helper class building a sequence of fixed rate coupons More...

#include <fixedratecoupon.hpp>

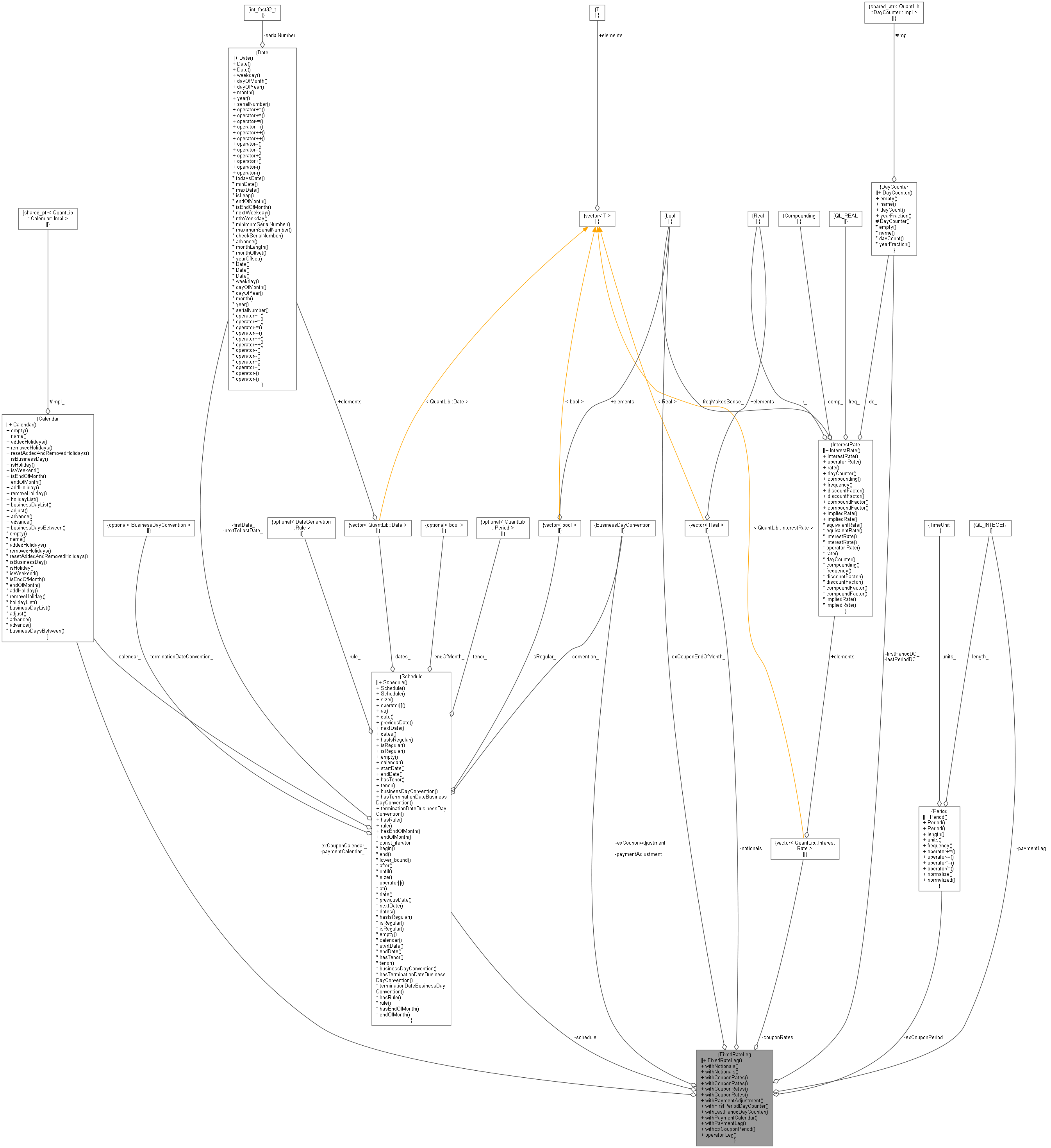

Collaboration diagram for FixedRateLeg:

Collaboration diagram for FixedRateLeg:

