Helper class building a sequence of capped/floored yoy inflation coupons. More...

#include <yoyinflationcoupon.hpp>

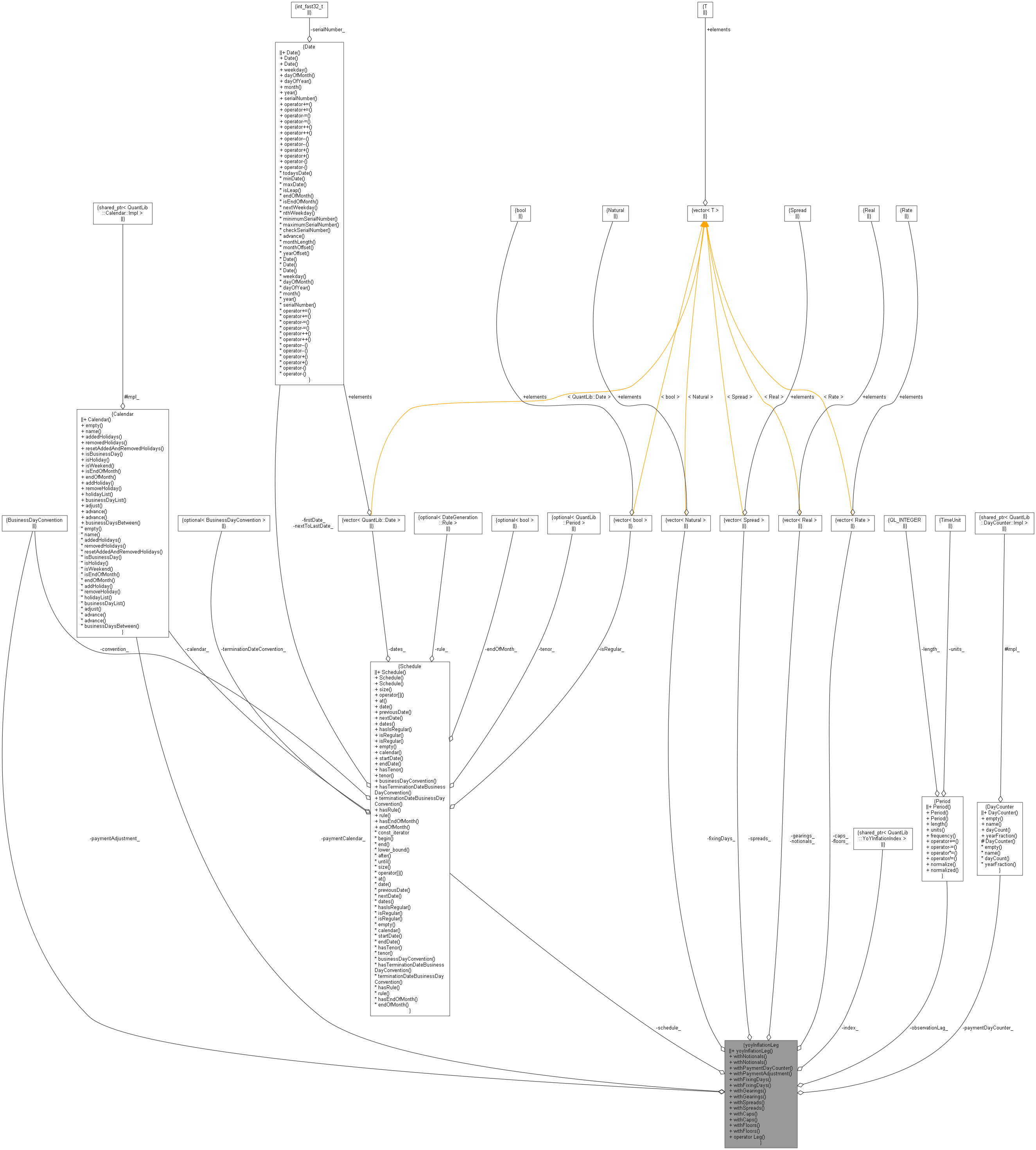

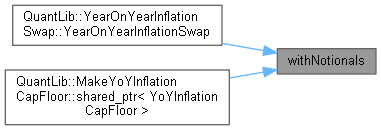

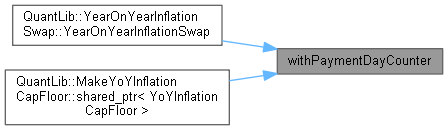

Collaboration diagram for yoyInflationLeg:

Collaboration diagram for yoyInflationLeg:

Private Attributes | |

| Schedule | schedule_ |

| ext::shared_ptr< YoYInflationIndex > | index_ |

| Period | observationLag_ |

| CPI::InterpolationType | interpolation_ |

| std::vector< Real > | notionals_ |

| DayCounter | paymentDayCounter_ |

| BusinessDayConvention | paymentAdjustment_ = ModifiedFollowing |

| Calendar | paymentCalendar_ |

| std::vector< Natural > | fixingDays_ |

| std::vector< Real > | gearings_ |

| std::vector< Spread > | spreads_ |

| std::vector< Rate > | caps_ |

| std::vector< Rate > | floors_ |

Detailed Description

Helper class building a sequence of capped/floored yoy inflation coupons.

