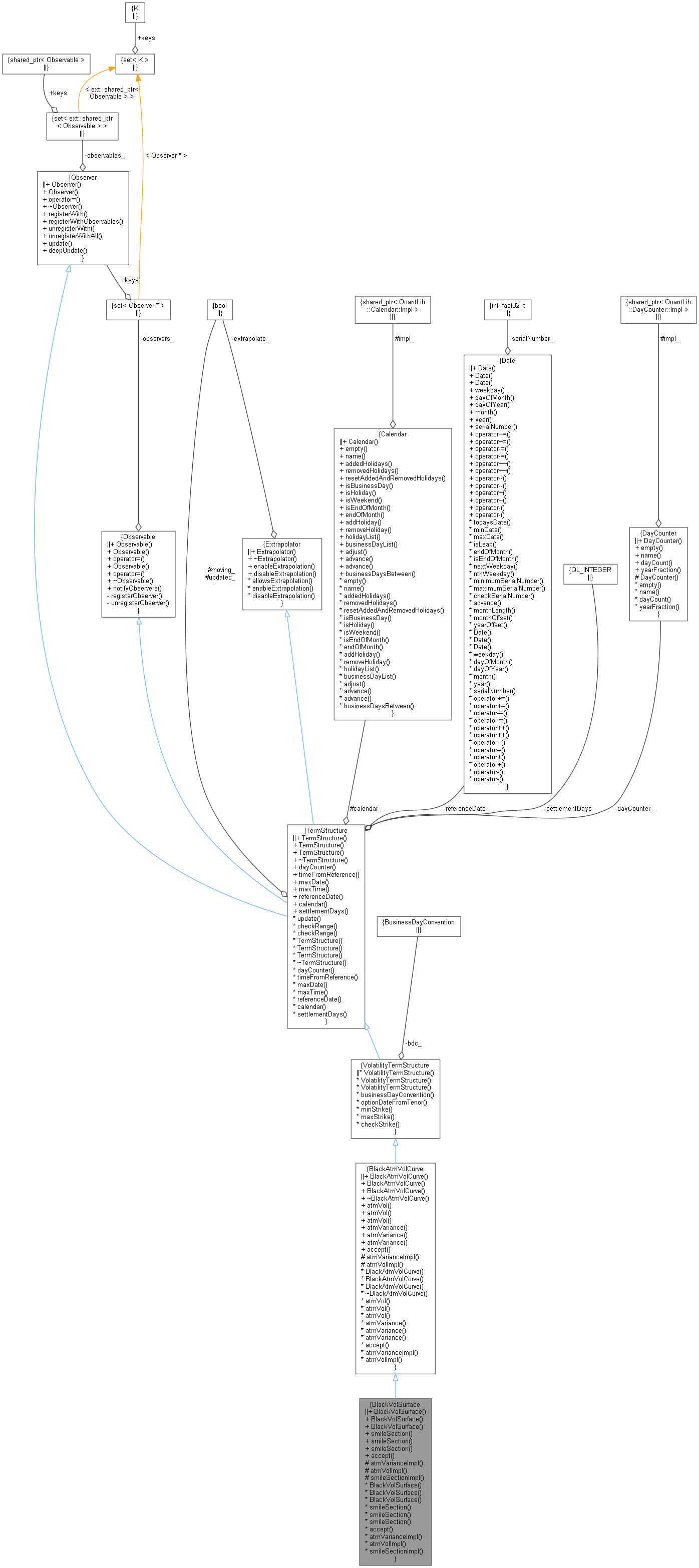

Inheritance diagram for BlackVolSurface:

Inheritance diagram for BlackVolSurface: Collaboration diagram for BlackVolSurface:

Collaboration diagram for BlackVolSurface:

Public Member Functions | |

Constructors | |

See the TermStructure documentation for issues regarding constructors. | |

| BlackVolSurface (BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| default constructor More... | |

| BlackVolSurface (const Date &referenceDate, const Calendar &cal=Calendar(), BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| BlackVolSurface (Natural settlementDays, const Calendar &, BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

Black spot volatility | |

| ext::shared_ptr< SmileSection > | smileSection (const Period &, bool extrapolate) const |

| returns the smile for a given option tenor More... | |

| ext::shared_ptr< SmileSection > | smileSection (const Date &, bool extrapolate) const |

| returns the smile for a given option date More... | |

| ext::shared_ptr< SmileSection > | smileSection (Time, bool extrapolate) const |

| returns the smile for a given option time More... | |

Visitability | |

| void | accept (AcyclicVisitor &) override |

| Public Member Functions inherited from BlackAtmVolCurve | |

| BlackAtmVolCurve (BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| default constructor More... | |

| BlackAtmVolCurve (const Date &referenceDate, const Calendar &cal=Calendar(), BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| BlackAtmVolCurve (Natural settlementDays, const Calendar &, BusinessDayConvention bdc=Following, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~BlackAtmVolCurve () override=default | |

| Volatility | atmVol (const Period &optionTenor, bool extrapolate=false) const |