Public Member Functions | |

| FixedRateLeg (Schedule schedule) | |

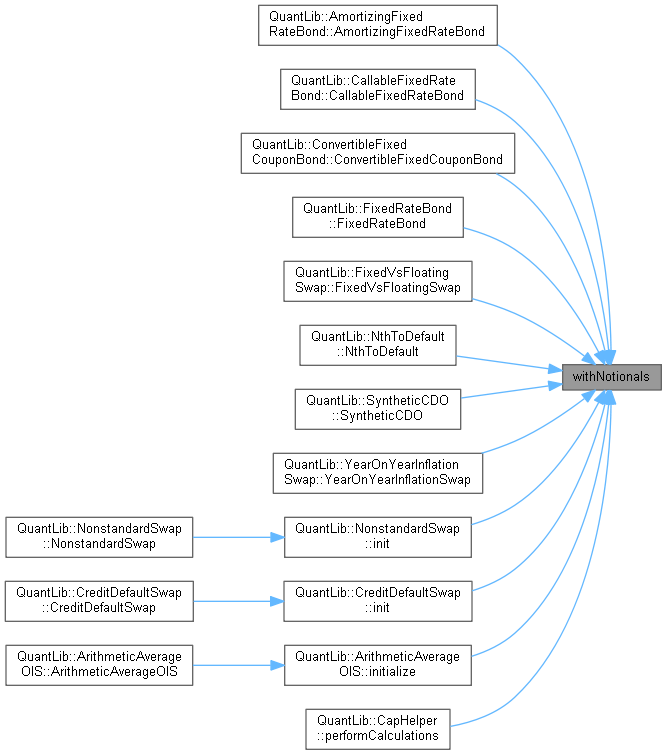

| FixedRateLeg & | withNotionals (Real) |

| FixedRateLeg & | withNotionals (const std::vector< Real > &) |

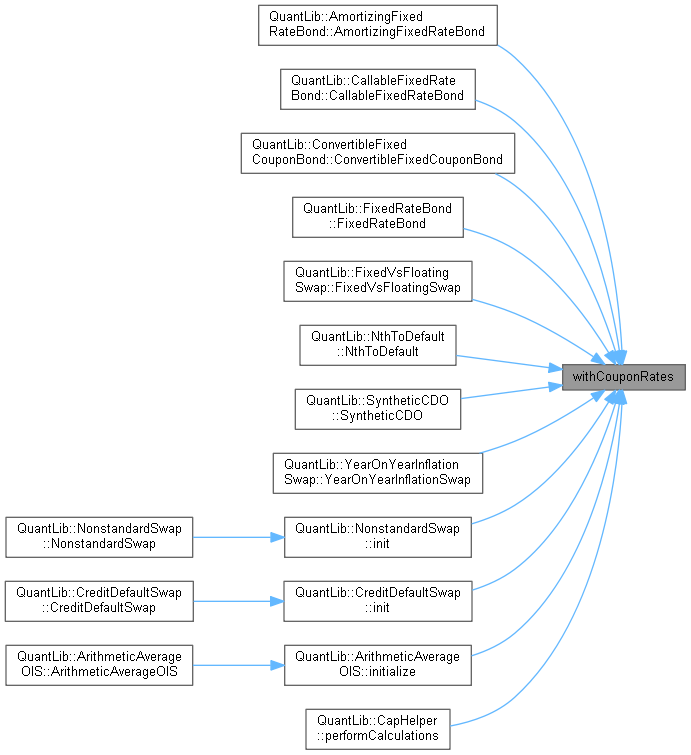

| FixedRateLeg & | withCouponRates (Rate, const DayCounter &paymentDayCounter, Compounding comp=Simple, Frequency freq=Annual) |

| FixedRateLeg & | withCouponRates (const std::vector< Rate > &, const DayCounter &paymentDayCounter, Compounding comp=Simple, Frequency freq=Annual) |

