Interface for inflation cap stripping, i.e. from price surfaces. More...

#include <yoyoptionletstripper.hpp>

Inheritance diagram for YoYOptionletStripper:

Inheritance diagram for YoYOptionletStripper: Collaboration diagram for YoYOptionletStripper:

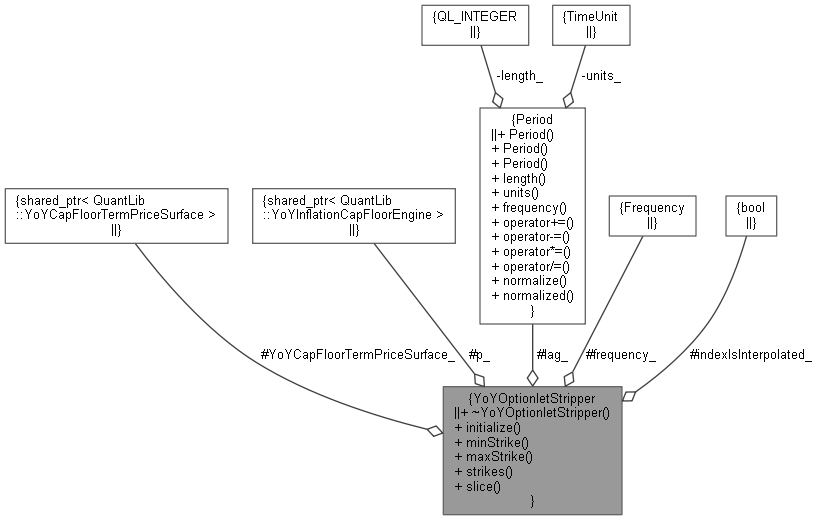

Collaboration diagram for YoYOptionletStripper:

Public Member Functions | |

| virtual | ~YoYOptionletStripper ()=default |

| virtual void | initialize (const ext::shared_ptr< YoYCapFloorTermPriceSurface > &, const ext::shared_ptr< YoYInflationCapFloorEngine > &, Real slope) const =0 |

| YoYOptionletStripper interface. More... | |

| virtual Rate | minStrike () const =0 |

| virtual Rate | maxStrike () const =0 |

| virtual std::vector< Rate > | strikes () const =0 |

| virtual std::pair< std::vector< Rate >, std::vector< Volatility > > | slice (const Date &d) const =0 |

Protected Attributes | |

| ext::shared_ptr< YoYCapFloorTermPriceSurface > | YoYCapFloorTermPriceSurface_ |

| ext::shared_ptr< YoYInflationCapFloorEngine > | p_ |

| Period | lag_ |

| Frequency | frequency_ |

| bool | indexIsInterpolated_ |

Detailed Description

Interface for inflation cap stripping, i.e. from price surfaces.

Strippers return K slices of the volatility surface at a given T. In initialize they actually do the stripping along each K.

Definition at line 37 of file yoyoptionletstripper.hpp.

Constructor & Destructor Documentation

◆ ~YoYOptionletStripper()

|

virtualdefault |

Member Function Documentation

◆ initialize()

|

pure virtual |

YoYOptionletStripper interface.

Implemented in InterpolatedYoYOptionletStripper< Interpolator1D >.

◆ minStrike()

|

pure virtual |

Implemented in InterpolatedYoYOptionletStripper< Interpolator1D >.

◆ maxStrike()

|

pure virtual |

Implemented in InterpolatedYoYOptionletStripper< Interpolator1D >.

◆ strikes()

|

pure virtual |

Implemented in InterpolatedYoYOptionletStripper< Interpolator1D >.

◆ slice()

|

pure virtual |

Implemented in InterpolatedYoYOptionletStripper< Interpolator1D >.

Member Data Documentation

◆ YoYCapFloorTermPriceSurface_

|

mutableprotected |

Definition at line 55 of file yoyoptionletstripper.hpp.

◆ p_

|

mutableprotected |

Definition at line 56 of file yoyoptionletstripper.hpp.

◆ lag_

|

mutableprotected |

Definition at line 57 of file yoyoptionletstripper.hpp.

◆ frequency_

|

mutableprotected |

Definition at line 58 of file yoyoptionletstripper.hpp.

◆ indexIsInterpolated_

|

mutableprotected |

Definition at line 59 of file yoyoptionletstripper.hpp.