helper class More...

#include <makecds.hpp>

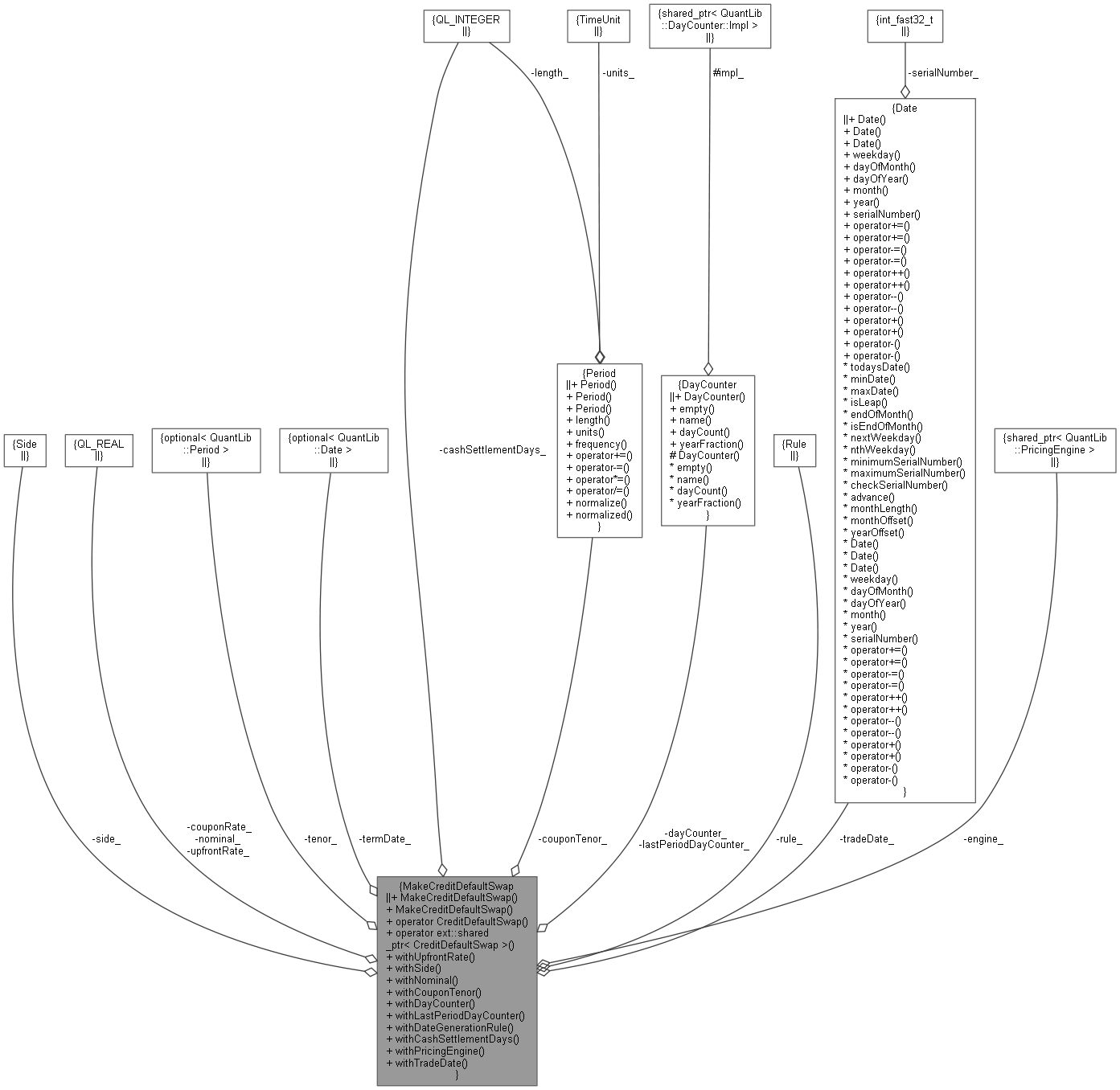

Collaboration diagram for MakeCreditDefaultSwap:

Collaboration diagram for MakeCreditDefaultSwap:

