Interface for zero inflation term structures. More...

#include <inflationtermstructure.hpp>

Inheritance diagram for ZeroInflationTermStructure:

Inheritance diagram for ZeroInflationTermStructure: Collaboration diagram for ZeroInflationTermStructure:

Collaboration diagram for ZeroInflationTermStructure:

Public Member Functions | |

Constructors | |

| ZeroInflationTermStructure (Date baseDate, Frequency frequency, const DayCounter &dayCounter, const ext::shared_ptr< Seasonality > &seasonality={}) | |

| ZeroInflationTermStructure (const Date &referenceDate, Date baseDate, Frequency frequency, const DayCounter &dayCounter, const ext::shared_ptr< Seasonality > &seasonality={}) | |

| ZeroInflationTermStructure (Natural settlementDays, const Calendar &calendar, Date baseDate, Frequency frequency, const DayCounter &dayCounter, const ext::shared_ptr< Seasonality > &seasonality={}) | |

| Public Member Functions inherited from InflationTermStructure | |

| InflationTermStructure (Date baseDate, Frequency frequency, const DayCounter &dayCounter=DayCounter(), ext::shared_ptr< Seasonality > seasonality={}, Rate baseRate=Null< Rate >()) | |

| InflationTermStructure (const Date &referenceDate, Date baseDate, Frequency frequency, const DayCounter &dayCounter=DayCounter(), ext::shared_ptr< Seasonality > seasonality={}, Rate baseRate=Null< Rate >()) | |

| InflationTermStructure (Natural settlementDays, const Calendar &calendar, Date baseDate, Frequency frequency, const DayCounter &dayCounter=DayCounter(), ext::shared_ptr< Seasonality > seasonality={}, Rate baseRate=Null< Rate >()) | |

| QL_DEPRECATED_DISABLE_WARNING | ~InflationTermStructure () override=default |

| virtual Period | observationLag () const |

| virtual Frequency | frequency () const |

| virtual Rate | baseRate () const |

| virtual Date | baseDate () const |

| minimum (base) date More... | |

| bool | hasExplicitBaseDate () const |

| void | setSeasonality (const ext::shared_ptr< Seasonality > &seasonality) |

| ext::shared_ptr< Seasonality > | seasonality () const |

| bool | hasSeasonality () const |

| Public Member Functions inherited from TermStructure | |

| TermStructure (DayCounter dc=DayCounter()) | |

| default constructor More... | |

| TermStructure (const Date &referenceDate, Calendar calendar=Calendar(), DayCounter dc=DayCounter()) | |

| initialize with a fixed reference date More... | |

| TermStructure (Natural settlementDays, Calendar, DayCounter dc=DayCounter()) | |

| calculate the reference date based on the global evaluation date More... | |

| ~TermStructure () override=default | |

| virtual DayCounter | dayCounter () const |

| the day counter used for date/time conversion More... | |

| Time | timeFromReference (const Date &date) const |

| date/time conversion More... | |

| virtual Date | maxDate () const =0 |

| the latest date for which the curve can return values More... | |

| virtual Time | maxTime () const |

| the latest time for which the curve can return values More... | |

| virtual const Date & | referenceDate () const |

| the date at which discount = 1.0 and/or variance = 0.0 More... | |

| virtual Calendar | calendar () const |

| the calendar used for reference and/or option date calculation More... | |

| virtual Natural | settlementDays () const |

| the settlementDays used for reference date calculation More... | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Extrapolator | |

| Extrapolator ()=default | |

| virtual | ~Extrapolator ()=default |

| void | enableExtrapolation (bool b=true) |

| enable extrapolation in subsequent calls More... | |

| void | disableExtrapolation (bool b=true) |

| disable extrapolation in subsequent calls More... | |

| bool | allowsExtrapolation () const |

| tells whether extrapolation is enabled More... | |

Inspectors | |

| Rate | zeroRate (const Date &d, const Period &instObsLag=Period(-1, Days), bool forceLinearInterpolation=false, bool extrapolate=false) const |

| zero-coupon inflation rate. More... | |

| Rate | zeroRate (Time t, bool extrapolate=false) const |

| zero-coupon inflation rate. More... | |

| virtual Rate | zeroRateImpl (Time t) const =0 |

| to be defined in derived classes More... | |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from InflationTermStructure | |

| void | checkRange (const Date &, bool extrapolate) const |

| void | checkRange (Time t, bool extrapolate) const |

| Protected Member Functions inherited from TermStructure | |

| void | checkRange (const Date &d, bool extrapolate) const |

| date-range check More... | |

| void | checkRange (Time t, bool extrapolate) const |

| time-range check More... | |

| Protected Attributes inherited from InflationTermStructure | |

| ext::shared_ptr< Seasonality > | seasonality_ |

| Period | observationLag_ |

| Frequency | frequency_ |

| Rate | baseRate_ |

| Protected Attributes inherited from TermStructure | |

| bool | moving_ = false |

| bool | updated_ = true |

| Calendar | calendar_ |

Detailed Description

Interface for zero inflation term structures.

