class for swap-rate spread indexes More...

#include <swapspreadindex.hpp>

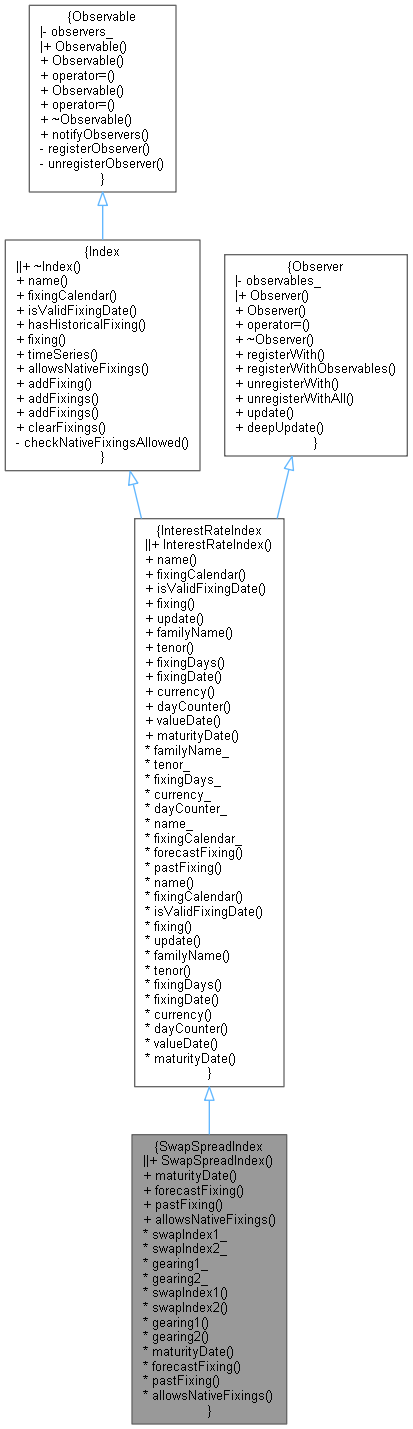

Inheritance diagram for SwapSpreadIndex:

