#include <exchangeratemanager.hpp>

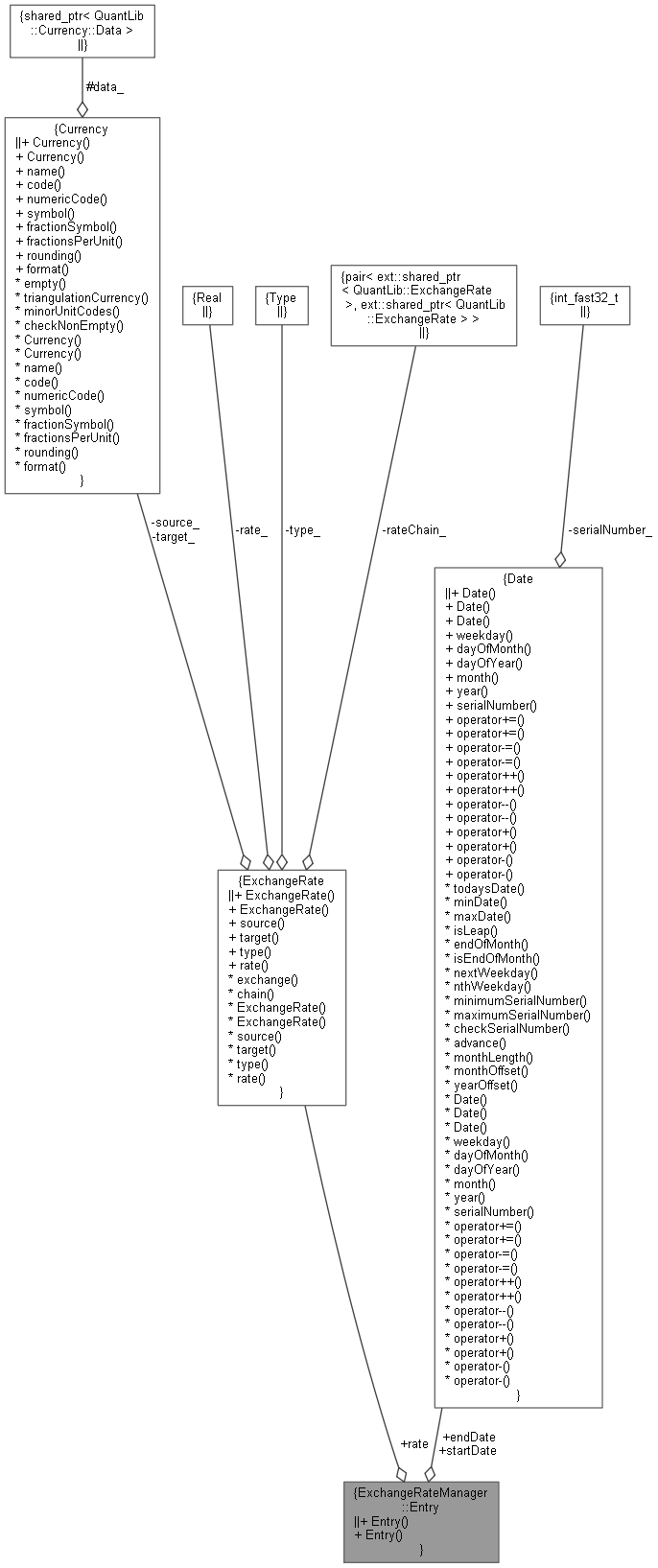

Collaboration diagram for ExchangeRateManager::Entry:

Collaboration diagram for ExchangeRateManager::Entry:

Public Member Functions | |

| Entry ()=default | |

| Entry (ExchangeRate rate, const Date &start, const Date &end) | |

Public Attributes | |

| ExchangeRate | rate |

| Date | startDate |

| Date | endDate |

Detailed Description

Definition at line 73 of file exchangeratemanager.hpp.

Constructor & Destructor Documentation

◆ Entry() [1/2]

|

default |

◆ Entry() [2/2]

| Entry | ( | ExchangeRate | rate, |

| const Date & | start, | ||

| const Date & | end | ||

| ) |

Definition at line 75 of file exchangeratemanager.hpp.

Member Data Documentation

◆ rate

| ExchangeRate rate |

Definition at line 77 of file exchangeratemanager.hpp.

◆ startDate

| Date startDate |

Definition at line 78 of file exchangeratemanager.hpp.

◆ endDate

| Date endDate |

Definition at line 78 of file exchangeratemanager.hpp.