helper class More...

#include <makeois.hpp>

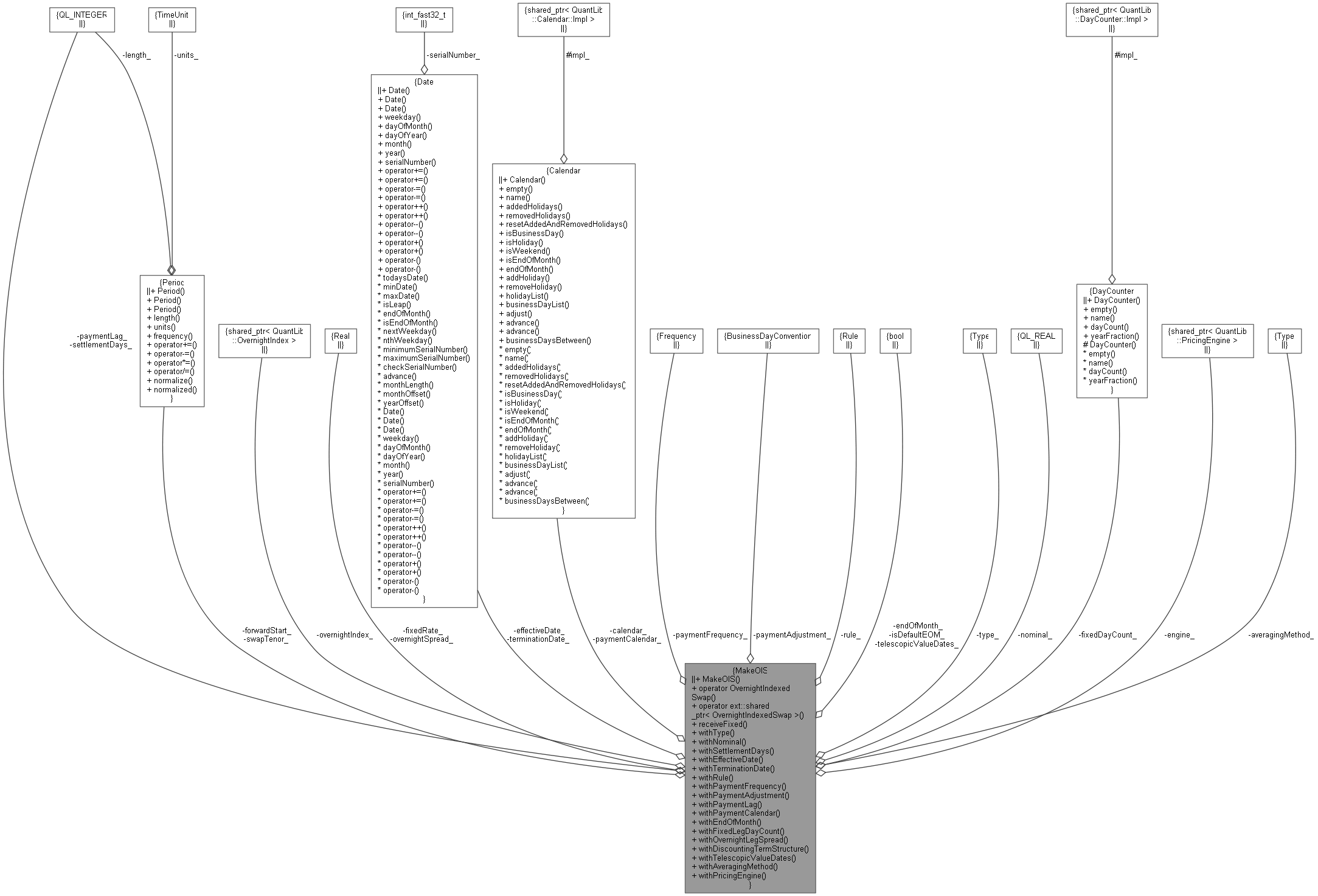

Collaboration diagram for MakeOIS:

Collaboration diagram for MakeOIS:

Detailed Description

helper class

This class provides a more comfortable way to instantiate overnight indexed swaps.

Definition at line 39 of file makeois.hpp.

Constructor & Destructor Documentation

◆ MakeOIS()

| MakeOIS | ( | const Period & | swapTenor, |

| const ext::shared_ptr< OvernightIndex > & | overnightIndex, | ||

| Rate | fixedRate = Null<Rate>(), |

||

| const Period & | fwdStart = 0*Days |

||

| ) |

Definition at line 30 of file makeois.cpp.

Member Function Documentation

◆ operator OvernightIndexedSwap()

| operator OvernightIndexedSwap | ( | ) | const |

Definition at line 40 of file makeois.cpp.