| FixedRateLeg & | withCouponRates (const InterestRate &) |

| FixedRateLeg & | withCouponRates (const std::vector< InterestRate > &) |

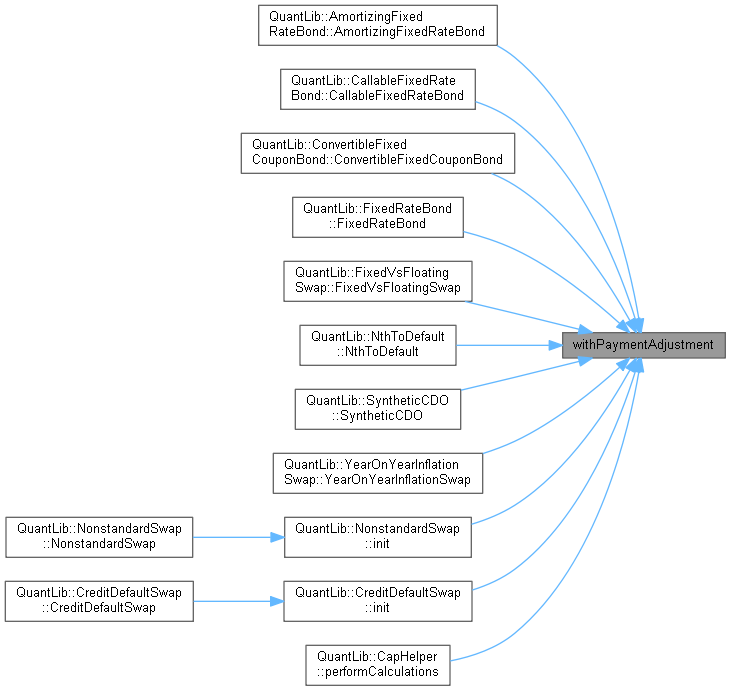

| FixedRateLeg & | withPaymentAdjustment (BusinessDayConvention) |

| FixedRateLeg & | withFirstPeriodDayCounter (const DayCounter &) |

| FixedRateLeg & | withLastPeriodDayCounter (const DayCounter &) |

| FixedRateLeg & | withPaymentCalendar (const Calendar &) |

| FixedRateLeg & | withPaymentLag (Integer lag) |

| FixedRateLeg & | withExCouponPeriod (const Period &, const Calendar &, BusinessDayConvention, bool endOfMonth=false) |

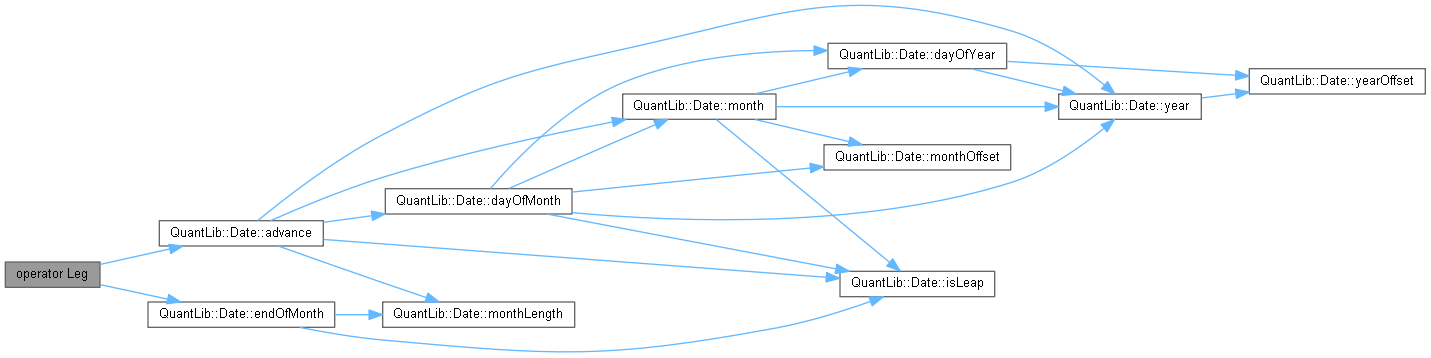

| operator Leg () const | |

Private Attributes | |

| Schedule | schedule_ |

| std::vector< Real > | notionals_ |

| std::vector< InterestRate > | couponRates_ |

| DayCounter | firstPeriodDC_ |

| DayCounter | lastPeriodDC_ |

| Calendar | paymentCalendar_ |

| BusinessDayConvention | paymentAdjustment_ = Following |

| Integer | paymentLag_ = 0 |

| Period | exCouponPeriod_ |

| Calendar | exCouponCalendar_ |

| BusinessDayConvention | exCouponAdjustment_ = Following |

| bool | exCouponEndOfMonth_ = false |

Detailed Description

helper class building a sequence of fixed rate coupons

Definition at line 90 of file fixedratecoupon.hpp.