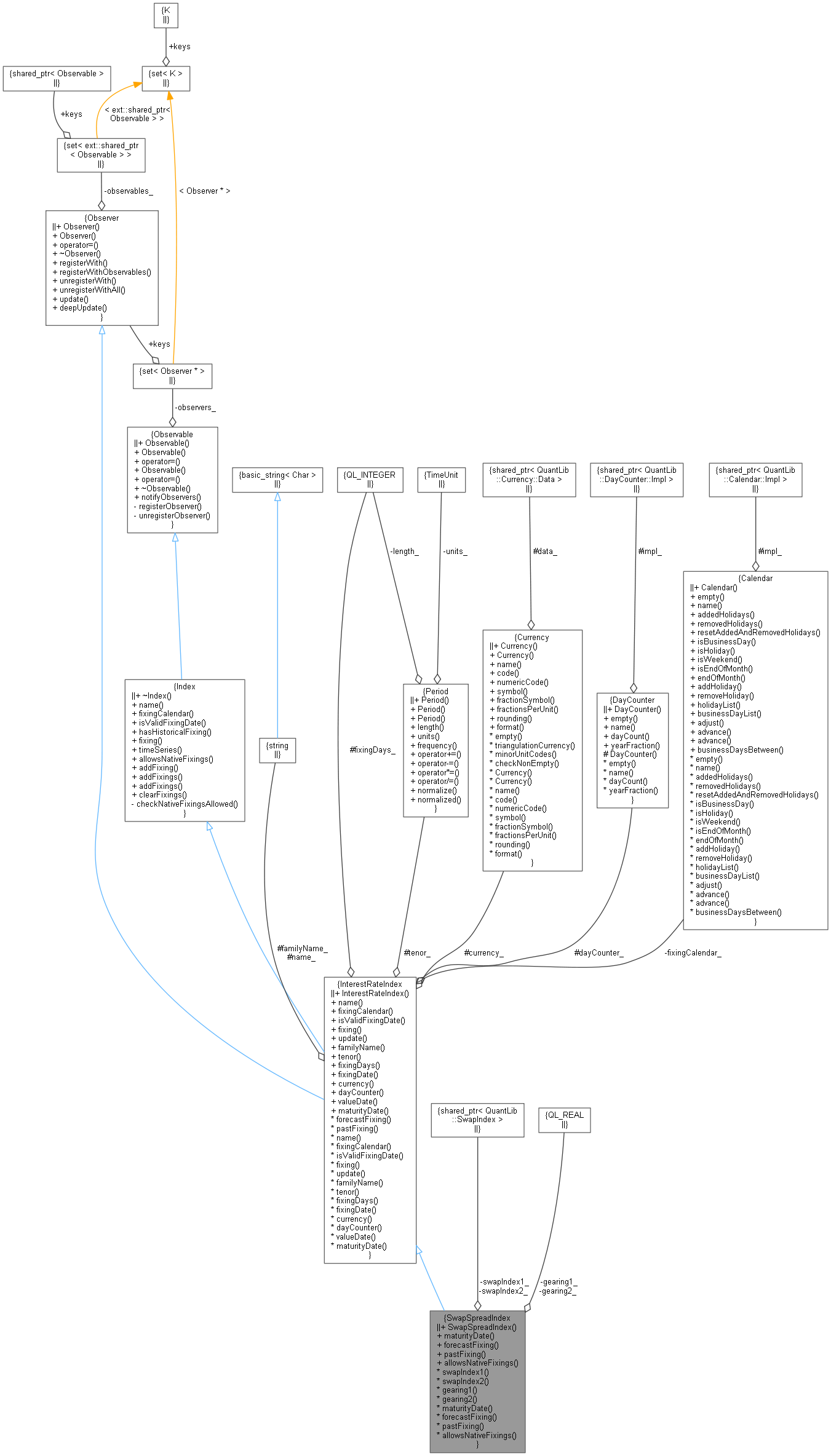

Inheritance diagram for SwapSpreadIndex: Collaboration diagram for SwapSpreadIndex:

Collaboration diagram for SwapSpreadIndex:

Public Member Functions | |

| SwapSpreadIndex (const std::string &familyName, const ext::shared_ptr< SwapIndex > &swapIndex1, ext::shared_ptr< SwapIndex > swapIndex2, Real gearing1=1.0, Real gearing2=-1.0) | |

InterestRateIndex interface | |

| Date | maturityDate (const Date &valueDate) const override |

| Rate | forecastFixing (const Date &fixingDate) const override |

| It can be overridden to implement particular conventions. More... | |

| Rate | pastFixing (const Date &fixingDate) const override |

| returns a past fixing at the given date More... | |

| bool | allowsNativeFixings () override |

| check if index allows for native fixings. More... | |

| Public Member Functions inherited from InterestRateIndex | |

| InterestRateIndex (std::string familyName, const Period &tenor, Natural settlementDays, Currency currency, Calendar fixingCalendar, DayCounter dayCounter) | |

| std::string | name () const override |

| Returns the name of the index. More... | |

| Calendar | fixingCalendar () const override |

| returns the calendar defining valid fixing dates More... | |

| bool | isValidFixingDate (const Date &fixingDate) const override |

| returns TRUE if the fixing date is a valid one More... | |

| Rate | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const override |

| returns the fixing at the given date More... | |

| std::string | familyName () const |

| Period | tenor () const |

| Natural | fixingDays () const |

| const Currency & | currency () const |

| const DayCounter & | dayCounter () const |

| virtual Date | fixingDate (const Date &valueDate) const |

| virtual Date | valueDate (const Date &fixingDate) const |

| Public Member Functions inherited from Index | |

| ~Index () override=default | |

| virtual std::string | name () const =0 |

| Returns the name of the index. More... | |

| virtual Calendar | fixingCalendar () const =0 |

| returns the calendar defining valid fixing dates More... | |

| virtual bool | isValidFixingDate (const Date &fixingDate) const =0 |

| returns TRUE if the fixing date is a valid one More... | |

| bool | hasHistoricalFixing (const Date &fixingDate) const |

| returns whether a historical fixing was stored for the given date More... | |

| virtual Real | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const =0 |

| returns the fixing at the given date More... | |

| virtual Real | pastFixing (const Date &fixingDate) const |

| returns a past fixing at the given date More... | |

| const TimeSeries< Real > & | timeSeries () const |

| returns the fixing TimeSeries More... | |

| virtual bool | allowsNativeFixings () |

| check if index allows for native fixings. More... | |

| void | update () override |

| virtual void | addFixing (const Date &fixingDate, Real fixing, bool forceOverwrite=false) |

