#include <fdmhestonhullwhiteop.hpp>

Inheritance diagram for FdmHestonHullWhiteOp:

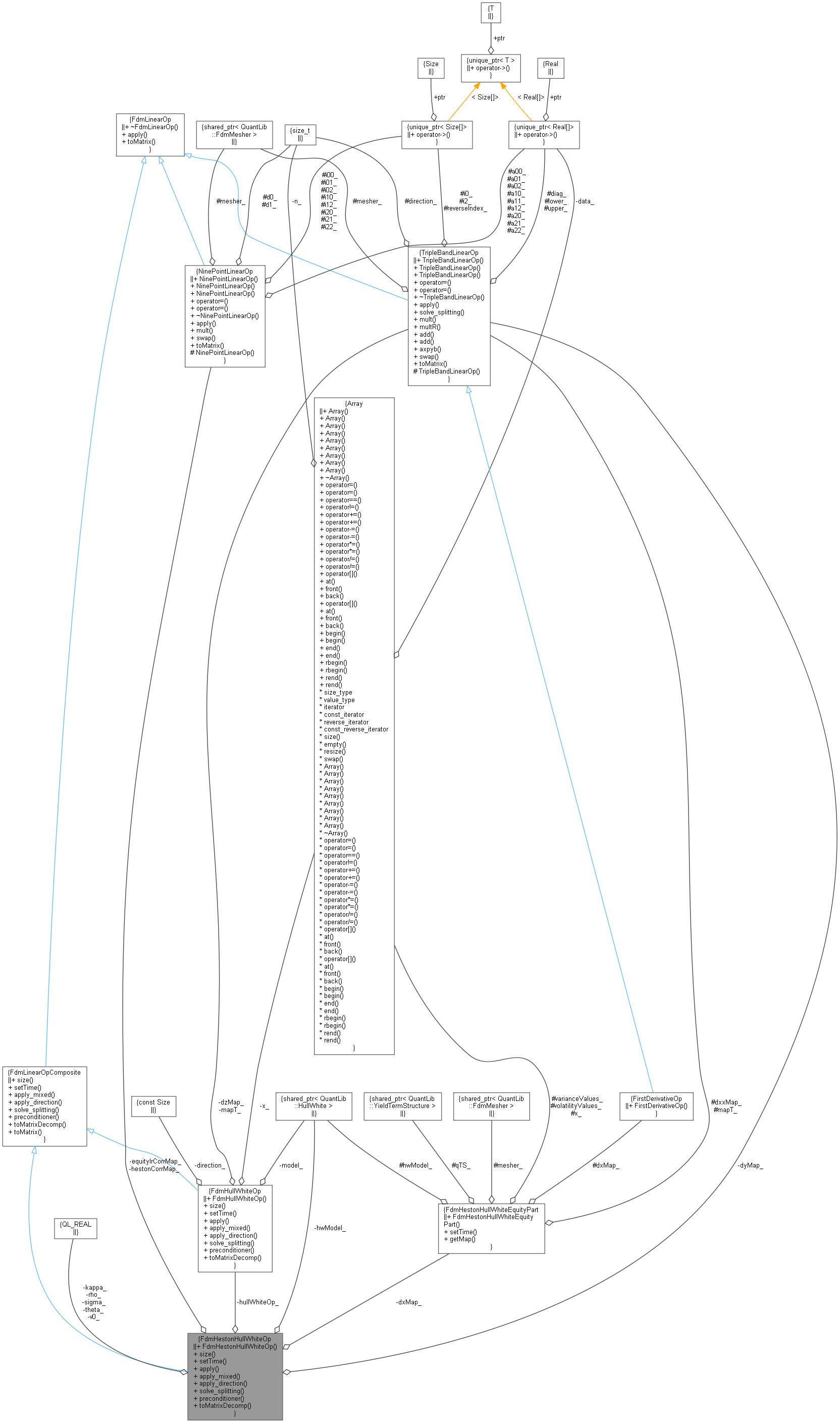

Inheritance diagram for FdmHestonHullWhiteOp: Collaboration diagram for FdmHestonHullWhiteOp:

Collaboration diagram for FdmHestonHullWhiteOp:

Public Member Functions | |

| FdmHestonHullWhiteOp (const ext::shared_ptr< FdmMesher > &mesher, const ext::shared_ptr< HestonProcess > &hestonProcess, const ext::shared_ptr< HullWhiteProcess > &hwProcess, Real equityShortRateCorrelation) | |

| Size | size () const override |

| void | setTime (Time t1, Time t2) override |

| Time \(t1 <= t2\) is required. More... | |

| Array | apply (const Array &r) const override |

| Array | apply_mixed (const Array &r) const override |

| Array | apply_direction (Size direction, const Array &r) const override |

| Array | solve_splitting (Size direction, const Array &r, Real s) const override |