Constructor & Destructor Documentation

◆ FixedRateLeg()

| FixedRateLeg | ( | Schedule | schedule | ) |

Definition at line 92 of file fixedratecoupon.cpp.

Member Function Documentation

◆ withNotionals() [1/2]

| FixedRateLeg & withNotionals | ( | Real | notional | ) |

◆ withNotionals() [2/2]

| FixedRateLeg & withNotionals | ( | const std::vector< Real > & | notionals | ) |

Definition at line 100 of file fixedratecoupon.cpp.

◆ withCouponRates() [1/4]

| FixedRateLeg & withCouponRates | ( | Rate | rate, |

| const DayCounter & | paymentDayCounter, | ||

| Compounding | comp = Simple, |

||

| Frequency | freq = Annual |

||

| ) |

◆ withCouponRates() [2/4]

| FixedRateLeg & withCouponRates | ( | const std::vector< Rate > & | rates, |

| const DayCounter & | paymentDayCounter, | ||

| Compounding | comp = Simple, |

||

| Frequency | freq = Annual |

||

| ) |

Definition at line 120 of file fixedratecoupon.cpp.

◆ withCouponRates() [3/4]

| FixedRateLeg & withCouponRates | ( | const InterestRate & | i | ) |

Definition at line 114 of file fixedratecoupon.cpp.

◆ withCouponRates() [4/4]

| FixedRateLeg & withCouponRates | ( | const std::vector< InterestRate > & | interestRates | ) |

Definition at line 130 of file fixedratecoupon.cpp.

◆ withPaymentAdjustment()

| FixedRateLeg & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

◆ withFirstPeriodDayCounter()

| FixedRateLeg & withFirstPeriodDayCounter | ( | const DayCounter & | dayCounter | ) |

◆ withLastPeriodDayCounter()

| FixedRateLeg & withLastPeriodDayCounter | ( | const DayCounter & | dayCounter | ) |

◆ withPaymentCalendar()

| FixedRateLeg & withPaymentCalendar | ( | const Calendar & | cal | ) |

◆ withPaymentLag()

| FixedRateLeg & withPaymentLag | ( | Integer | lag | ) |

◆ withExCouponPeriod()

| FixedRateLeg & withExCouponPeriod | ( | const Period & | period, |

| const Calendar & | cal, | ||

| BusinessDayConvention | convention, | ||

| bool | endOfMonth = false |

||

| ) |

◆ operator Leg()

| operator Leg | ( | ) | const |

Member Data Documentation

◆ schedule_

|

private |

Definition at line 116 of file fixedratecoupon.hpp.

◆ notionals_

|

private |

Definition at line 117 of file fixedratecoupon.hpp.

◆ couponRates_

|

private |

Definition at line 118 of file fixedratecoupon.hpp.

◆ firstPeriodDC_

|

private |

Definition at line 119 of file fixedratecoupon.hpp.

◆ lastPeriodDC_

|

private |

Definition at line 119 of file fixedratecoupon.hpp.

◆ paymentCalendar_

|

private |

Definition at line 120 of file fixedratecoupon.hpp.

◆ paymentAdjustment_

|

private |

Definition at line 121 of file fixedratecoupon.hpp.

◆ paymentLag_

|

private |

Definition at line 122 of file fixedratecoupon.hpp.

◆ exCouponPeriod_

|

private |

Definition at line 123 of file fixedratecoupon.hpp.

◆ exCouponCalendar_

|

private |

Definition at line 124 of file fixedratecoupon.hpp.

◆ exCouponAdjustment_

|

private |

Definition at line 125 of file fixedratecoupon.hpp.

◆ exCouponEndOfMonth_

|

private |

Definition at line 126 of file fixedratecoupon.hpp.