#include <ql/math/interpolations/xabrinterpolation.hpp>

Inheritance diagram for XABRInterpolationImpl< I1, I2, Model >:

Inheritance diagram for XABRInterpolationImpl< I1, I2, Model >: Collaboration diagram for XABRInterpolationImpl< I1, I2, Model >:

Collaboration diagram for XABRInterpolationImpl< I1, I2, Model >:

Classes | |

| class | XABRError |

Public Member Functions | |

| XABRInterpolationImpl (const I1 &xBegin, const I1 &xEnd, const I2 &yBegin, Time t, const Real &forward, const std::vector< Real > ¶ms, const std::vector< bool > ¶mIsFixed, bool vegaWeighted, ext::shared_ptr< EndCriteria > endCriteria, ext::shared_ptr< OptimizationMethod > optMethod, const Real errorAccept, const bool useMaxError, const Size maxGuesses, const std::vector< Real > &addParams=std::vector< Real >(), VolatilityType volatilityType=VolatilityType::ShiftedLognormal) | |

| void | update () override |

| Real | value (Real x) const override |

| Real | primitive (Real) const override |

| Real | derivative (Real) const override |

| Real | secondDerivative (Real) const override |

| Real | interpolationSquaredError () const |

| Array | interpolationErrors () const |

| Real | interpolationError () const |

| Real | interpolationMaxError () const |

| Public Member Functions inherited from Interpolation::templateImpl< I1, I2 > | |

| templateImpl (const I1 &xBegin, const I1 &xEnd, const I2 &yBegin, const int requiredPoints=2) | |

| Real | xMin () const override |

| Real | xMax () const override |

| std::vector< Real > | xValues () const override |

| std::vector< Real > | yValues () const override |

| bool | isInRange (Real x) const override |

| Public Member Functions inherited from Interpolation::Impl | |

| virtual | ~Impl ()=default |

| virtual void | update ()=0 |

| virtual Real | xMin () const =0 |

| virtual Real | xMax () const =0 |

| virtual std::vector< Real > | xValues () const =0 |

| virtual std::vector< Real > | yValues () const =0 |

| virtual bool | isInRange (Real) const =0 |

| virtual Real | value (Real) const =0 |

| virtual Real | primitive (Real) const =0 |

| virtual Real | derivative (Real) const =0 |

| virtual Real | secondDerivative (Real) const =0 |

| Public Member Functions inherited from XABRCoeffHolder< Model > | |

| XABRCoeffHolder (const Time t, const Real &forward, const std::vector< Real > ¶ms, const std::vector< bool > ¶mIsFixed, std::vector< Real > addParams) | |

| virtual | ~XABRCoeffHolder ()=default |

| void | updateModelInstance () |

Private Attributes | |

| ext::shared_ptr< EndCriteria > | endCriteria_ |

| ext::shared_ptr< OptimizationMethod > | optMethod_ |

| const Real | errorAccept_ |

| const bool | useMaxError_ |

| const Size | maxGuesses_ |

| bool | vegaWeighted_ |

| NoConstraint | constraint_ |

| VolatilityType | volatilityType_ |

Additional Inherited Members | |

| Public Attributes inherited from XABRCoeffHolder< Model > | |

| Real | t_ |

| const Real & | forward_ |

| std::vector< Real > | params_ |

| std::vector< bool > | paramIsFixed_ |

| std::vector< Real > | weights_ |

| Real | error_ |

| Real | maxError_ |

| EndCriteria::Type | XABREndCriteria_ = EndCriteria::None |

| ext::shared_ptr< typename Model::type > | modelInstance_ |

| std::vector< Real > | addParams_ |

| Protected Member Functions inherited from Interpolation::templateImpl< I1, I2 > | |

| Size | locate (Real x) const |

| Protected Attributes inherited from Interpolation::templateImpl< I1, I2 > | |

| I1 | xBegin_ |

| I1 | xEnd_ |

| I2 | yBegin_ |

Detailed Description

class QuantLib::detail::XABRInterpolationImpl< I1, I2, Model >

Definition at line 102 of file xabrinterpolation.hpp.