Definition at line 114 of file yoyinflationcoupon.hpp.

Constructor & Destructor Documentation

◆ yoyInflationLeg() [1/2]

| yoyInflationLeg | ( | Schedule | schedule, |

| Calendar | cal, | ||

| ext::shared_ptr< YoYInflationIndex > | index, | ||

| const Period & | observationLag, | ||

| CPI::InterpolationType | interpolation | ||

| ) |

Definition at line 85 of file yoyinflationcoupon.cpp.

◆ yoyInflationLeg() [2/2]

| yoyInflationLeg | ( | Schedule | schedule, |

| Calendar | cal, | ||

| ext::shared_ptr< YoYInflationIndex > | index, | ||

| const Period & | observationLag | ||

| ) |

- Deprecated:

- Use the overload that passes an interpolation type instead. Deprecated in version 1.36.

Definition at line 93 of file yoyinflationcoupon.cpp.

Member Function Documentation

◆ withNotionals() [1/2]

| yoyInflationLeg & withNotionals | ( | Real | notional | ) |

◆ withNotionals() [2/2]

| yoyInflationLeg & withNotionals | ( | const std::vector< Real > & | notionals | ) |

Definition at line 105 of file yoyinflationcoupon.cpp.

◆ withPaymentDayCounter()

| yoyInflationLeg & withPaymentDayCounter | ( | const DayCounter & | dayCounter | ) |

◆ withPaymentAdjustment()

| yoyInflationLeg & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

◆ withFixingDays() [1/2]

| yoyInflationLeg & withFixingDays | ( | Natural | fixingDays | ) |

Definition at line 120 of file yoyinflationcoupon.cpp.

◆ withFixingDays() [2/2]

| yoyInflationLeg & withFixingDays | ( | const std::vector< Natural > & | fixingDays | ) |

Definition at line 125 of file yoyinflationcoupon.cpp.

◆ withGearings() [1/2]

| yoyInflationLeg & withGearings | ( | Real | gearing | ) |

Definition at line 130 of file yoyinflationcoupon.cpp.

◆ withGearings() [2/2]

| yoyInflationLeg & withGearings | ( | const std::vector< Real > & | gearings | ) |

Definition at line 135 of file yoyinflationcoupon.cpp.

◆ withSpreads() [1/2]

| yoyInflationLeg & withSpreads | ( | Spread | spread | ) |

◆ withSpreads() [2/2]

| yoyInflationLeg & withSpreads | ( | const std::vector< Spread > & | spreads | ) |

Definition at line 145 of file yoyinflationcoupon.cpp.

◆ withCaps() [1/2]

| yoyInflationLeg & withCaps | ( | Rate | cap | ) |

Definition at line 150 of file yoyinflationcoupon.cpp.

◆ withCaps() [2/2]

| yoyInflationLeg & withCaps | ( | const std::vector< Rate > & | caps | ) |

Definition at line 155 of file yoyinflationcoupon.cpp.

◆ withFloors() [1/2]

| yoyInflationLeg & withFloors | ( | Rate | floor | ) |

Definition at line 160 of file yoyinflationcoupon.cpp.

◆ withFloors() [2/2]

| yoyInflationLeg & withFloors | ( | const std::vector< Rate > & | floors | ) |

Definition at line 165 of file yoyinflationcoupon.cpp.

◆ operator Leg()

| operator Leg | ( | ) | const |

Member Data Documentation

◆ schedule_

|

private |

Definition at line 145 of file yoyinflationcoupon.hpp.

◆ index_

|

private |

Definition at line 146 of file yoyinflationcoupon.hpp.

◆ observationLag_

|

private |

Definition at line 147 of file yoyinflationcoupon.hpp.

◆ interpolation_

|

private |

Definition at line 148 of file yoyinflationcoupon.hpp.

◆ notionals_

|

private |

Definition at line 149 of file yoyinflationcoupon.hpp.

◆ paymentDayCounter_

|

private |

Definition at line 150 of file yoyinflationcoupon.hpp.

◆ paymentAdjustment_

|

private |

Definition at line 151 of file yoyinflationcoupon.hpp.

◆ paymentCalendar_

|

private |

Definition at line 152 of file yoyinflationcoupon.hpp.

◆ fixingDays_

|

private |

Definition at line 153 of file yoyinflationcoupon.hpp.

◆ gearings_

|

private |

Definition at line 154 of file yoyinflationcoupon.hpp.

◆ spreads_

|

private |

Definition at line 155 of file yoyinflationcoupon.hpp.

◆ caps_

|

private |

Definition at line 156 of file yoyinflationcoupon.hpp.

◆ floors_

|

private |

Definition at line 156 of file yoyinflationcoupon.hpp.