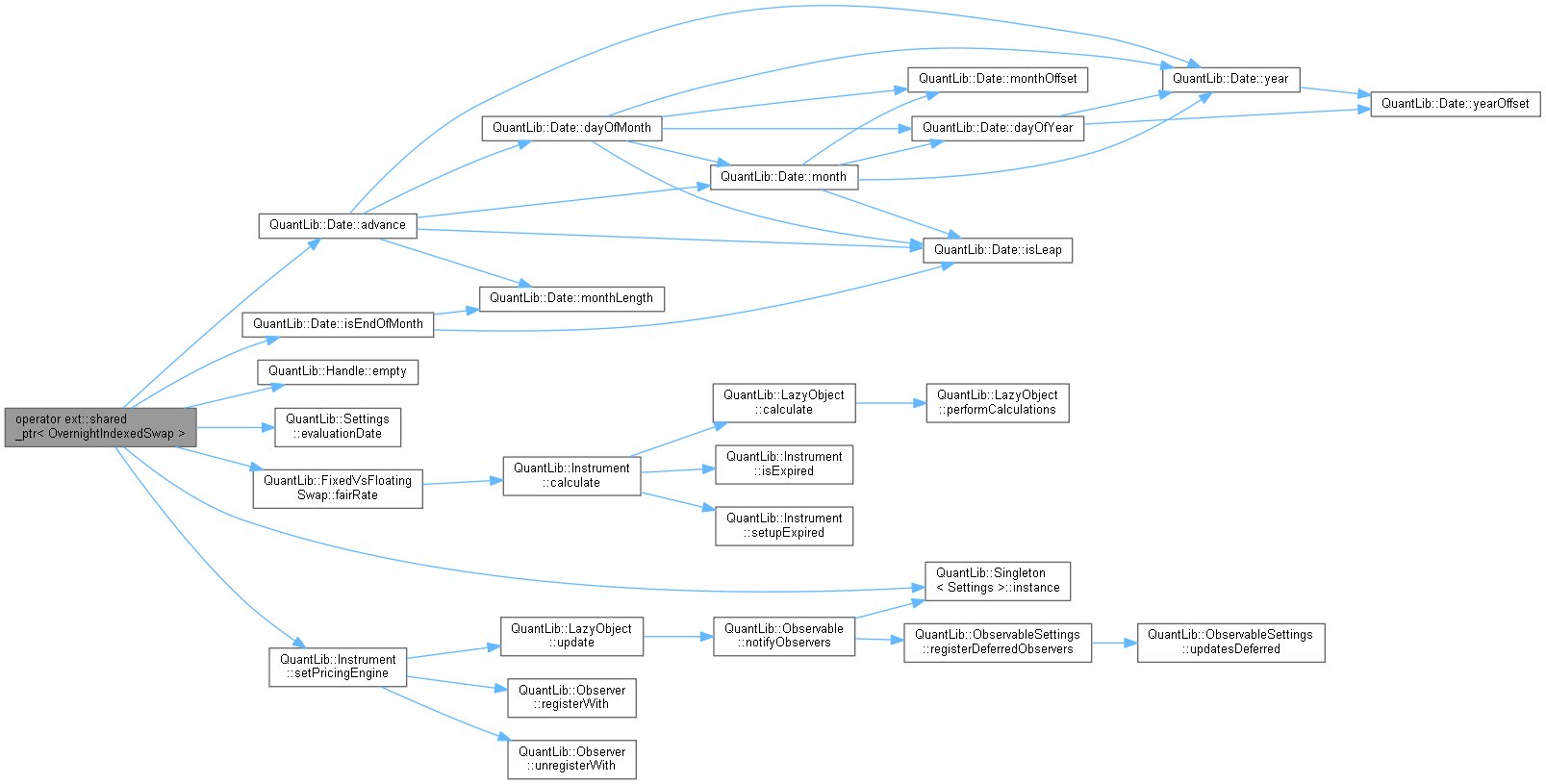

◆ operator ext::shared_ptr< OvernightIndexedSwap >()

| operator ext::shared_ptr< OvernightIndexedSwap > | ( | ) | const |

◆ receiveFixed()

Definition at line 167 of file makeois.cpp.

◆ withType()

| MakeOIS & withType | ( | Swap::Type | type | ) |

◆ withNominal()

◆ withSettlementDays()

◆ withEffectiveDate()

◆ withTerminationDate()

◆ withRule()

| MakeOIS & withRule | ( | DateGeneration::Rule | r | ) |

Definition at line 243 of file makeois.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ withFixedLegRule()

| MakeOIS & withFixedLegRule | ( | DateGeneration::Rule | r | ) |

◆ withOvernightLegRule()

| MakeOIS & withOvernightLegRule | ( | DateGeneration::Rule | r | ) |

◆ withPaymentFrequency()

Definition at line 200 of file makeois.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ withFixedLegPaymentFrequency()

◆ withOvernightLegPaymentFrequency()

◆ withPaymentAdjustment()

| MakeOIS & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

◆ withPaymentLag()

◆ withPaymentCalendar()