Public Member Functions | |

| MakeCreditDefaultSwap (const Period &tenor, Real couponRate) | |

| MakeCreditDefaultSwap (const Date &termDate, Real couponRate) | |

| operator CreditDefaultSwap () const | |

| operator ext::shared_ptr< CreditDefaultSwap > () const | |

| MakeCreditDefaultSwap & | withUpfrontRate (Real) |

| MakeCreditDefaultSwap & | withSide (Protection::Side) |

| MakeCreditDefaultSwap & | withNominal (Real) |

| MakeCreditDefaultSwap & | withCouponTenor (Period) |

| MakeCreditDefaultSwap & | withDayCounter (DayCounter &) |

| MakeCreditDefaultSwap & | withLastPeriodDayCounter (DayCounter &) |

| MakeCreditDefaultSwap & | withDateGenerationRule (DateGeneration::Rule rule) |

| MakeCreditDefaultSwap & | withCashSettlementDays (Natural cashSettlementDays) |

| MakeCreditDefaultSwap & | withPricingEngine (const ext::shared_ptr< PricingEngine > &) |

| MakeCreditDefaultSwap & | withTradeDate (const Date &tradeDate) |

Private Attributes | |

| Protection::Side | side_ |

| Real | nominal_ |

| ext::optional< Period > | tenor_ |

| ext::optional< Date > | termDate_ |

| Period | couponTenor_ |

| Real | couponRate_ |

| Real | upfrontRate_ |

| DayCounter | dayCounter_ |

| DayCounter | lastPeriodDayCounter_ |

| DateGeneration::Rule | rule_ |

| Natural | cashSettlementDays_ |

| Date | tradeDate_ |

| ext::shared_ptr< PricingEngine > | engine_ |

Detailed Description

helper class

This class provides a more comfortable way to instantiate standard cds.

Definition at line 37 of file makecds.hpp.

Constructor & Destructor Documentation

◆ MakeCreditDefaultSwap() [1/2]

| MakeCreditDefaultSwap | ( | const Period & | tenor, |

| Real | couponRate | ||

| ) |

Definition at line 28 of file makecds.cpp.

◆ MakeCreditDefaultSwap() [2/2]

| MakeCreditDefaultSwap | ( | const Date & | termDate, |

| Real | couponRate | ||

| ) |

Definition at line 35 of file makecds.cpp.

Member Function Documentation

◆ operator CreditDefaultSwap()

