Analytic Heston engine incl. stochastic interest rates. More...

#include <analytichestonforwardeuropeanengine.hpp>

Inheritance diagram for AnalyticHestonForwardEuropeanEngine:

Inheritance diagram for AnalyticHestonForwardEuropeanEngine: Collaboration diagram for AnalyticHestonForwardEuropeanEngine:

Collaboration diagram for AnalyticHestonForwardEuropeanEngine:

Public Member Functions | |

| AnalyticHestonForwardEuropeanEngine (ext::shared_ptr< HestonProcess > process, Size integrationOrder=144) | |

| void | calculate () const override |

| Real | propagator (Time resetTime, Real varReset) const |

| ext::shared_ptr< AnalyticHestonEngine > | forwardChF (Handle< Quote > &spotReset, Real varReset) const |

| Public Member Functions inherited from GenericEngine< ForwardOptionArguments< VanillaOption::arguments >, VanillaOption::results > | |

| PricingEngine::arguments * | getArguments () const override |

| const PricingEngine::results * | getResults () const override |

| void | reset () override |

| void | update () override |

| Public Member Functions inherited from PricingEngine | |

| ~PricingEngine () override=default | |

| virtual arguments * | getArguments () const =0 |

| virtual const results * | getResults () const =0 |

| virtual void | reset ()=0 |

| virtual void | calculate () const =0 |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Private Member Functions | |

| std::pair< Real, Real > | calculateP1P2 (Time t, Handle< Quote > &St, Real K, Real ratio, Real phiRightLimit=100) const |

| std::pair< Real, Real > | calculateP1P2Hat (Time tenor, Time resetTime, Real K, Real ratio, Real phiRightLimit=100, Real nuRightLimit=2.0) const |

Private Attributes | |

| ext::shared_ptr< HestonProcess > | process_ |

| Size | integrationOrder_ |

| Real | v0_ |

| Real | rho_ |

| Real | kappa_ |

| Real | theta_ |

| Real | sigma_ |

| Handle< YieldTermStructure > | dividendYield_ |

| Handle< YieldTermStructure > | riskFreeRate_ |

| Handle< Quote > | s0_ |

| Real | kappaHat_ |

| Real | thetaHat_ |

| Real | R_ |

| GaussLegendreIntegration | outerIntegrator_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from GenericEngine< ForwardOptionArguments< VanillaOption::arguments >, VanillaOption::results > | |

| ForwardOptionArguments< VanillaOption::arguments > | arguments_ |

| VanillaOption::results | results_ |

Detailed Description

Analytic Heston engine incl. stochastic interest rates.

This class is pricing a european option under the following process

\[ \begin{array}{rcl} dS(t, S) &=& (r-d) S dt +\sqrt{v} S dW_1 \\ dv(t, S) &=& \kappa (\theta - v) dt + \sigma \sqrt{v} dW_2 \\ dW_1 dW_2 &=& \rho dt \\ \end{array} \]

References:

Implements the analytical solution for forward-starting strike-reset options descriped in "On the Pricing of Forward Starting Options under Stochastic Volatility", S. Kruse (2003)

- Tests:

- For tReset > 0, price from the analytic pricer is compared to the MC priver for calls/puts at various moneynesses

- For tReset ~ 0, price from the analytic pricer is compared to the Heston analytic vanilla pricer for various options

Definition at line 64 of file analytichestonforwardeuropeanengine.hpp.

Constructor & Destructor Documentation

◆ AnalyticHestonForwardEuropeanEngine()

|

explicit |

Definition at line 95 of file analytichestonforwardeuropeanengine.cpp.

Member Function Documentation

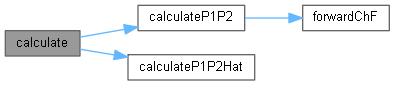

◆ calculate()

|

overridevirtual |

Implements PricingEngine.

Definition at line 121 of file analytichestonforwardeuropeanengine.cpp.

Here is the call graph for this function:

◆ propagator()

Definition at line 218 of file analytichestonforwardeuropeanengine.cpp.

Here is the call graph for this function:

◆ forwardChF()

| ext::shared_ptr< AnalyticHestonEngine > forwardChF | ( | Handle< Quote > & | spotReset, |

| Real | varReset | ||

| ) | const |

Definition at line 233 of file analytichestonforwardeuropeanengine.cpp.

Here is the caller graph for this function:

◆ calculateP1P2()

|

private |

Definition at line 253 of file analytichestonforwardeuropeanengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ calculateP1P2Hat()

|

private |

Definition at line 193 of file analytichestonforwardeuropeanengine.cpp.

Here is the caller graph for this function:

Member Data Documentation

◆ process_

|

private |

Definition at line 83 of file analytichestonforwardeuropeanengine.hpp.

◆ integrationOrder_

|

private |

Definition at line 84 of file analytichestonforwardeuropeanengine.hpp.

◆ v0_

|

private |

Definition at line 87 of file analytichestonforwardeuropeanengine.hpp.

◆ rho_

|

private |

Definition at line 87 of file analytichestonforwardeuropeanengine.hpp.

◆ kappa_

|

private |

Definition at line 87 of file analytichestonforwardeuropeanengine.hpp.

◆ theta_

|

private |

Definition at line 87 of file analytichestonforwardeuropeanengine.hpp.

◆ sigma_

|

private |

Definition at line 87 of file analytichestonforwardeuropeanengine.hpp.

◆ dividendYield_

|

private |

Definition at line 88 of file analytichestonforwardeuropeanengine.hpp.

◆ riskFreeRate_

|

private |

Definition at line 89 of file analytichestonforwardeuropeanengine.hpp.

◆ s0_

Definition at line 90 of file analytichestonforwardeuropeanengine.hpp.

◆ kappaHat_

|

private |

Definition at line 93 of file analytichestonforwardeuropeanengine.hpp.

◆ thetaHat_

|

private |

Definition at line 93 of file analytichestonforwardeuropeanengine.hpp.

◆ R_

|

private |

Definition at line 93 of file analytichestonforwardeuropeanengine.hpp.

◆ outerIntegrator_

|

private |

Definition at line 98 of file analytichestonforwardeuropeanengine.hpp.