Statistic tool for sequences with discrepancy calculation. More...

#include <discrepancystatistics.hpp>

Inheritance diagram for DiscrepancyStatistics:

Inheritance diagram for DiscrepancyStatistics: Collaboration diagram for DiscrepancyStatistics:

Collaboration diagram for DiscrepancyStatistics:

Public Types | |

| typedef SequenceStatistics::value_type | value_type |

| Public Types inherited from GenericSequenceStatistics< StatisticsType > | |

| typedef StatisticsType | statistics_type |

| typedef std::vector< typename StatisticsType::value_type > | value_type |

Public Member Functions | |

| DiscrepancyStatistics (Size dimension) | |

| Public Member Functions inherited from GenericSequenceStatistics< StatisticsType > | |

| GenericSequenceStatistics (Size dimension=0) | |

| Size | size () const |

| Matrix | covariance () const |

| returns the covariance Matrix More... | |

| Matrix | correlation () const |

| returns the correlation Matrix More... | |

| Size | samples () const |

| Real | weightSum () const |

| std::vector< Real > | mean () const |

| std::vector< Real > | variance () const |

| std::vector< Real > | standardDeviation () const |

| std::vector< Real > | downsideVariance () const |

| std::vector< Real > | downsideDeviation () const |

| std::vector< Real > | semiVariance () const |

| std::vector< Real > | semiDeviation () const |

| std::vector< Real > | errorEstimate () const |

| std::vector< Real > | skewness () const |

| std::vector< Real > | kurtosis () const |

| std::vector< Real > | min () const |

| std::vector< Real > | max () const |

| std::vector< Real > | gaussianPercentile (Real y) const |

| std::vector< Real > | percentile (Real y) const |

| std::vector< Real > | gaussianPotentialUpside (Real percentile) const |

| std::vector< Real > | potentialUpside (Real percentile) const |

| std::vector< Real > | gaussianValueAtRisk (Real percentile) const |

| std::vector< Real > | valueAtRisk (Real percentile) const |

| std::vector< Real > | gaussianExpectedShortfall (Real percentile) const |

| std::vector< Real > | expectedShortfall (Real percentile) const |

| std::vector< Real > | regret (Real target) const |

| std::vector< Real > | gaussianShortfall (Real target) const |

| std::vector< Real > | shortfall (Real target) const |

| std::vector< Real > | gaussianAverageShortfall (Real target) const |

| std::vector< Real > | averageShortfall (Real target) const |

| void | reset (Size dimension=0) |

| template<class Sequence > | |

| void | add (const Sequence &sample, Real weight=1.0) |

| template<class Iterator > | |

| void | add (Iterator begin, Iterator end, Real weight=1.0) |

1-dimensional inspectors | |

| Real | adiscr_ |

| Real | cdiscr_ |

| Real | bdiscr_ |

| Real | ddiscr_ |

| Real | discrepancy () const |

| template<class Sequence > | |

| void | add (const Sequence &sample, Real weight=1.0) |

| template<class Iterator > | |

| void | add (Iterator begin, Iterator end, Real weight=1.0) |

| void | reset (Size dimension=0) |

Additional Inherited Members | |

| Protected Attributes inherited from GenericSequenceStatistics< StatisticsType > | |

| Size | dimension_ = 0 |

| std::vector< statistics_type > | stats_ |

| std::vector< Real > | results_ |

| Matrix | quadraticSum_ |

Detailed Description

Statistic tool for sequences with discrepancy calculation.

It inherit from SequenceStatistics<Statistics> and adds \( L^2 \) discrepancy calculation

Definition at line 35 of file discrepancystatistics.hpp.

Member Typedef Documentation

◆ value_type

Definition at line 37 of file discrepancystatistics.hpp.

Constructor & Destructor Documentation

◆ DiscrepancyStatistics()

| DiscrepancyStatistics | ( | Size | dimension | ) |

Member Function Documentation

◆ discrepancy()

| Real discrepancy | ( | ) | const |

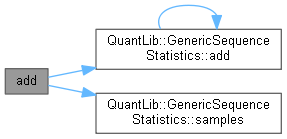

◆ add() [1/2]

| void add | ( | const Sequence & | sample, |

| Real | weight = 1.0 |

||

| ) |

Definition at line 45 of file discrepancystatistics.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ add() [2/2]

| void add | ( | Iterator | begin, |

| Iterator | end, | ||

| Real | weight = 1.0 |

||

| ) |

◆ reset()

| void reset | ( | Size | dimension = 0 | ) |

Definition at line 108 of file discrepancystatistics.hpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

Member Data Documentation

◆ adiscr_

|

mutableprivate |

Definition at line 96 of file discrepancystatistics.hpp.

◆ cdiscr_

|

private |

Definition at line 96 of file discrepancystatistics.hpp.

◆ bdiscr_

|

private |

Definition at line 97 of file discrepancystatistics.hpp.

◆ ddiscr_

|

private |

Definition at line 97 of file discrepancystatistics.hpp.