| operator CreditDefaultSwap | ( | ) | const |

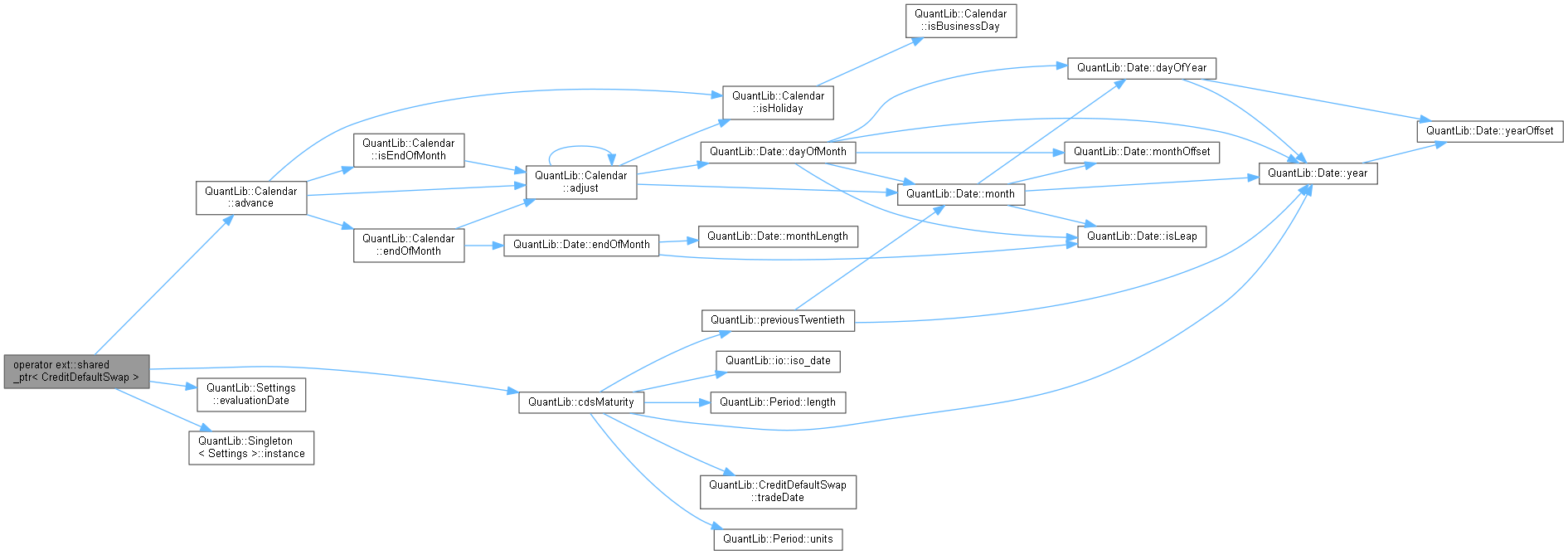

◆ operator ext::shared_ptr< CreditDefaultSwap >()

| operator ext::shared_ptr< CreditDefaultSwap > | ( | ) | const |

◆ withUpfrontRate()

| MakeCreditDefaultSwap & withUpfrontRate | ( | Real | upfrontRate | ) |

Definition at line 86 of file makecds.cpp.

◆ withSide()

| MakeCreditDefaultSwap & withSide | ( | Protection::Side | side | ) |

Definition at line 92 of file makecds.cpp.

◆ withNominal()

| MakeCreditDefaultSwap & withNominal | ( | Real | nominal | ) |

Definition at line 97 of file makecds.cpp.

◆ withCouponTenor()

| MakeCreditDefaultSwap & withCouponTenor | ( | Period | couponTenor | ) |

Definition at line 103 of file makecds.cpp.

◆ withDayCounter()

| MakeCreditDefaultSwap & withDayCounter | ( | DayCounter & | dayCounter | ) |

Definition at line 109 of file makecds.cpp.

◆ withLastPeriodDayCounter()

| MakeCreditDefaultSwap & withLastPeriodDayCounter | ( | DayCounter & | lastPeriodDayCounter | ) |

Definition at line 114 of file makecds.cpp.

◆ withDateGenerationRule()

| MakeCreditDefaultSwap & withDateGenerationRule | ( | DateGeneration::Rule | rule | ) |

Definition at line 120 of file makecds.cpp.

◆ withCashSettlementDays()

| MakeCreditDefaultSwap & withCashSettlementDays | ( | Natural | cashSettlementDays | ) |

Definition at line 125 of file makecds.cpp.

◆ withPricingEngine()

| MakeCreditDefaultSwap & withPricingEngine | ( | const ext::shared_ptr< PricingEngine > & | engine | ) |

Definition at line 130 of file makecds.cpp.

◆ withTradeDate()

| MakeCreditDefaultSwap & withTradeDate | ( | const Date & | tradeDate | ) |

Definition at line 136 of file makecds.cpp.

Member Data Documentation

◆ side_

|

private |

Definition at line 59 of file makecds.hpp.

◆ nominal_

|

private |

Definition at line 60 of file makecds.hpp.

◆ tenor_

|

private |

Definition at line 61 of file makecds.hpp.

◆ termDate_

|

private |

Definition at line 62 of file makecds.hpp.

◆ couponTenor_

|

private |

Definition at line 63 of file makecds.hpp.

◆ couponRate_

|

private |

Definition at line 64 of file makecds.hpp.

◆ upfrontRate_

|

private |

Definition at line 65 of file makecds.hpp.

◆ dayCounter_

|

private |

Definition at line 66 of file makecds.hpp.

◆ lastPeriodDayCounter_

|

private |

Definition at line 67 of file makecds.hpp.

◆ rule_

|

private |

Definition at line 68 of file makecds.hpp.

◆ cashSettlementDays_

|

private |

Definition at line 69 of file makecds.hpp.

◆ tradeDate_

|

private |

Definition at line 70 of file makecds.hpp.

◆ engine_

|

private |

Definition at line 72 of file makecds.hpp.