Market-model evolver. More...

#include <evolver.hpp>

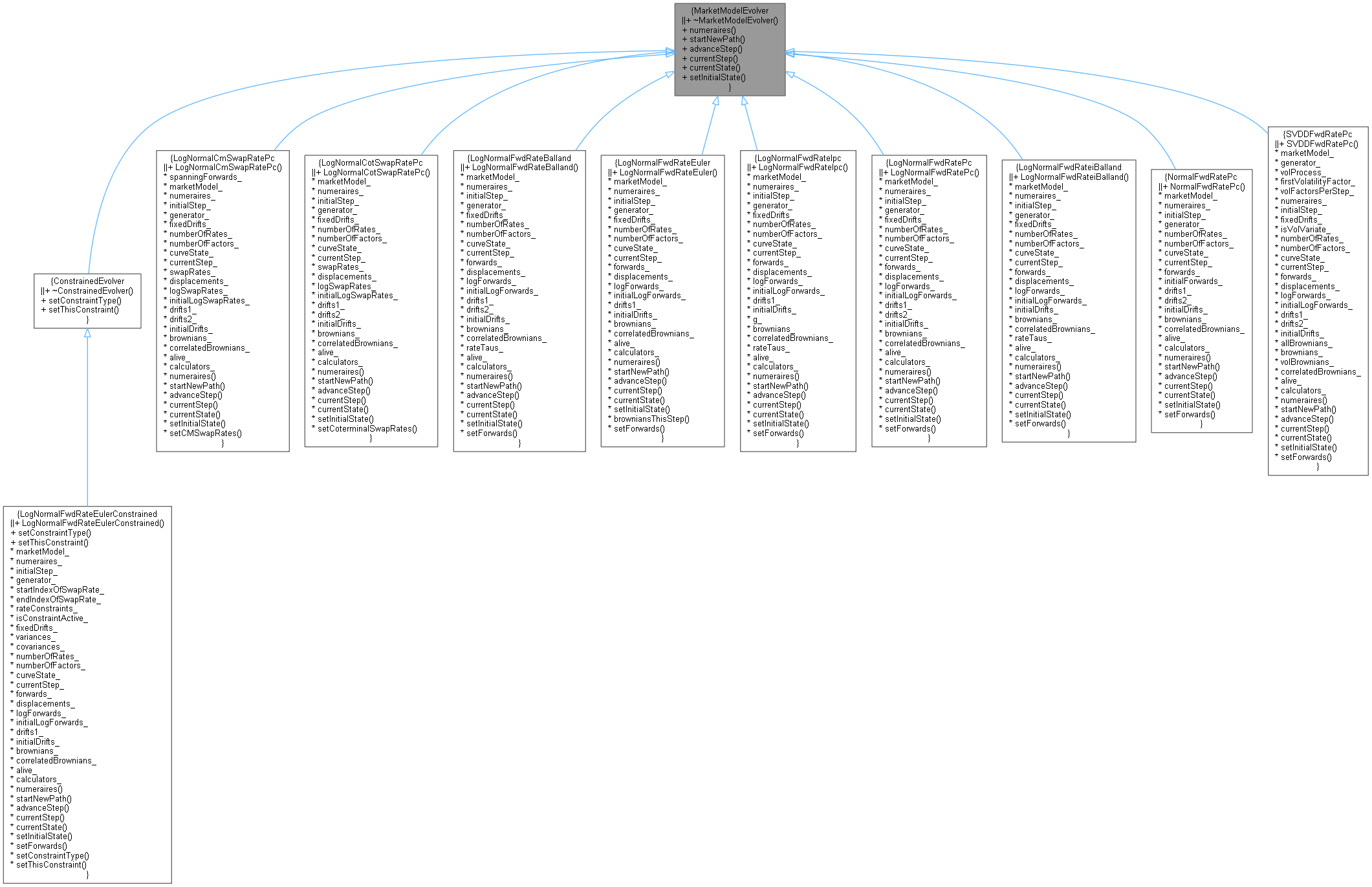

Inheritance diagram for MarketModelEvolver:

Inheritance diagram for MarketModelEvolver: Collaboration diagram for MarketModelEvolver:

Collaboration diagram for MarketModelEvolver:

Public Member Functions | |

| virtual | ~MarketModelEvolver ()=default |

| virtual const std::vector< Size > & | numeraires () const =0 |

| virtual Real | startNewPath ()=0 |

| virtual Real | advanceStep ()=0 |

| virtual Size | currentStep () const =0 |

| virtual const CurveState & | currentState () const =0 |

| virtual void | setInitialState (const CurveState &)=0 |

Detailed Description

Market-model evolver.

Abstract base class. The evolver does the actual gritty work of evolving the forward rates from one time to the next.

Definition at line 35 of file evolver.hpp.

Constructor & Destructor Documentation

◆ ~MarketModelEvolver()

|

virtualdefault |

Member Function Documentation

◆ numeraires()

|

pure virtual |

Implemented in LogNormalCmSwapRatePc, LogNormalCotSwapRatePc, LogNormalFwdRateBalland, LogNormalFwdRateEuler, LogNormalFwdRateEulerConstrained, LogNormalFwdRateiBalland, LogNormalFwdRateIpc, LogNormalFwdRatePc, NormalFwdRatePc, and SVDDFwdRatePc.

Here is the caller graph for this function:

◆ startNewPath()

|

pure virtual |

Implemented in LogNormalCmSwapRatePc, LogNormalCotSwapRatePc, LogNormalFwdRateBalland, LogNormalFwdRateEuler, LogNormalFwdRateEulerConstrained, LogNormalFwdRateiBalland, LogNormalFwdRateIpc, LogNormalFwdRatePc, NormalFwdRatePc, and SVDDFwdRatePc.

Here is the caller graph for this function:

◆ advanceStep()

|

pure virtual |

Implemented in LogNormalCmSwapRatePc, LogNormalCotSwapRatePc, LogNormalFwdRateBalland, LogNormalFwdRateEuler, LogNormalFwdRateEulerConstrained, LogNormalFwdRateiBalland, LogNormalFwdRateIpc, LogNormalFwdRatePc, NormalFwdRatePc, and SVDDFwdRatePc.

Here is the caller graph for this function:

◆ currentStep()

|

pure virtual |

Implemented in LogNormalCmSwapRatePc, LogNormalCotSwapRatePc, LogNormalFwdRateBalland, LogNormalFwdRateEuler, LogNormalFwdRateEulerConstrained, LogNormalFwdRateiBalland, LogNormalFwdRateIpc, LogNormalFwdRatePc, NormalFwdRatePc, and SVDDFwdRatePc.

Here is the caller graph for this function:

◆ currentState()

|

pure virtual |

Implemented in LogNormalCmSwapRatePc, LogNormalCotSwapRatePc, LogNormalFwdRateBalland, LogNormalFwdRateEuler, LogNormalFwdRateEulerConstrained, LogNormalFwdRateiBalland, LogNormalFwdRateIpc, LogNormalFwdRatePc, NormalFwdRatePc, and SVDDFwdRatePc.

Here is the caller graph for this function:

◆ setInitialState()

|

pure virtual |