GARCH volatility model. More...

#include <garch.hpp>

Inheritance diagram for Garch11:

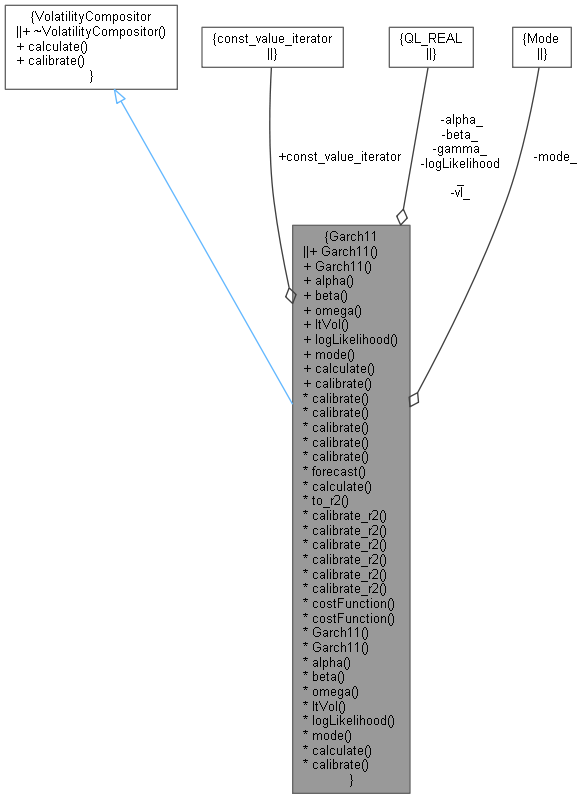

Inheritance diagram for Garch11: Collaboration diagram for Garch11:

Collaboration diagram for Garch11:

Public Types | |

| enum | Mode { MomentMatchingGuess , GammaGuess , BestOfTwo , DoubleOptimization } |

| typedef TimeSeries< Volatility > | time_series |

| Public Types inherited from VolatilityCompositor | |

| typedef TimeSeries< Volatility > | time_series |

Public Member Functions | |

Constructors | |

| Garch11 (Real a, Real b, Real vl) | |

| Garch11 (const time_series &qs, Mode mode=BestOfTwo) | |

Inspectors | |

| Real | alpha () const |

| Real | beta () const |

| Real | omega () const |

| Real | ltVol () const |

| Real | logLikelihood () const |

| Mode | mode () const |

VolatilityCompositor interface | |

| time_series | calculate (const time_series "eSeries) override |

| void | calibrate (const time_series "eSeries) override |

| Public Member Functions inherited from VolatilityCompositor | |

| virtual | ~VolatilityCompositor ()=default |

| virtual time_series | calculate (const time_series &volatilitySeries)=0 |

| virtual void | calibrate (const time_series &volatilitySeries)=0 |

Additional interface | |

| Real | alpha_ |

| Real | beta_ |

| Real | gamma_ |

| Real | vl_ |

| Real | logLikelihood_ |

| Mode | mode_ |

| void | calibrate (const time_series "eSeries, OptimizationMethod &method, const EndCriteria &endCriteria) |

| void | calibrate (const time_series "eSeries, OptimizationMethod &method, const EndCriteria &endCriteria, const Array &initialGuess) |

| template<typename ForwardIterator > | |

| void | calibrate (ForwardIterator begin, ForwardIterator end) |

| template<typename ForwardIterator > | |

| void | calibrate (ForwardIterator begin, ForwardIterator end, OptimizationMethod &method, EndCriteria endCriteria) |

| template<typename ForwardIterator > | |

| void | calibrate (ForwardIterator begin, ForwardIterator end, OptimizationMethod &method, EndCriteria endCriteria, const Array &initialGuess) |

| Real | forecast (Real r, Real sigma2) const |

| static time_series | calculate (const time_series "eSeries, Real alpha, Real beta, Real omega) |

| template<typename InputIterator > | |

| static Real | to_r2 (InputIterator begin, InputIterator end, std::vector< Volatility > &r2) |

| static ext::shared_ptr< Problem > | calibrate_r2 (Mode mode, const std::vector< Volatility > &r2, Real mean_r2, Real &alpha, Real &beta, Real &omega) |

| static ext::shared_ptr< Problem > | calibrate_r2 (Mode mode, const std::vector< Volatility > &r2, Real mean_r2, OptimizationMethod &method, const EndCriteria &endCriteria, Real &alpha, Real &beta, Real &omega) |

| static ext::shared_ptr< Problem > | calibrate_r2 (const std::vector< Volatility > &r2, Real mean_r2, OptimizationMethod &method, const EndCriteria &endCriteria, const Array &initialGuess, Real &alpha, Real &beta, Real &omega) |

| static ext::shared_ptr< Problem > | calibrate_r2 (const std::vector< Volatility > &r2, OptimizationMethod &method, const EndCriteria &endCriteria, const Array &initialGuess, Real &alpha, Real &beta, Real &omega) |

| static ext::shared_ptr< Problem > | calibrate_r2 (const std::vector< Volatility > &r2, Real mean_r2, OptimizationMethod &method, Constraint &constraints, const EndCriteria &endCriteria, const Array &initialGuess, Real &alpha, Real &beta, Real &omega) |

| static ext::shared_ptr< Problem > | calibrate_r2 (const std::vector< Volatility > &r2, OptimizationMethod &method, Constraint &constraints, const EndCriteria &endCriteria, const Array &initialGuess, Real &alpha, Real &beta, Real &omega) |

| template<class InputIterator > | |

| static Real | costFunction (InputIterator begin, InputIterator end, Real alpha, Real beta, Real omega) |

| template<class InputIterator > | |

| Real | costFunction (InputIterator begin, InputIterator end) const |

Detailed Description

GARCH volatility model.

Volatilities are assumed to be expressed on an annual basis.

Member Typedef Documentation

◆ time_series

| typedef TimeSeries<Volatility> time_series |

Member Enumeration Documentation

◆ Mode

| enum Mode |

Constructor & Destructor Documentation

◆ Garch11() [1/2]

◆ Garch11() [2/2]

| Garch11 | ( | const time_series & | qs, |

| Mode | mode = BestOfTwo |

||

| ) |

Member Function Documentation

◆ alpha()

| Real alpha | ( | ) | const |

◆ beta()

| Real beta | ( | ) | const |

◆ omega()

| Real omega | ( | ) | const |

◆ ltVol()

◆ logLikelihood()

◆ mode()

◆ calculate() [1/2]

|

overridevirtual |

Implements VolatilityCompositor.

Definition at line 78 of file garch.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ calibrate() [1/6]

|

overridevirtual |

Implements VolatilityCompositor.

Definition at line 81 of file garch.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ calculate() [2/2]

|

static |

◆ calibrate() [2/6]

| void calibrate | ( | const time_series & | quoteSeries, |

| OptimizationMethod & | method, | ||

| const EndCriteria & | endCriteria | ||

| ) |

◆ calibrate() [3/6]

| void calibrate | ( | const time_series & | quoteSeries, |

| OptimizationMethod & | method, | ||

| const EndCriteria & | endCriteria, | ||

| const Array & | initialGuess | ||

| ) |

◆ calibrate() [4/6]

| void calibrate | ( | ForwardIterator | begin, |

| ForwardIterator | end | ||

| ) |

◆ calibrate() [5/6]

| void calibrate | ( | ForwardIterator | begin, |

| ForwardIterator | end, | ||

| OptimizationMethod & | method, | ||

| EndCriteria | endCriteria | ||

| ) |

◆ calibrate() [6/6]

| void calibrate | ( | ForwardIterator | begin, |

| ForwardIterator | end, | ||

| OptimizationMethod & | method, | ||

| EndCriteria | endCriteria, | ||

| const Array & | initialGuess | ||

| ) |

◆ forecast()

◆ to_r2()

|

static |

◆ calibrate_r2() [1/6]

◆ calibrate_r2() [2/6]

|

static |

◆ calibrate_r2() [3/6]

|

static |

◆ calibrate_r2() [4/6]

|

static |

◆ calibrate_r2() [5/6]

|

static |

◆ calibrate_r2() [6/6]

|

static |

◆ costFunction() [1/2]

◆ costFunction() [2/2]

|

private |