#include <bumpinstrumentjacobian.hpp>

Collaboration diagram for OrthogonalizedBumpFinder:

Collaboration diagram for OrthogonalizedBumpFinder:

Public Member Functions | |

| OrthogonalizedBumpFinder (const VegaBumpCollection &bumps, const std::vector< VolatilityBumpInstrumentJacobian::Swaption > &swaptions, const std::vector< VolatilityBumpInstrumentJacobian::Cap > &caps, Real multiplierCutOff, Real tolerance) | |

| void | GetVegaBumps (std::vector< std::vector< Matrix > > &theBumps) const |

Private Attributes | |

| VolatilityBumpInstrumentJacobian | derivativesProducer_ |

| Real | multiplierCutOff_ |

| Real | tolerance_ |

Detailed Description

Pass in a market model, a list of instruments, and possible bumps.

Get out pseudo-root bumps that shift each implied vol by one percent, and leave the other instruments fixed.

If the contribution of an instrument is too correlated with other instruments used, discard it.

- Examples

- MarketModels.cpp.

Definition at line 90 of file bumpinstrumentjacobian.hpp.

Constructor & Destructor Documentation

◆ OrthogonalizedBumpFinder()

| OrthogonalizedBumpFinder | ( | const VegaBumpCollection & | bumps, |

| const std::vector< VolatilityBumpInstrumentJacobian::Swaption > & | swaptions, | ||

| const std::vector< VolatilityBumpInstrumentJacobian::Cap > & | caps, | ||

| Real | multiplierCutOff, | ||

| Real | tolerance | ||

| ) |

Definition at line 138 of file bumpinstrumentjacobian.cpp.

Member Function Documentation

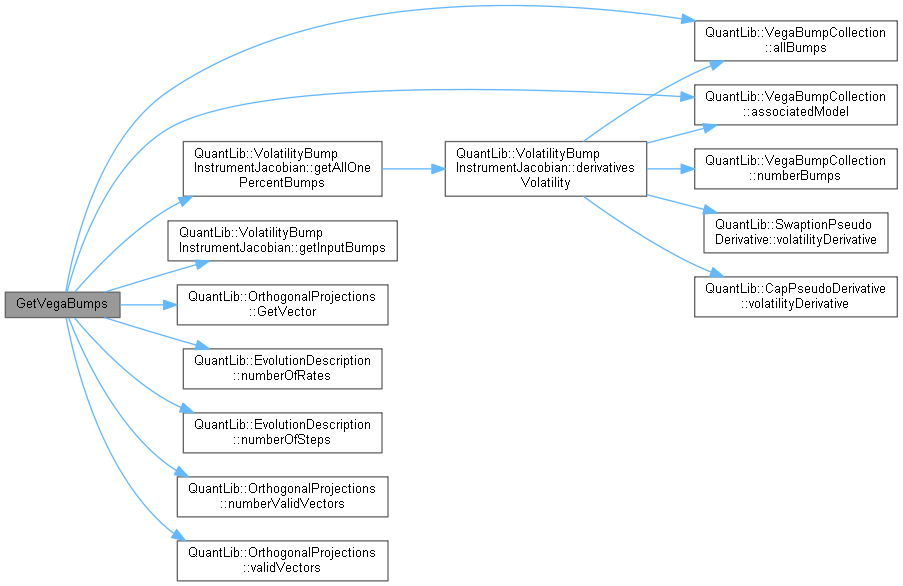

◆ GetVegaBumps()

| void GetVegaBumps | ( | std::vector< std::vector< Matrix > > & | theBumps | ) | const |

- Examples

- MarketModels.cpp.

Definition at line 152 of file bumpinstrumentjacobian.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ derivativesProducer_

|

private |

Definition at line 104 of file bumpinstrumentjacobian.hpp.

◆ multiplierCutOff_

|

private |

Definition at line 105 of file bumpinstrumentjacobian.hpp.

◆ tolerance_

|

private |

Definition at line 106 of file bumpinstrumentjacobian.hpp.