| void | addFixings (const TimeSeries< Real > &t, bool forceOverwrite=false) |

| stores historical fixings from a TimeSeries More... | |

| template<class DateIterator , class ValueIterator > | |

| void | addFixings (DateIterator dBegin, DateIterator dEnd, ValueIterator vBegin, bool forceOverwrite=false) |

| stores historical fixings at the given dates More... | |

| void | clearFixings () |

| clears all stored historical fixings More... | |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

Inspectors | |

| ext::shared_ptr< SwapIndex > | swapIndex1_ |

| ext::shared_ptr< SwapIndex > | swapIndex2_ |

| Real | gearing1_ |

| Real | gearing2_ |

| ext::shared_ptr< SwapIndex > | swapIndex1 () |

| ext::shared_ptr< SwapIndex > | swapIndex2 () |

| Real | gearing1 () const |

| Real | gearing2 () const |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Member Functions inherited from Index | |

| ext::shared_ptr< Observable > | notifier () const |

| Protected Attributes inherited from InterestRateIndex | |

| std::string | familyName_ |

| Period | tenor_ |

| Natural | fixingDays_ |

| Currency | currency_ |

| DayCounter | dayCounter_ |

| std::string | name_ |

Detailed Description

class for swap-rate spread indexes

Definition at line 30 of file swapspreadindex.hpp.

Constructor & Destructor Documentation

◆ SwapSpreadIndex()

| SwapSpreadIndex | ( | const std::string & | familyName, |

| const ext::shared_ptr< SwapIndex > & | swapIndex1, | ||

| ext::shared_ptr< SwapIndex > | swapIndex2, | ||

| Real | gearing1 = 1.0, |

||

| Real | gearing2 = -1.0 |

||

| ) |

Member Function Documentation

◆ maturityDate()

Implements InterestRateIndex.

Definition at line 40 of file swapspreadindex.hpp.

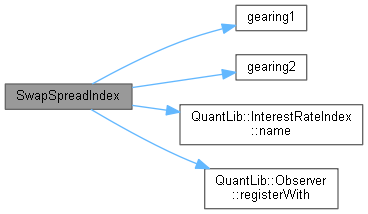

◆ forecastFixing()

It can be overridden to implement particular conventions.

Implements InterestRateIndex.

Definition at line 63 of file swapspreadindex.hpp.

Here is the call graph for this function:

◆ pastFixing()

returns a past fixing at the given date

the date passed as arguments must be the actual calendar date of the fixing; no settlement days must be used.

Reimplemented from Index.

Definition at line 71 of file swapspreadindex.hpp.

Here is the call graph for this function:

◆ allowsNativeFixings()

|

overridevirtual |

check if index allows for native fixings.

If this returns false, calls to addFixing and similar methods will raise an exception.

Reimplemented from Index.

Definition at line 45 of file swapspreadindex.hpp.

◆ swapIndex1()

| ext::shared_ptr< SwapIndex > swapIndex1 | ( | ) |

Definition at line 50 of file swapspreadindex.hpp.

◆ swapIndex2()

| ext::shared_ptr< SwapIndex > swapIndex2 | ( | ) |

Definition at line 51 of file swapspreadindex.hpp.

◆ gearing1()

| Real gearing1 | ( | ) | const |

◆ gearing2()

| Real gearing2 | ( | ) | const |

Member Data Documentation

◆ swapIndex1_

|

private |

Definition at line 58 of file swapspreadindex.hpp.

◆ swapIndex2_

|

private |

Definition at line 58 of file swapspreadindex.hpp.

◆ gearing1_

|

private |

Definition at line 59 of file swapspreadindex.hpp.

◆ gearing2_

|

private |

Definition at line 59 of file swapspreadindex.hpp.