#include <alphafinder.hpp>

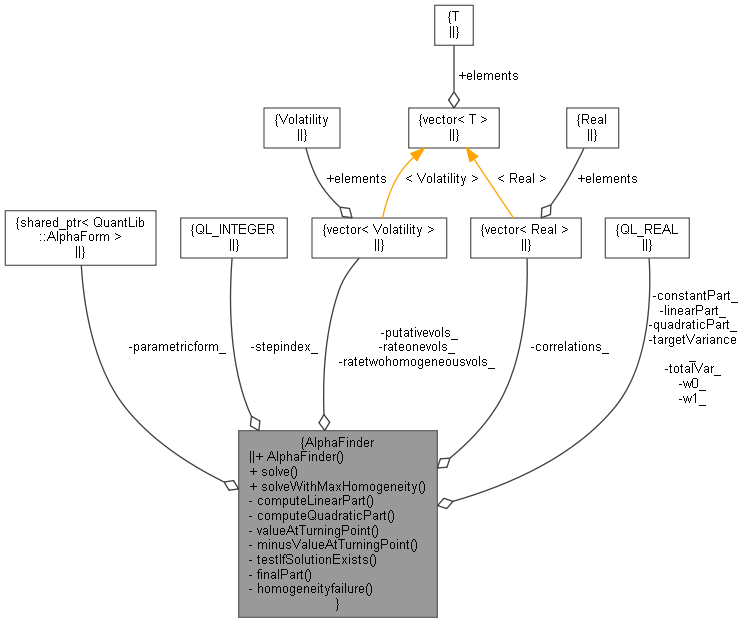

Collaboration diagram for AlphaFinder:

Collaboration diagram for AlphaFinder:

Public Member Functions | |

| AlphaFinder (ext::shared_ptr< AlphaForm > parametricform) | |

| bool | solve (Real alpha0, Integer stepindex, const std::vector< Volatility > &rateonevols, const std::vector< Volatility > &ratetwohomogeneousvols, const std::vector< Real > &correlations, Real w0, Real w1, Real targetVariance, Real tolerance, Real alphaMax, Real alphaMin, Integer steps, Real &alpha, Real &a, Real &b, std::vector< Volatility > &ratetwovols) |

| bool | solveWithMaxHomogeneity (Real alpha0, Integer stepindex, const std::vector< Volatility > &rateonevols, const std::vector< Volatility > &ratetwohomogeneousvols, const std::vector< Real > &correlations, Real w0, Real w1, Real targetVariance, Real tolerance, Real alphaMax, Real alphaMin, Integer steps, Real &alpha, Real &a, Real &b, std::vector< Volatility > &ratetwovols) |

Private Member Functions | |

| Real | computeLinearPart (Real alpha) |

| Real | computeQuadraticPart (Real alpha) |

| Real | valueAtTurningPoint (Real alpha) |

| Real | minusValueAtTurningPoint (Real alpha) |

| bool | testIfSolutionExists (Real alpha) |

| bool | finalPart (Real alphaFound, Integer stepindex, const std::vector< Volatility > &ratetwohomogeneousvols, Real quadraticPart, Real linearPart, Real constantPart, Real &alpha, Real &a, Real &b, std::vector< Volatility > &ratetwovols) |

| Real | homogeneityfailure (Real alpha) |

Private Attributes | |

| ext::shared_ptr< AlphaForm > | parametricform_ |

| Integer | stepindex_ |

| std::vector< Volatility > | rateonevols_ |

| std::vector< Volatility > | ratetwohomogeneousvols_ |

| std::vector< Volatility > | putativevols_ |

| std::vector< Real > | correlations_ |

| Real | w0_ |

| Real | w1_ |

| Real | constantPart_ |

| Real | linearPart_ |

| Real | quadraticPart_ |

| Real | totalVar_ |

| Real | targetVariance_ |

Detailed Description

Definition at line 29 of file alphafinder.hpp.

Constructor & Destructor Documentation

◆ AlphaFinder()

| AlphaFinder | ( | ext::shared_ptr< AlphaForm > | parametricform | ) |

Definition at line 179 of file alphafinder.cpp.

Member Function Documentation

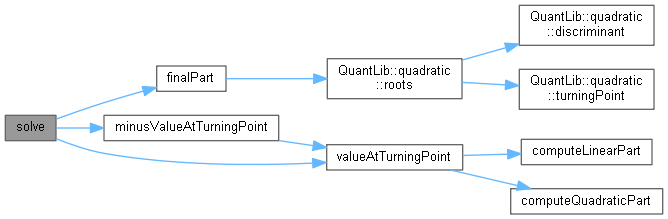

◆ solve()

