Multi-dimensional simplex class. More...

#include <simplex.hpp>

Inheritance diagram for Simplex:

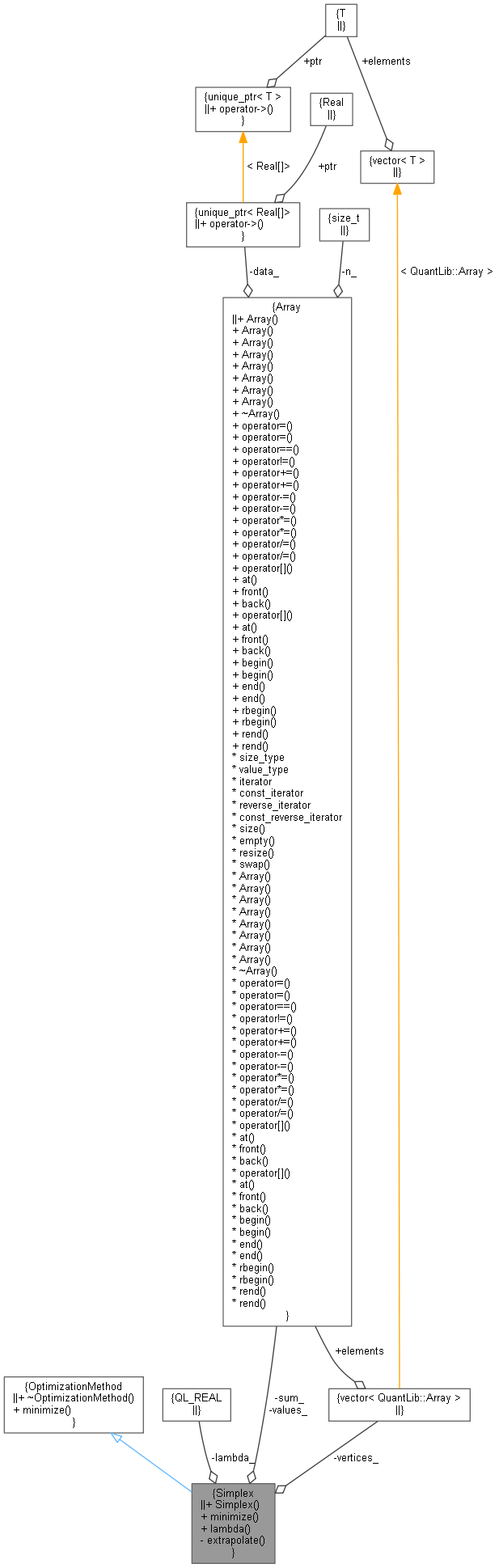

Inheritance diagram for Simplex: Collaboration diagram for Simplex:

Collaboration diagram for Simplex:

Public Member Functions | |

| Simplex (Real lambda) | |

| EndCriteria::Type | minimize (Problem &P, const EndCriteria &endCriteria) override |

| minimize the optimization problem P More... | |

| Real | lambda () const |

| Public Member Functions inherited from OptimizationMethod | |

| virtual | ~OptimizationMethod ()=default |

| virtual EndCriteria::Type | minimize (Problem &P, const EndCriteria &endCriteria)=0 |

| minimize the optimization problem P More... | |

Private Member Functions | |

| Real | extrapolate (Problem &P, Size iHighest, Real &factor) const |

Private Attributes | |

| Real | lambda_ |

| std::vector< Array > | vertices_ |

| Array | values_ |

| Array | sum_ |

Detailed Description

Multi-dimensional simplex class.

This method is rather raw and requires quite a lot of computing resources, but it has the advantage that it does not need any evaluation of the cost function's gradient, and that it is quite easily implemented. First, we choose N+1 starting points, given here by a starting point \( \mathbf{P}_{0} \) and N points such that

\[ \mathbf{P}_{\mathbf{i}}=\mathbf{P}_{0}+\lambda \mathbf{e}_{\mathbf{i}}, \]

where \( \lambda \) is the problem's characteristic length scale). These points will form a geometrical form called simplex. The principle of the downhill simplex method is, at each iteration, to move the worst point (highest cost function value) through the opposite face to a better point. When the simplex seems to be constrained in a valley, it will be contracted downhill, keeping the best point unchanged.

Definition at line 58 of file simplex.hpp.

Constructor & Destructor Documentation

◆ Simplex()

Constructor taking as input the characteristic length

Definition at line 61 of file simplex.hpp.

Member Function Documentation

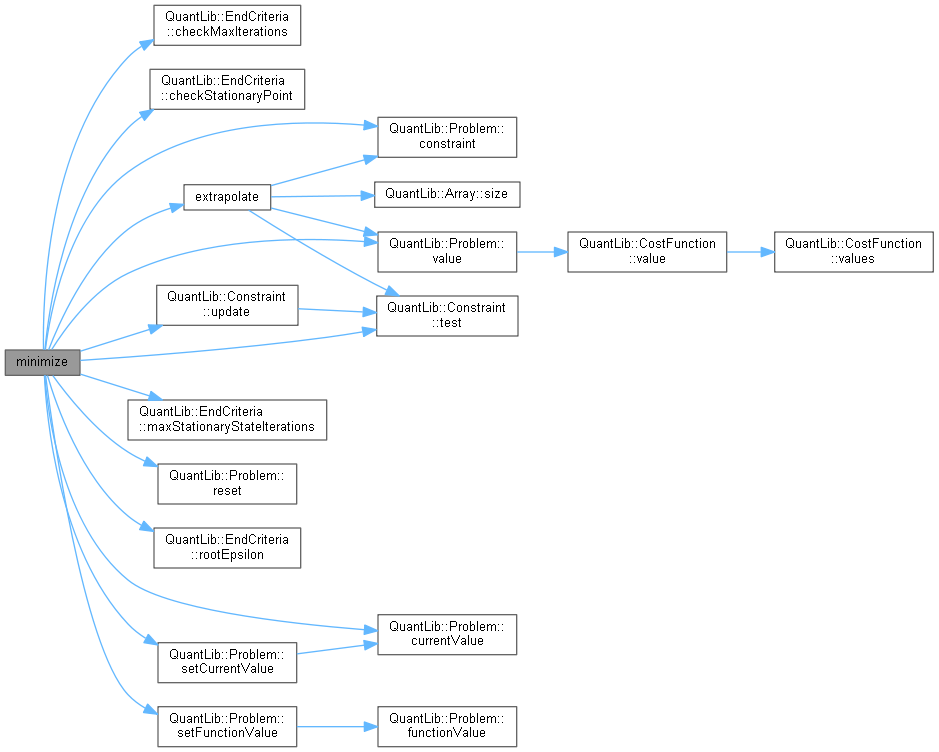

◆ minimize()

|

overridevirtual |

minimize the optimization problem P

Implements OptimizationMethod.

Definition at line 81 of file simplex.cpp.

Here is the call graph for this function:

◆ lambda()

| Real lambda | ( | ) | const |

Definition at line 63 of file simplex.hpp.

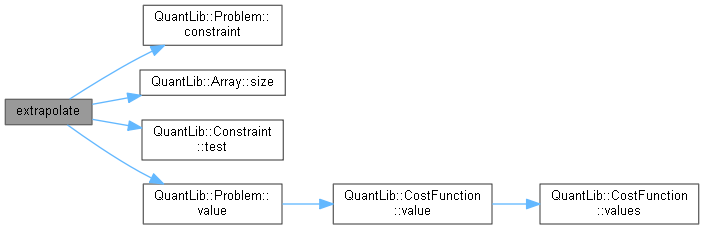

◆ extrapolate()

Definition at line 54 of file simplex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ lambda_

|

private |

Definition at line 69 of file simplex.hpp.

◆ vertices_

|

mutableprivate |

Definition at line 70 of file simplex.hpp.

◆ values_

|

mutableprivate |

Definition at line 71 of file simplex.hpp.

◆ sum_

|

private |

Definition at line 71 of file simplex.hpp.