◆ withCalendar()

◆ withFixedLegCalendar()

◆ withOvernightLegCalendar()

◆ withConvention()

| MakeOIS & withConvention | ( | BusinessDayConvention | bdc | ) |

◆ withFixedLegConvention()

| MakeOIS & withFixedLegConvention | ( | BusinessDayConvention | bdc | ) |

◆ withOvernightLegConvention()

| MakeOIS & withOvernightLegConvention | ( | BusinessDayConvention | bdc | ) |

◆ withTerminationDateConvention()

| MakeOIS & withTerminationDateConvention | ( | BusinessDayConvention | bdc | ) |

◆ withFixedLegTerminationDateConvention()

| MakeOIS & withFixedLegTerminationDateConvention | ( | BusinessDayConvention | bdc | ) |

◆ withOvernightLegTerminationDateConvention()

| MakeOIS & withOvernightLegTerminationDateConvention | ( | BusinessDayConvention | bdc | ) |

◆ withEndOfMonth()

Definition at line 305 of file makeois.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ withFixedLegEndOfMonth()

◆ withOvernightLegEndOfMonth()

◆ withFixedLegDayCount()

| MakeOIS & withFixedLegDayCount | ( | const DayCounter & | dc | ) |

◆ withOvernightLegSpread()

Definition at line 321 of file makeois.cpp.

◆ withDiscountingTermStructure()

| MakeOIS & withDiscountingTermStructure | ( | const Handle< YieldTermStructure > & | discountingTermStructure | ) |

◆ withTelescopicValueDates()

◆ withAveragingMethod()

| MakeOIS & withAveragingMethod | ( | RateAveraging::Type | averagingMethod | ) |

◆ withLookbackDays()

◆ withLockoutDays()

◆ withObservationShift()

◆ withPricingEngine()

| MakeOIS & withPricingEngine | ( | const ext::shared_ptr< PricingEngine > & | engine | ) |

Definition at line 265 of file makeois.cpp.

Member Data Documentation

◆ swapTenor_

|

private |

Definition at line 98 of file makeois.hpp.

◆ overnightIndex_

|

private |

Definition at line 99 of file makeois.hpp.

◆ fixedRate_

|

private |

Definition at line 100 of file makeois.hpp.

◆ forwardStart_

|

private |

Definition at line 101 of file makeois.hpp.

◆ settlementDays_

|

private |

Definition at line 103 of file makeois.hpp.

◆ effectiveDate_

|

private |

Definition at line 104 of file makeois.hpp.

◆ terminationDate_

|

private |

Definition at line 104 of file makeois.hpp.

◆ fixedCalendar_

|

private |

Definition at line 105 of file makeois.hpp.

◆ overnightCalendar_

|

private |

Definition at line 105 of file makeois.hpp.

◆ fixedPaymentFrequency_

Definition at line 107 of file makeois.hpp.

◆ overnightPaymentFrequency_

Definition at line 108 of file makeois.hpp.

◆ paymentCalendar_

|

private |

Definition at line 109 of file makeois.hpp.

◆ paymentAdjustment_

|

private |

Definition at line 110 of file makeois.hpp.

◆ paymentLag_

|

private |

Definition at line 111 of file makeois.hpp.

◆ fixedConvention_

|

private |

Definition at line 113 of file makeois.hpp.

◆ fixedTerminationDateConvention_

|

private |

Definition at line 114 of file makeois.hpp.

◆ overnightConvention_

|

private |

Definition at line 115 of file makeois.hpp.

◆ overnightTerminationDateConvention_

|

private |

Definition at line 116 of file makeois.hpp.

◆ fixedRule_

|

private |

Definition at line 117 of file makeois.hpp.

◆ overnightRule_

|

private |

Definition at line 118 of file makeois.hpp.

◆ fixedEndOfMonth_

|

private |

Definition at line 119 of file makeois.hpp.

◆ overnightEndOfMonth_

|

private |

Definition at line 119 of file makeois.hpp.

◆ isDefaultEOM_

|

private |

Definition at line 119 of file makeois.hpp.

◆ type_

|

private |

Definition at line 121 of file makeois.hpp.

◆ nominal_

|

private |

Definition at line 122 of file makeois.hpp.

◆ overnightSpread_

|

private |

Definition at line 124 of file makeois.hpp.

◆ fixedDayCount_

|

private |

Definition at line 125 of file makeois.hpp.

◆ engine_

|

private |

Definition at line 127 of file makeois.hpp.

◆ telescopicValueDates_

|

private |

Definition at line 129 of file makeois.hpp.

◆ averagingMethod_

|

private |

Definition at line 130 of file makeois.hpp.

◆ lookbackDays_

Definition at line 131 of file makeois.hpp.

◆ lockoutDays_

|

private |

Definition at line 132 of file makeois.hpp.

◆ applyObservationShift_

|

private |

Definition at line 133 of file makeois.hpp.