| bool solve | ( | Real | alpha0, |

| Integer | stepindex, | ||

| const std::vector< Volatility > & | rateonevols, | ||

| const std::vector< Volatility > & | ratetwohomogeneousvols, | ||

| const std::vector< Real > & | correlations, | ||

| Real | w0, | ||

| Real | w1, | ||

| Real | targetVariance, | ||

| Real | tolerance, | ||

| Real | alphaMax, | ||

| Real | alphaMin, | ||

| Integer | steps, | ||

| Real & | alpha, | ||

| Real & | a, | ||

| Real & | b, | ||

| std::vector< Volatility > & | ratetwovols | ||

| ) |

Definition at line 297 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

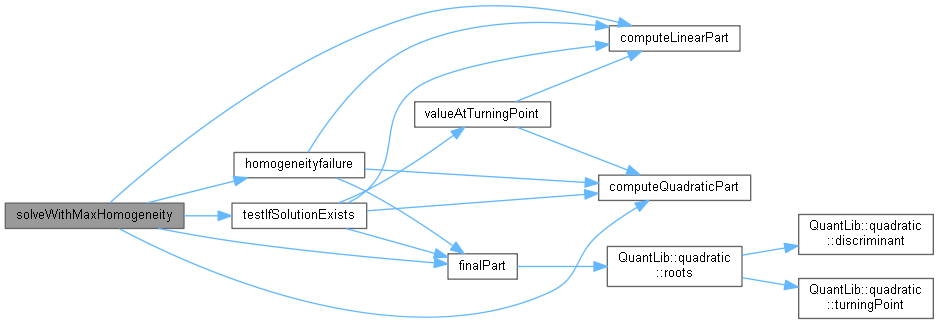

◆ solveWithMaxHomogeneity()

| bool solveWithMaxHomogeneity | ( | Real | alpha0, |

| Integer | stepindex, | ||

| const std::vector< Volatility > & | rateonevols, | ||

| const std::vector< Volatility > & | ratetwohomogeneousvols, | ||

| const std::vector< Real > & | correlations, | ||

| Real | w0, | ||

| Real | w1, | ||

| Real | targetVariance, | ||

| Real | tolerance, | ||

| Real | alphaMax, | ||

| Real | alphaMin, | ||

| Integer | steps, | ||

| Real & | alpha, | ||

| Real & | a, | ||

| Real & | b, | ||

| std::vector< Volatility > & | ratetwovols | ||

| ) |

Definition at line 418 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ computeLinearPart()

◆ computeQuadraticPart()

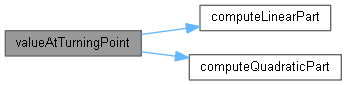

◆ valueAtTurningPoint()

Definition at line 265 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ minusValueAtTurningPoint()

Definition at line 275 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

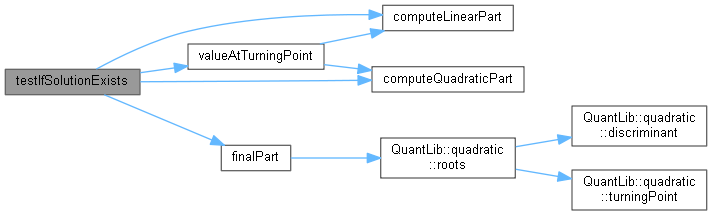

◆ testIfSolutionExists()

Definition at line 279 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

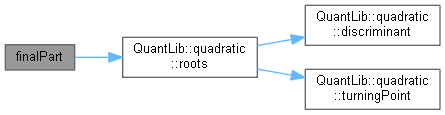

◆ finalPart()

|

private |

Definition at line 232 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

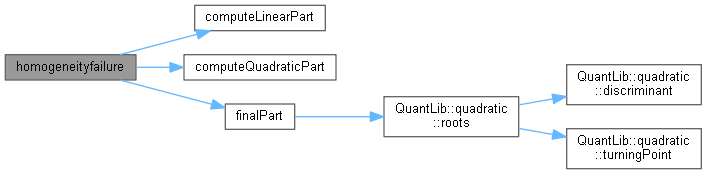

◆ homogeneityfailure()

Definition at line 210 of file alphafinder.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ parametricform_

|

private |

Definition at line 84 of file alphafinder.hpp.

◆ stepindex_

|

private |

Definition at line 85 of file alphafinder.hpp.

◆ rateonevols_

|

private |

Definition at line 86 of file alphafinder.hpp.

◆ ratetwohomogeneousvols_

|

private |

Definition at line 86 of file alphafinder.hpp.

◆ putativevols_

|

private |

Definition at line 87 of file alphafinder.hpp.

◆ correlations_

|

private |

Definition at line 88 of file alphafinder.hpp.

◆ w0_

|

private |

Definition at line 89 of file alphafinder.hpp.

◆ w1_

|

private |

Definition at line 89 of file alphafinder.hpp.

◆ constantPart_

|

private |

Definition at line 90 of file alphafinder.hpp.

◆ linearPart_

|

private |

Definition at line 90 of file alphafinder.hpp.

◆ quadraticPart_

|

private |

Definition at line 90 of file alphafinder.hpp.

◆ totalVar_

|

private |

Definition at line 91 of file alphafinder.hpp.

◆ targetVariance_

|

private |

Definition at line 91 of file alphafinder.hpp.