Constructor & Destructor Documentation

◆ XABRInterpolationImpl()

| XABRInterpolationImpl | ( | const I1 & | xBegin, |

| const I1 & | xEnd, | ||

| const I2 & | yBegin, | ||

| Time | t, | ||

| const Real & | forward, | ||

| const std::vector< Real > & | params, | ||

| const std::vector< bool > & | paramIsFixed, | ||

| bool | vegaWeighted, | ||

| ext::shared_ptr< EndCriteria > | endCriteria, | ||

| ext::shared_ptr< OptimizationMethod > | optMethod, | ||

| const Real | errorAccept, | ||

| const bool | useMaxError, | ||

| const Size | maxGuesses, | ||

| const std::vector< Real > & | addParams = std::vector<Real>(), |

||

| VolatilityType | volatilityType = VolatilityType::ShiftedLognormal |

||

| ) |

Definition at line 105 of file xabrinterpolation.hpp.

Member Function Documentation

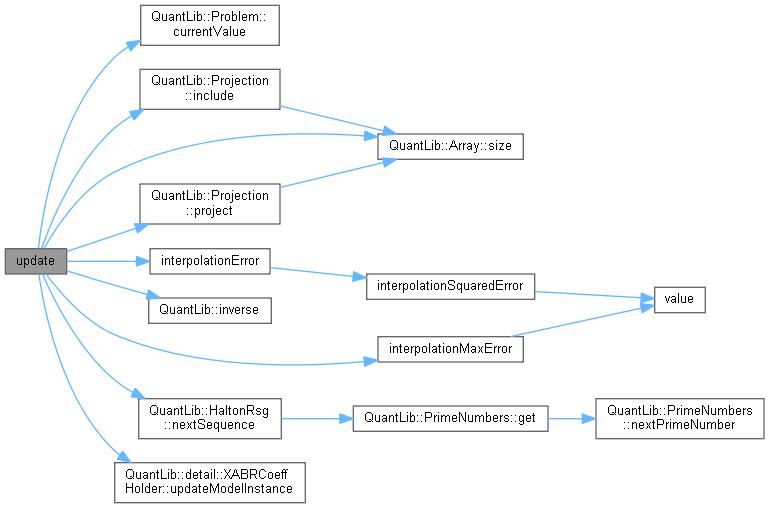

◆ update()

|

overridevirtual |

Implements Interpolation::Impl.

Definition at line 139 of file xabrinterpolation.hpp.

Here is the call graph for this function:

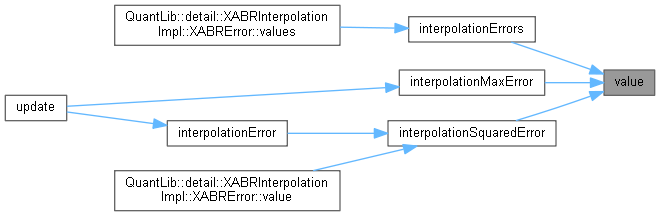

◆ value()

Implements Interpolation::Impl.

Definition at line 241 of file xabrinterpolation.hpp.

Here is the caller graph for this function:

◆ primitive()

Implements Interpolation::Impl.

Definition at line 243 of file xabrinterpolation.hpp.

◆ derivative()

Implements Interpolation::Impl.

Definition at line 244 of file xabrinterpolation.hpp.

◆ secondDerivative()

Implements Interpolation::Impl.

Definition at line 245 of file xabrinterpolation.hpp.

◆ interpolationSquaredError()

| Real interpolationSquaredError | ( | ) | const |

Definition at line 248 of file xabrinterpolation.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ interpolationErrors()

| Array interpolationErrors | ( | ) | const |

Definition at line 261 of file xabrinterpolation.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ interpolationError()

| Real interpolationError | ( | ) | const |

Definition at line 273 of file xabrinterpolation.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ interpolationMaxError()

| Real interpolationMaxError | ( | ) | const |

Definition at line 279 of file xabrinterpolation.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ endCriteria_

|

private |

Definition at line 316 of file xabrinterpolation.hpp.

◆ optMethod_

|

private |

Definition at line 317 of file xabrinterpolation.hpp.

◆ errorAccept_

|

private |

Definition at line 318 of file xabrinterpolation.hpp.

◆ useMaxError_

|

private |

Definition at line 319 of file xabrinterpolation.hpp.

◆ maxGuesses_

|

private |

Definition at line 320 of file xabrinterpolation.hpp.

◆ vegaWeighted_

|

private |

Definition at line 321 of file xabrinterpolation.hpp.

◆ constraint_

|

private |

Definition at line 322 of file xabrinterpolation.hpp.

◆ volatilityType_

|

private |

Definition at line 323 of file xabrinterpolation.hpp.