#include <bumpinstrumentjacobian.hpp>

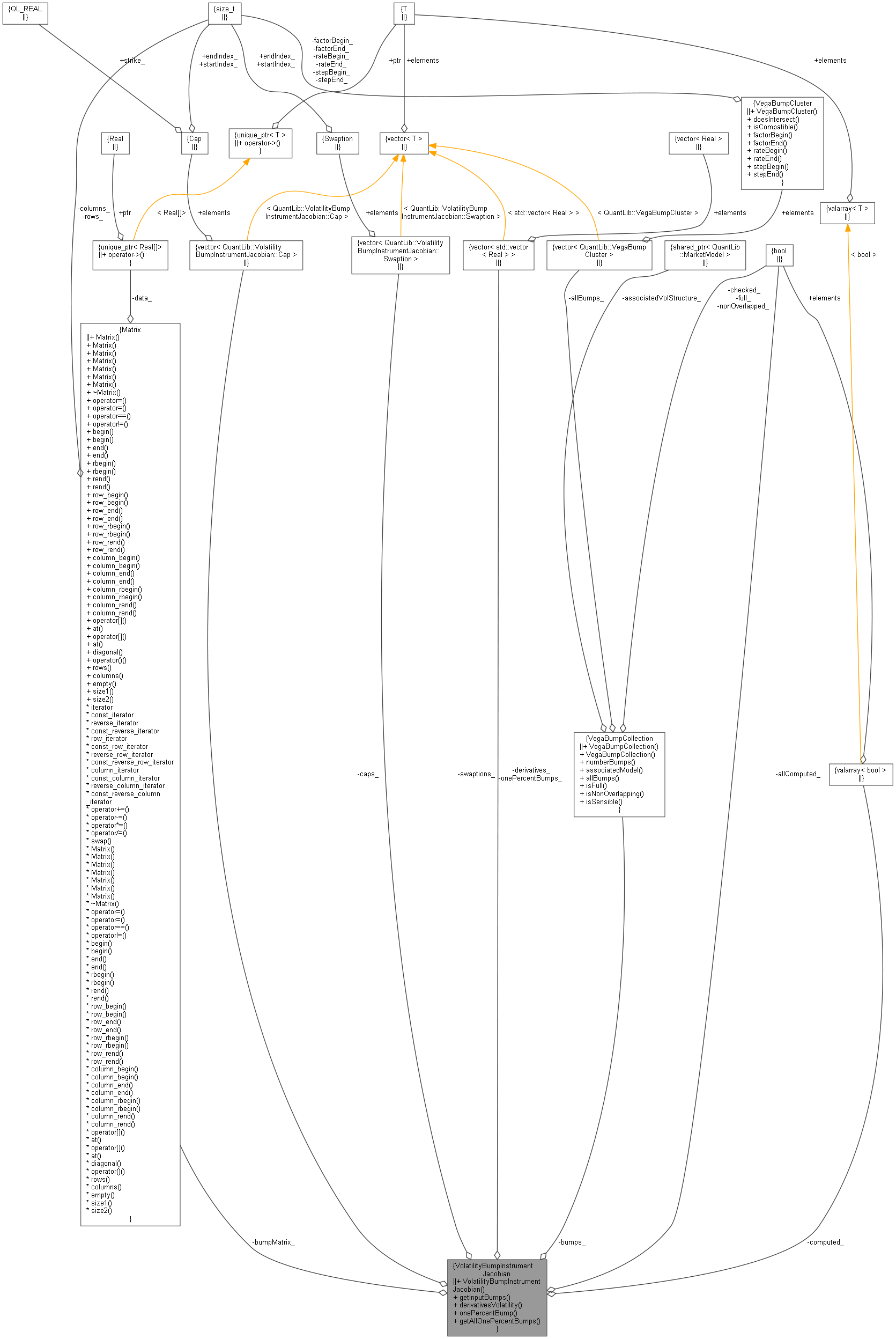

Collaboration diagram for VolatilityBumpInstrumentJacobian:

Collaboration diagram for VolatilityBumpInstrumentJacobian:

Classes | |

| struct | Cap |

| struct | Swaption |

Public Member Functions | |

| VolatilityBumpInstrumentJacobian (const VegaBumpCollection &bumps, const std::vector< Swaption > &swaptions, const std::vector< Cap > &caps) | |

| const VegaBumpCollection & | getInputBumps () const |

| std::vector< Real > | derivativesVolatility (Size j) const |

| std::vector< Real > | onePercentBump (Size j) const |

| const Matrix & | getAllOnePercentBumps () const |

Private Attributes | |

| VegaBumpCollection | bumps_ |

| std::vector< Swaption > | swaptions_ |

| std::vector< Cap > | caps_ |

| std::valarray< bool > | computed_ |

| bool | allComputed_ |

| std::vector< std::vector< Real > > | derivatives_ |

| std::vector< std::vector< Real > > | onePercentBumps_ |

| Matrix | bumpMatrix_ |

Detailed Description

Definition at line 32 of file bumpinstrumentjacobian.hpp.

Constructor & Destructor Documentation

◆ VolatilityBumpInstrumentJacobian()

| VolatilityBumpInstrumentJacobian | ( | const VegaBumpCollection & | bumps, |

| const std::vector< Swaption > & | swaptions, | ||

| const std::vector< Cap > & | caps | ||

| ) |

Definition at line 30 of file bumpinstrumentjacobian.cpp.

Member Function Documentation

◆ getInputBumps()

| const VegaBumpCollection & getInputBumps | ( | ) | const |

Definition at line 56 of file bumpinstrumentjacobian.hpp.

Here is the caller graph for this function:

◆ derivativesVolatility()

Definition at line 42 of file bumpinstrumentjacobian.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ onePercentBump()

Definition at line 118 of file bumpinstrumentjacobian.cpp.

Here is the call graph for this function:

◆ getAllOnePercentBumps()

| const Matrix & getAllOnePercentBumps | ( | ) | const |

Definition at line 124 of file bumpinstrumentjacobian.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ bumps_

|

private |

Definition at line 70 of file bumpinstrumentjacobian.hpp.

◆ swaptions_

|

private |

Definition at line 71 of file bumpinstrumentjacobian.hpp.

◆ caps_

|

private |

Definition at line 72 of file bumpinstrumentjacobian.hpp.

◆ computed_

|

mutableprivate |

Definition at line 73 of file bumpinstrumentjacobian.hpp.

◆ allComputed_

|

mutableprivate |

Definition at line 74 of file bumpinstrumentjacobian.hpp.

◆ derivatives_

|

mutableprivate |

Definition at line 75 of file bumpinstrumentjacobian.hpp.

◆ onePercentBumps_

|

mutableprivate |

Definition at line 77 of file bumpinstrumentjacobian.hpp.

◆ bumpMatrix_

|

mutableprivate |

Definition at line 78 of file bumpinstrumentjacobian.hpp.