| spot at-the-money volatility More... | |

| Volatility | atmVol (const Date &maturity, bool extrapolate=false) const |

| spot at-the-money volatility More... | |

| Volatility | atmVol (Time maturity, bool extrapolate=false) const |

| spot at-the-money volatility More... | |

| Real | atmVariance (const Period &optionTenor, bool extrapolate=false) const |

| spot at-the-money variance More... | |

| Real | atmVariance (const Date &maturity, bool extrapolate=false) const |

| spot at-the-money variance More... | |

| Real | atmVariance (Time maturity, bool extrapolate=false) const |

| spot at-the-money variance More... | |

| Public Member Functions inherited from VolatilityTermStructure | |

| VolatilityTermStructure (BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| VolatilityTermStructure (const Date &referenceDate, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| VolatilityTermStructure (Natural settlementDays, const Calendar &cal, BusinessDayConvention bdc, const DayCounter &dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| virtual BusinessDayConvention | businessDayConvention () const |

| the business day convention used in tenor to date conversion More... | |

| Date | optionDateFromTenor (const Period &) const |

| period/date conversion More... | |

| virtual Rate | minStrike () const =0 |

| the minimum strike for which the term structure can return vols More... | |

| virtual Rate | maxStrike () const =0 |

| the maximum strike for which the term structure can return vols More... | |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Date | maxDate () const =0 |

| the latest date for which the curve can return values More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

Protected Member Functions | |

BlackAtmVolCurve interface | |

| Real | atmVarianceImpl (Time t) const override |

| spot at-the-money variance calculation More... | |

| Volatility | atmVolImpl (Time t) const override |

| spot at-the-money volatility calculation More... | |

Calculations | |

This method must be implemented in derived classes to perform the actual volatility calculations. When it is called, time check has already been performed; therefore, it must assume that time-extrapolation is allowed. | |

| virtual ext::shared_ptr< SmileSection > | smileSectionImpl (Time) const =0 |

Calculations | |

These methods must be implemented in derived classes to perform the actual volatility calculations. When they are called, range check has already been performed; therefore, they must assume that extrapolation is required. | |

| Protected Member Functions inherited from VolatilityTermStructure | |

| void | checkStrike (Rate strike, bool extrapolate) const |

| strike-range check More... | |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

Black volatility (smile) surface.

This abstract class defines the interface of concrete Black volatility (smile) surface which will be derived from this one.

Volatilities are assumed to be expressed on an annual basis.

Definition at line 42 of file blackvolsurface.hpp.

Constructor & Destructor Documentation

◆ BlackVolSurface() [1/3]

| BlackVolSurface | ( | BusinessDayConvention | bdc = Following, |

| const DayCounter & | dc = DayCounter() |

||

| ) |

default constructor

- Warning:

- term structures initialized by means of this constructor must manage their own reference date by overriding the referenceDate() method.

Definition at line 25 of file blackvolsurface.cpp.

◆ BlackVolSurface() [2/3]

| BlackVolSurface | ( | const Date & | referenceDate, |

| const Calendar & | cal = Calendar(), |

||

| BusinessDayConvention | bdc = Following, |

||

| const DayCounter & | dc = DayCounter() |

||

| ) |

initialize with a fixed reference date

Definition at line 29 of file blackvolsurface.cpp.

◆ BlackVolSurface() [3/3]

| BlackVolSurface | ( | Natural | settlementDays, |

| const Calendar & | cal, | ||

| BusinessDayConvention | bdc = Following, |

||

| const DayCounter & | dc = DayCounter() |

||

| ) |

calculate the reference date based on the global evaluation date

Definition at line 35 of file blackvolsurface.cpp.

Member Function Documentation

◆ smileSection() [1/3]

| ext::shared_ptr< SmileSection > smileSection | ( | const Period & | p, |

| bool | extrapolate | ||

| ) | const |

returns the smile for a given option tenor

Definition at line 106 of file blackvolsurface.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ smileSection() [2/3]

| ext::shared_ptr< SmileSection > smileSection | ( | const Date & | d, |

| bool | extrapolate | ||

| ) | const |

returns the smile for a given option date

Definition at line 112 of file blackvolsurface.hpp.

Here is the call graph for this function:

◆ smileSection() [3/3]

| ext::shared_ptr< SmileSection > smileSection | ( | Time | t, |

| bool | extrapolate | ||

| ) | const |

returns the smile for a given option time

Definition at line 118 of file blackvolsurface.hpp.

Here is the call graph for this function:

◆ accept()

|

overridevirtual |

Reimplemented from BlackAtmVolCurve.

Reimplemented in EquityFXVolSurface, InterestRateVolSurface, and SabrVolSurface.

Definition at line 51 of file blackvolsurface.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ atmVarianceImpl()

spot at-the-money variance calculation

Implements BlackAtmVolCurve.

Definition at line 41 of file blackvolsurface.cpp.

Here is the call graph for this function:

◆ atmVolImpl()

|

overrideprotectedvirtual |

spot at-the-money volatility calculation

Implements BlackAtmVolCurve.

Definition at line 46 of file blackvolsurface.cpp.

Here is the call graph for this function:

◆ smileSectionImpl()

|

protectedpure virtual |