Black-formula pricer for capped/floored yoy inflation coupons. More...

#include <inflationcouponpricer.hpp>

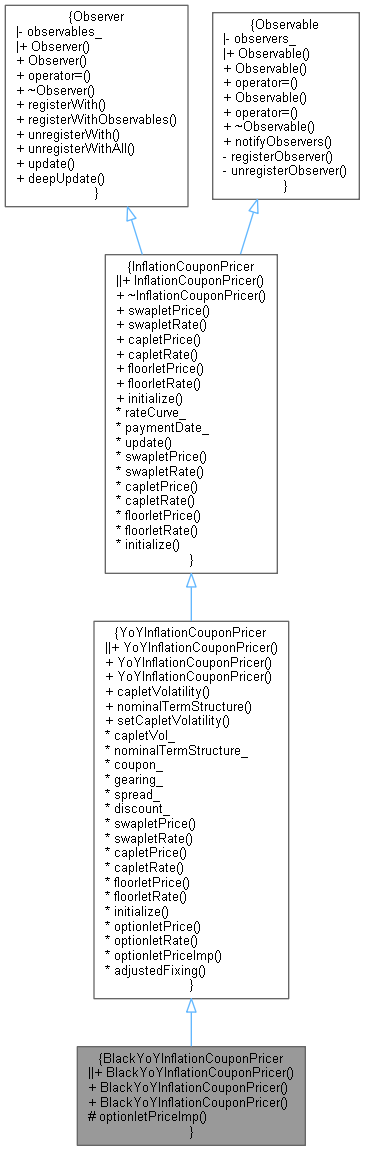

Inheritance diagram for BlackYoYInflationCouponPricer:

Inheritance diagram for BlackYoYInflationCouponPricer: Collaboration diagram for BlackYoYInflationCouponPricer:

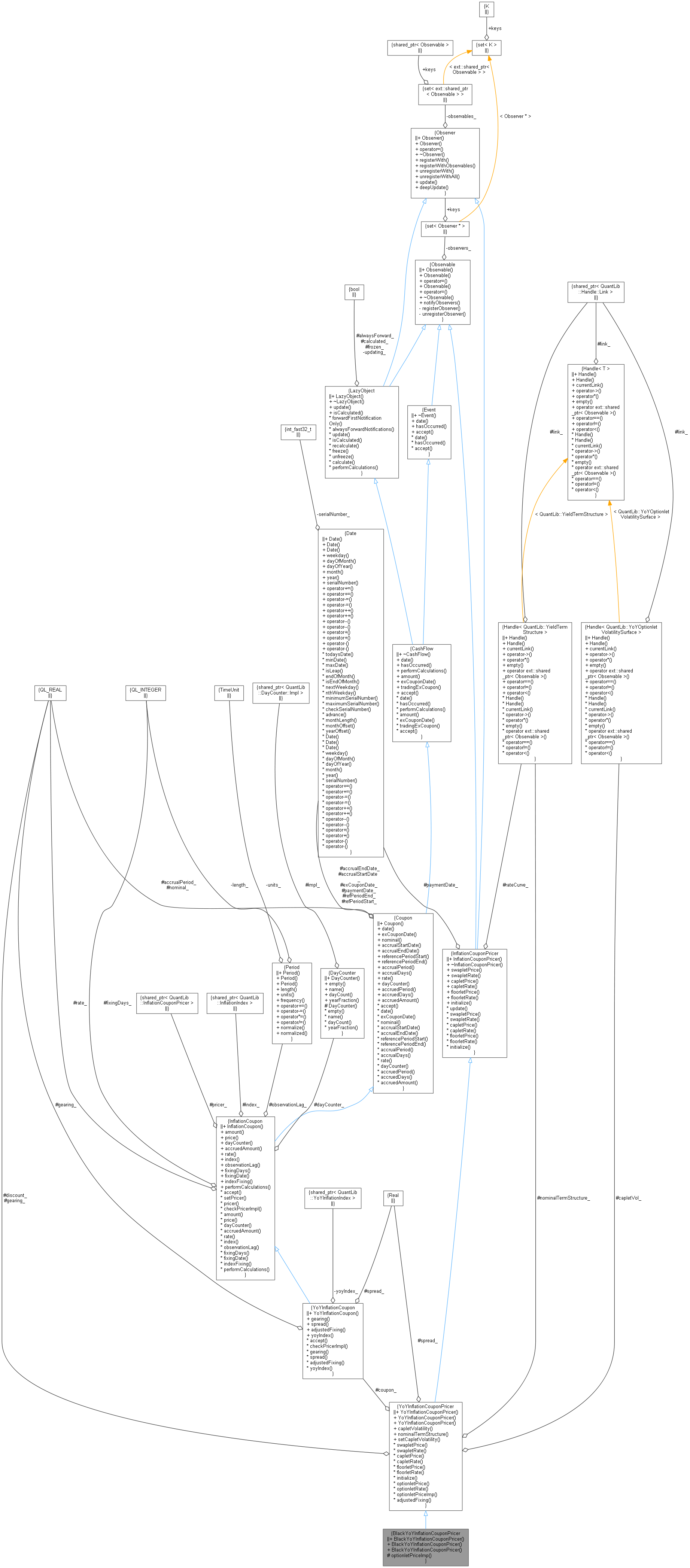

Collaboration diagram for BlackYoYInflationCouponPricer:

Protected Member Functions | |

| Real | optionletPriceImp (Option::Type, Real strike, Real forward, Real stdDev) const override |

| Protected Member Functions inherited from YoYInflationCouponPricer | |

| virtual Real | optionletPrice (Option::Type optionType, Real effStrike) const |

| virtual Real | optionletRate (Option::Type optionType, Real effStrike) const |

| virtual Rate | adjustedFixing (Rate fixing=Null< Rate >()) const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from YoYInflationCouponPricer | |

| Handle< YoYOptionletVolatilitySurface > | capletVol_ |

| data More... | |

| Handle< YieldTermStructure > | nominalTermStructure_ |

| const YoYInflationCoupon * | coupon_ |

| Real | gearing_ |

| Spread | spread_ |

| Real | discount_ |

| Protected Attributes inherited from InflationCouponPricer | |

| Date | paymentDate_ |

Detailed Description

Black-formula pricer for capped/floored yoy inflation coupons.

Definition at line 146 of file inflationcouponpricer.hpp.

Constructor & Destructor Documentation

◆ BlackYoYInflationCouponPricer() [1/3]

Definition at line 148 of file inflationcouponpricer.hpp.

◆ BlackYoYInflationCouponPricer() [2/3]

|

explicit |

Definition at line 152 of file inflationcouponpricer.hpp.

◆ BlackYoYInflationCouponPricer() [3/3]

| BlackYoYInflationCouponPricer | ( | const Handle< YoYOptionletVolatilitySurface > & | capletVol, |

| const Handle< YieldTermStructure > & | nominalTermStructure | ||

| ) |

Definition at line 156 of file inflationcouponpricer.hpp.

Member Function Documentation

◆ optionletPriceImp()

|

overrideprotectedvirtual |

Derived classes usually only need to implement this.

The name of the method is misleading. This actually returns the rate of the optionlet (so not discounted and not accrued).

Reimplemented from YoYInflationCouponPricer.

Definition at line 178 of file inflationcouponpricer.cpp.

Here is the call graph for this function: