#include <volatilitymodel.hpp>

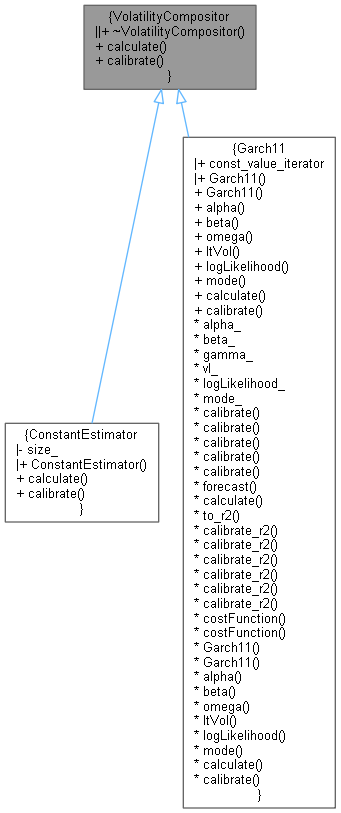

Inheritance diagram for VolatilityCompositor:

Inheritance diagram for VolatilityCompositor: Collaboration diagram for VolatilityCompositor:

Collaboration diagram for VolatilityCompositor:

Public Types | |

| typedef TimeSeries< Volatility > | time_series |

Public Member Functions | |

| virtual | ~VolatilityCompositor ()=default |

| virtual time_series | calculate (const time_series &volatilitySeries)=0 |

| virtual void | calibrate (const time_series &volatilitySeries)=0 |

Detailed Description

Definition at line 41 of file volatilitymodel.hpp.

Member Typedef Documentation

◆ time_series

| typedef TimeSeries<Volatility> time_series |

Definition at line 43 of file volatilitymodel.hpp.

Constructor & Destructor Documentation

◆ ~VolatilityCompositor()

|

virtualdefault |

Member Function Documentation

◆ calculate()

|

pure virtual |

Implemented in Garch11.

◆ calibrate()

|

pure virtual |

Implemented in Garch11.