#include <fdmlinearop.hpp>

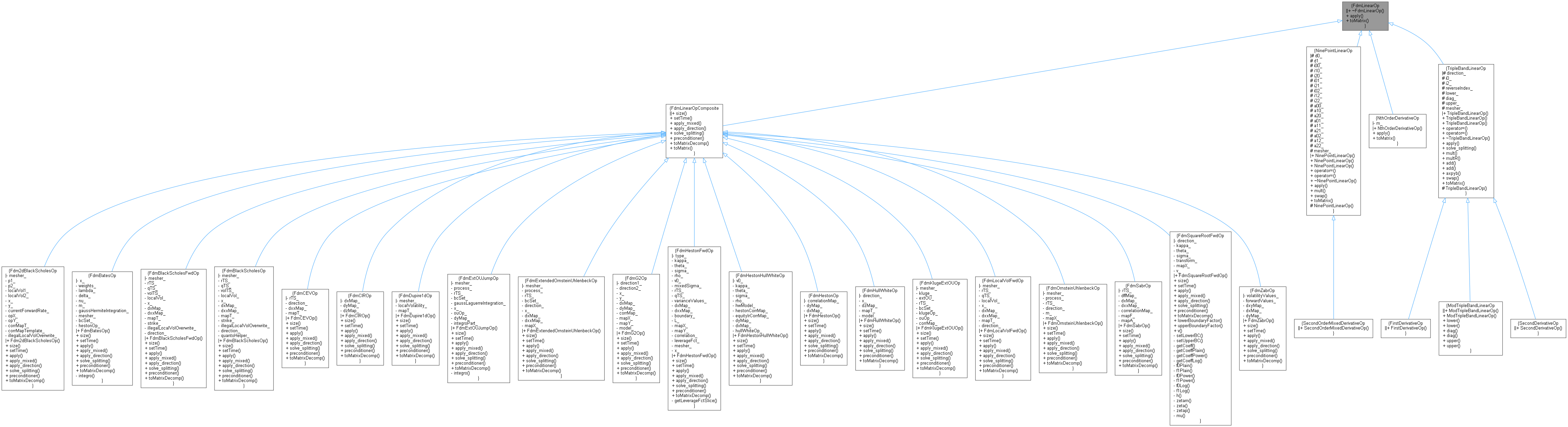

Inheritance diagram for FdmLinearOp:

Inheritance diagram for FdmLinearOp: Collaboration diagram for FdmLinearOp:

Collaboration diagram for FdmLinearOp:

Public Types | |

| typedef Array | array_type |

Public Member Functions | |

| virtual | ~FdmLinearOp ()=default |

| virtual array_type | apply (const array_type &r) const =0 |

| virtual SparseMatrix | toMatrix () const =0 |

Detailed Description

Definition at line 34 of file fdmlinearop.hpp.

Member Typedef Documentation

◆ array_type

| typedef Array array_type |

Definition at line 36 of file fdmlinearop.hpp.

Constructor & Destructor Documentation

◆ ~FdmLinearOp()

|

virtualdefault |

Member Function Documentation

◆ apply()

|

pure virtual |

Implemented in FdmDupire1dOp, FdmExtendedOrnsteinUhlenbeckOp, FdmExtOUJumpOp, FdmKlugeExtOUOp, FdmZabrOp, FdmBatesOp, FdmBlackScholesFwdOp, FdmBlackScholesOp, FdmCEVOp, FdmCIROp, FdmG2Op, FdmHestonFwdOp, FdmHestonHullWhiteOp, FdmHestonOp, FdmHullWhiteOp, FdmLocalVolFwdOp, FdmOrnsteinUhlenbeckOp, FdmSabrOp, FdmSquareRootFwdOp, NinePointLinearOp, TripleBandLinearOp, Fdm2dBlackScholesOp, FdmWienerOp, and NthOrderDerivativeOp.

◆ toMatrix()

|

pure virtual |

Implemented in FdmLinearOpComposite, NinePointLinearOp, NthOrderDerivativeOp, and TripleBandLinearOp.