| Array | preconditioner (const Array &r, Real s) const override |

| std::vector< SparseMatrix > | toMatrixDecomp () const override |

| Public Member Functions inherited from FdmLinearOpComposite | |

| virtual Size | size () const =0 |

| virtual void | setTime (Time t1, Time t2)=0 |

| Time \(t1 <= t2\) is required. More... | |

| virtual Array | apply_mixed (const Array &r) const =0 |

| virtual Array | apply_direction (Size direction, const Array &r) const =0 |

| virtual Array | solve_splitting (Size direction, const Array &r, Real s) const =0 |

| virtual Array | preconditioner (const Array &r, Real s) const =0 |

| virtual std::vector< SparseMatrix > | toMatrixDecomp () const |

| SparseMatrix | toMatrix () const override |

| Public Member Functions inherited from FdmLinearOp | |

| virtual | ~FdmLinearOp ()=default |

| virtual array_type | apply (const array_type &r) const =0 |

| virtual SparseMatrix | toMatrix () const =0 |

Private Attributes | |

| const Real | v0_ |

| const Real | kappa_ |

| const Real | theta_ |

| const Real | sigma_ |

| const Real | rho_ |

| const ext::shared_ptr< HullWhite > | hwModel_ |

| NinePointLinearOp | hestonCorrMap_ |

| NinePointLinearOp | equityIrCorrMap_ |

| TripleBandLinearOp | dyMap_ |

| FdmHestonHullWhiteEquityPart | dxMap_ |

| FdmHullWhiteOp | hullWhiteOp_ |

Additional Inherited Members | |

| Public Types inherited from FdmLinearOp | |

| typedef Array | array_type |

Detailed Description

Definition at line 62 of file fdmhestonhullwhiteop.hpp.

Constructor & Destructor Documentation

◆ FdmHestonHullWhiteOp()

| FdmHestonHullWhiteOp | ( | const ext::shared_ptr< FdmMesher > & | mesher, |

| const ext::shared_ptr< HestonProcess > & | hestonProcess, | ||

| const ext::shared_ptr< HullWhiteProcess > & | hwProcess, | ||

| Real | equityShortRateCorrelation | ||

| ) |

Definition at line 69 of file fdmhestonhullwhiteop.cpp.

Member Function Documentation

◆ size()

|

overridevirtual |

Implements FdmLinearOpComposite.

Definition at line 98 of file fdmhestonhullwhiteop.cpp.

◆ setTime()

Time \(t1 <= t2\) is required.

Implements FdmLinearOpComposite.

Definition at line 93 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function:

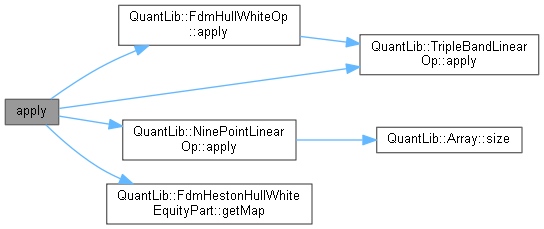

◆ apply()

Implements FdmLinearOp.

Definition at line 102 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function:

◆ apply_mixed()

Implements FdmLinearOpComposite.

Definition at line 120 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function:

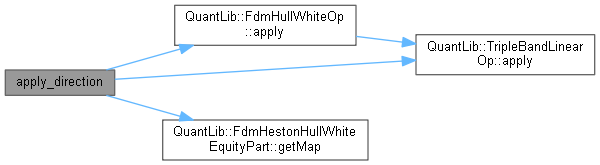

◆ apply_direction()

Implements FdmLinearOpComposite.

Definition at line 108 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function:

◆ solve_splitting()

Implements FdmLinearOpComposite.

Definition at line 124 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ preconditioner()

Implements FdmLinearOpComposite.

Definition at line 139 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function:

◆ toMatrixDecomp()

|

overridevirtual |

Reimplemented from FdmLinearOpComposite.

Definition at line 144 of file fdmhestonhullwhiteop.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ v0_

|

private |

Definition at line 83 of file fdmhestonhullwhiteop.hpp.

◆ kappa_

|

private |

Definition at line 83 of file fdmhestonhullwhiteop.hpp.

◆ theta_

|

private |

Definition at line 83 of file fdmhestonhullwhiteop.hpp.

◆ sigma_

|

private |

Definition at line 83 of file fdmhestonhullwhiteop.hpp.

◆ rho_

|

private |

Definition at line 83 of file fdmhestonhullwhiteop.hpp.

◆ hwModel_

|

private |

Definition at line 84 of file fdmhestonhullwhiteop.hpp.

◆ hestonCorrMap_

|

private |

Definition at line 86 of file fdmhestonhullwhiteop.hpp.

◆ equityIrCorrMap_

|

private |

Definition at line 87 of file fdmhestonhullwhiteop.hpp.

◆ dyMap_

|

private |

Definition at line 88 of file fdmhestonhullwhiteop.hpp.

◆ dxMap_

|

private |

Definition at line 89 of file fdmhestonhullwhiteop.hpp.

◆ hullWhiteOp_

|

private |

Definition at line 90 of file fdmhestonhullwhiteop.hpp.