Definition at line 126 of file inflationtermstructure.hpp.

Constructor & Destructor Documentation

◆ ZeroInflationTermStructure() [1/3]

| ZeroInflationTermStructure | ( | Date | baseDate, |

| Frequency | frequency, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

Definition at line 110 of file inflationtermstructure.cpp.

◆ ZeroInflationTermStructure() [2/3]

| ZeroInflationTermStructure | ( | const Date & | referenceDate, |

| Date | baseDate, | ||

| Frequency | frequency, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

Definition at line 117 of file inflationtermstructure.cpp.

◆ ZeroInflationTermStructure() [3/3]

| ZeroInflationTermStructure | ( | Natural | settlementDays, |

| const Calendar & | calendar, | ||

| Date | baseDate, | ||

| Frequency | frequency, | ||

| const DayCounter & | dayCounter, | ||

| const ext::shared_ptr< Seasonality > & | seasonality = {} |

||

| ) |

Definition at line 125 of file inflationtermstructure.cpp.

Member Function Documentation

◆ zeroRate() [1/2]

| Rate zeroRate | ( | const Date & | d, |

| const Period & | instObsLag = Period(-1,Days), |

||

| bool | forceLinearInterpolation = false, |

||

| bool | extrapolate = false |

||

| ) | const |

zero-coupon inflation rate.

Essentially the fair rate for a zero-coupon inflation swap (by definition), i.e. the zero term structure uses yearly compounding, which is assumed for ZCIIS instrument quotes.

- Note

- by default you get the same as lag and interpolation as the term structure. If you want to get predictions of RPI/CPI/etc then use an index.

Definition at line 134 of file inflationtermstructure.cpp.

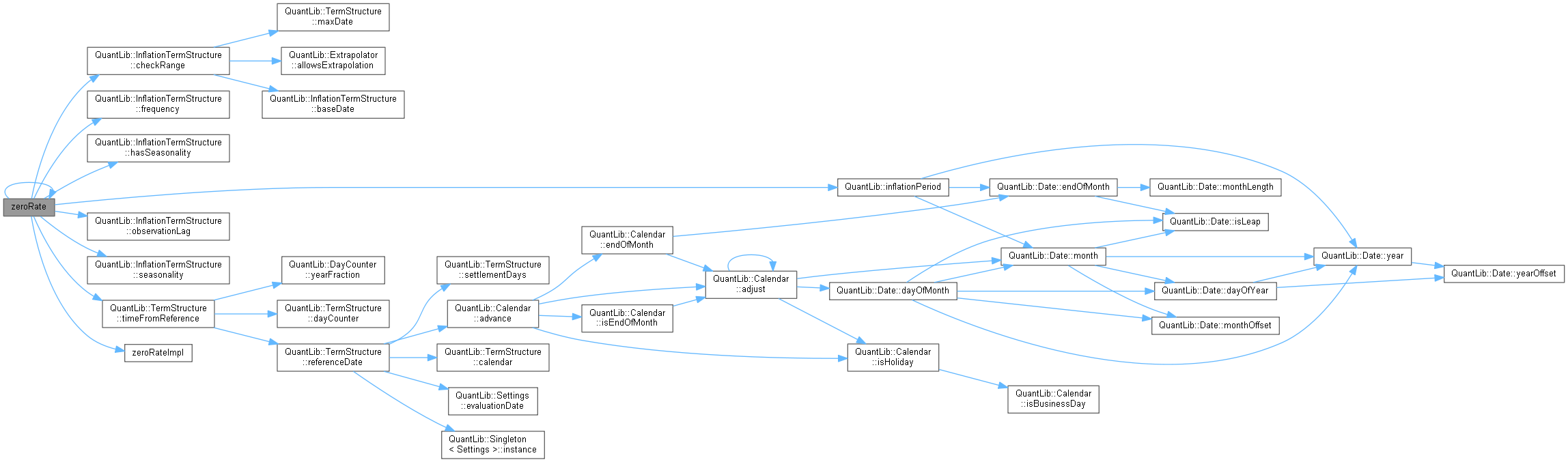

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ zeroRate() [2/2]

zero-coupon inflation rate.

- Warning:

- Since inflation is highly linked to dates (lags, interpolation, months for seasonality, etc) this method cannot account for all effects. If you call it, You'll have to manage lag, seasonality etc. yourself.

Definition at line 170 of file inflationtermstructure.cpp.

Here is the call graph for this function:

◆ zeroRateImpl()

to be defined in derived classes

Implemented in InterpolatedZeroInflationCurve< Interpolator >, and PiecewiseZeroInflationCurve< Interpolator, Bootstrap, Traits >.

Here is the caller graph for this function: