#include <discretizedswaption.hpp>

Inheritance diagram for DiscretizedSwaption:

Inheritance diagram for DiscretizedSwaption: Collaboration diagram for DiscretizedSwaption:

Collaboration diagram for DiscretizedSwaption:

Public Member Functions | |

| DiscretizedSwaption (const Swaption::arguments &, const Date &referenceDate, const DayCounter &dayCounter) | |

| void | reset (Size size) override |

| Public Member Functions inherited from DiscretizedOption | |

| DiscretizedOption (ext::shared_ptr< DiscretizedAsset > underlying, Exercise::Type exerciseType, std::vector< Time > exerciseTimes) | |

| void | reset (Size size) override |

| std::vector< Time > | mandatoryTimes () const override |

| Public Member Functions inherited from DiscretizedAsset | |

| DiscretizedAsset () | |

| virtual | ~DiscretizedAsset ()=default |

| Time | time () const |

| Time & | time () |

| const Array & | values () const |

| Array & | values () |

| const ext::shared_ptr< Lattice > & | method () const |

| void | initialize (const ext::shared_ptr< Lattice > &, Time t) |

| void | rollback (Time to) |

| void | partialRollback (Time to) |

| Real | presentValue () |

| void | preAdjustValues () |

| void | postAdjustValues () |

| void | adjustValues () |

Static Private Member Functions | |

| static void | prepareSwaptionWithSnappedDates (const Swaption::arguments &args, const Date &referenceDate, const DayCounter &dayCounter, PricingEngine::arguments &snappedArgs, std::vector< CouponAdjustment > &fixedCouponAdjustments, std::vector< CouponAdjustment > &floatingCouponAdjustments) |

Private Attributes | |

| Swaption::arguments | arguments_ |

| Time | lastPayment_ |

Additional Inherited Members | |

| Protected Types inherited from DiscretizedAsset | |

| enum class | CouponAdjustment { pre , post } |

| Protected Member Functions inherited from DiscretizedOption | |

| void | postAdjustValuesImpl () override |

| void | applyExerciseCondition () |

| Protected Member Functions inherited from DiscretizedAsset | |

| bool | isOnTime (Time t) const |

| virtual void | preAdjustValuesImpl () |

| Protected Attributes inherited from DiscretizedOption | |

| ext::shared_ptr< DiscretizedAsset > | underlying_ |

| Exercise::Type | exerciseType_ |

| std::vector< Time > | exerciseTimes_ |

| Protected Attributes inherited from DiscretizedAsset | |

| Time | time_ |

| Time | latestPreAdjustment_ |

| Time | latestPostAdjustment_ |

| Array | values_ |

Detailed Description

Definition at line 34 of file discretizedswaption.hpp.

Constructor & Destructor Documentation

◆ DiscretizedSwaption()

| DiscretizedSwaption | ( | const Swaption::arguments & | args, |

| const Date & | referenceDate, | ||

| const DayCounter & | dayCounter | ||

| ) |

Member Function Documentation

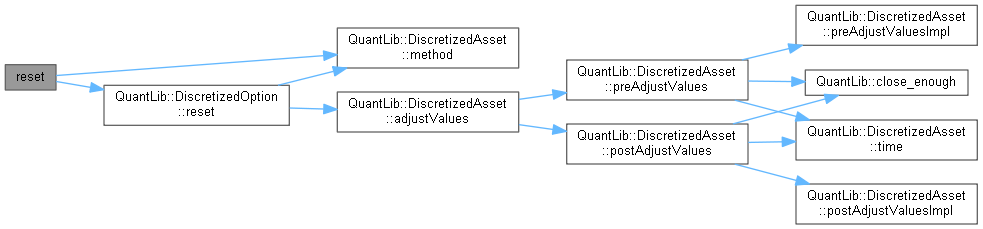

◆ reset()

|

overridevirtual |

This method should initialize the asset values to an Array of the given size and with values depending on the particular asset.

Reimplemented from DiscretizedOption.

Definition at line 72 of file discretizedswaption.cpp.

Here is the call graph for this function:

◆ prepareSwaptionWithSnappedDates()

|

staticprivate |

Definition at line 77 of file discretizedswaption.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ arguments_

|

private |

Definition at line 42 of file discretizedswaption.hpp.

◆ lastPayment_

|

private |

Definition at line 43 of file discretizedswaption.hpp.