Predictor-Corrector. More...

#include <ql/models/marketmodels/evolvers/lognormalcmswapratepc.hpp>

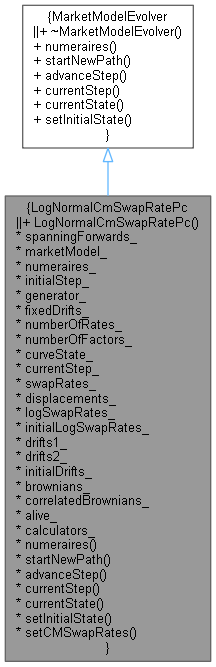

Inheritance diagram for LogNormalCmSwapRatePc:

Inheritance diagram for LogNormalCmSwapRatePc: Collaboration diagram for LogNormalCmSwapRatePc:

Collaboration diagram for LogNormalCmSwapRatePc:

Public Member Functions | |

| LogNormalCmSwapRatePc (Size spanningForwards, const ext::shared_ptr< MarketModel > &, const BrownianGeneratorFactory &, const std::vector< Size > &numeraires, Size initialStep=0) | |

| Public Member Functions inherited from MarketModelEvolver | |

| virtual | ~MarketModelEvolver ()=default |

| virtual const std::vector< Size > & | numeraires () const =0 |

| virtual Real | startNewPath ()=0 |

| virtual Real | advanceStep ()=0 |

| virtual Size | currentStep () const =0 |

| virtual const CurveState & | currentState () const =0 |

| virtual void | setInitialState (const CurveState &)=0 |

Detailed Description

Predictor-Corrector.

Definition at line 36 of file lognormalcmswapratepc.hpp.

Constructor & Destructor Documentation

◆ LogNormalCmSwapRatePc()

| LogNormalCmSwapRatePc | ( | Size | spanningForwards, |

| const ext::shared_ptr< MarketModel > & | marketModel, | ||

| const BrownianGeneratorFactory & | factory, | ||

| const std::vector< Size > & | numeraires, | ||

| Size | initialStep = 0 |

||

| ) |

Member Function Documentation

◆ numeraires()

|

overridevirtual |

Implements MarketModelEvolver.

Definition at line 77 of file lognormalcmswapratepc.cpp.

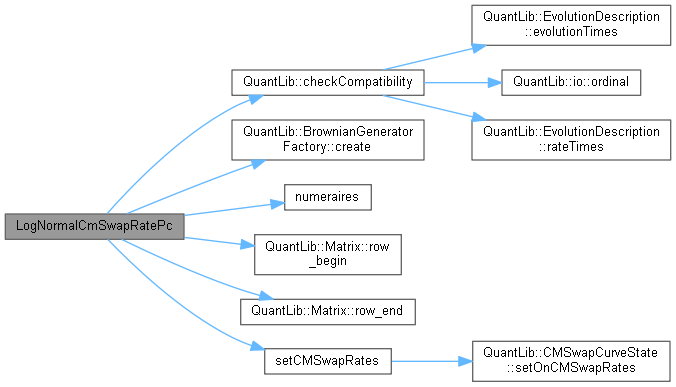

Here is the caller graph for this function:

◆ startNewPath()

|

overridevirtual |

Implements MarketModelEvolver.

Definition at line 98 of file lognormalcmswapratepc.cpp.

◆ advanceStep()

|

overridevirtual |

Implements MarketModelEvolver.

Definition at line 105 of file lognormalcmswapratepc.cpp.

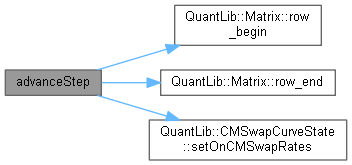

Here is the call graph for this function:

◆ currentStep()

|

overridevirtual |

Implements MarketModelEvolver.

Definition at line 151 of file lognormalcmswapratepc.cpp.

◆ currentState()

|

overridevirtual |

Implements MarketModelEvolver.

Definition at line 155 of file lognormalcmswapratepc.cpp.

◆ setInitialState()

|

overridevirtual |

Implements MarketModelEvolver.

Definition at line 92 of file lognormalcmswapratepc.cpp.

Here is the call graph for this function:

◆ setCMSwapRates()

|

private |

Definition at line 81 of file lognormalcmswapratepc.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ spanningForwards_

|

private |

Definition at line 55 of file lognormalcmswapratepc.hpp.

◆ marketModel_

|

private |

Definition at line 56 of file lognormalcmswapratepc.hpp.

◆ numeraires_

|

private |

Definition at line 57 of file lognormalcmswapratepc.hpp.

◆ initialStep_

|

private |

Definition at line 58 of file lognormalcmswapratepc.hpp.

◆ generator_

|

private |

Definition at line 59 of file lognormalcmswapratepc.hpp.

◆ fixedDrifts_

|

private |

Definition at line 61 of file lognormalcmswapratepc.hpp.

◆ numberOfRates_

|

private |

Definition at line 63 of file lognormalcmswapratepc.hpp.

◆ numberOfFactors_

|

private |

Definition at line 63 of file lognormalcmswapratepc.hpp.

◆ curveState_

|

private |

Definition at line 64 of file lognormalcmswapratepc.hpp.

◆ currentStep_

|

private |

Definition at line 65 of file lognormalcmswapratepc.hpp.

◆ swapRates_

|

private |

Definition at line 66 of file lognormalcmswapratepc.hpp.

◆ displacements_

|

private |

Definition at line 66 of file lognormalcmswapratepc.hpp.

◆ logSwapRates_

|

private |

Definition at line 66 of file lognormalcmswapratepc.hpp.

◆ initialLogSwapRates_

|

private |

Definition at line 66 of file lognormalcmswapratepc.hpp.

◆ drifts1_

|

private |

Definition at line 67 of file lognormalcmswapratepc.hpp.

◆ drifts2_

|

private |

Definition at line 67 of file lognormalcmswapratepc.hpp.

◆ initialDrifts_

|

private |

Definition at line 67 of file lognormalcmswapratepc.hpp.

◆ brownians_

|

private |

Definition at line 68 of file lognormalcmswapratepc.hpp.

◆ correlatedBrownians_

|

private |

Definition at line 68 of file lognormalcmswapratepc.hpp.

◆ alive_

|

private |

Definition at line 69 of file lognormalcmswapratepc.hpp.

◆ calculators_

|

private |

Definition at line 71 of file lognormalcmswapratepc.hpp.