#include <swapforwardmappings.hpp>

Collaboration diagram for SwapForwardMappings:

Collaboration diagram for SwapForwardMappings:

Static Public Member Functions | |

| static Real | annuity (const CurveState &cs, Size startIndex, Size endIndex, Size numeraireIndex) |

| compute annuity of arbitrary swap-rate More... | |

| static Real | swapDerivative (const CurveState &cs, Size startIndex, Size endIndex, Size forwardIndex) |

| compute derivative of swap-rate to underlying forward rate More... | |

| static Matrix | coterminalSwapForwardJacobian (const CurveState &cs) |

| static Matrix | coterminalSwapZedMatrix (const CurveState &cs, Spread displacement) |

| static Matrix | coinitialSwapForwardJacobian (const CurveState &cs) |

| static Matrix | coinitialSwapZedMatrix (const CurveState &cs, Spread displacement) |

| static Matrix | cmSwapForwardJacobian (const CurveState &cs, Size spanningForwards) |

| static Matrix | cmSwapZedMatrix (const CurveState &cs, Size spanningForwards, Spread displacement) |

| static Real | swaptionImpliedVolatility (const MarketModel &volStructure, Size startIndex, Size endIndex) |

Detailed Description

Definition at line 35 of file swapforwardmappings.hpp.

Member Function Documentation

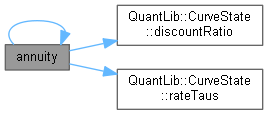

◆ annuity()

|

static |

compute annuity of arbitrary swap-rate

Definition at line 33 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

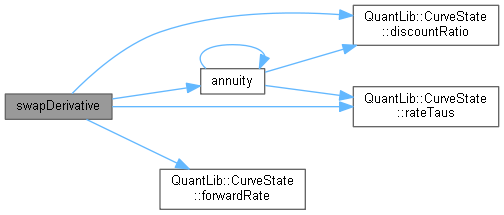

◆ swapDerivative()

|

static |

compute derivative of swap-rate to underlying forward rate

Definition at line 45 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ coterminalSwapForwardJacobian()

|

static |

Returns the dsr[i]/df[j] jacobian between coterminal swap rates and forward rates

Definition at line 72 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ coterminalSwapZedMatrix()

|

static |

Returns the Z matrix to switch base from forward to coterminal swap rates

Definition at line 102 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ coinitialSwapForwardJacobian()

|

static |

Returns the dsr[i]/df[j] jacobian between coinitial swap rates and forward rates

Definition at line 115 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ coinitialSwapZedMatrix()

|

static |

Returns the Z matrix to switch base from forward to coinitial swap rates

Definition at line 140 of file swapforwardmappings.cpp.

Here is the call graph for this function:

◆ cmSwapForwardJacobian()

|

static |

Returns the dsr[i]/df[j] jacobian between constant maturity swap rates and forward rates

Definition at line 127 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ cmSwapZedMatrix()

|

static |

Returns the Z matrix to switch base from forward to constant maturity swap rates

Definition at line 157 of file swapforwardmappings.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

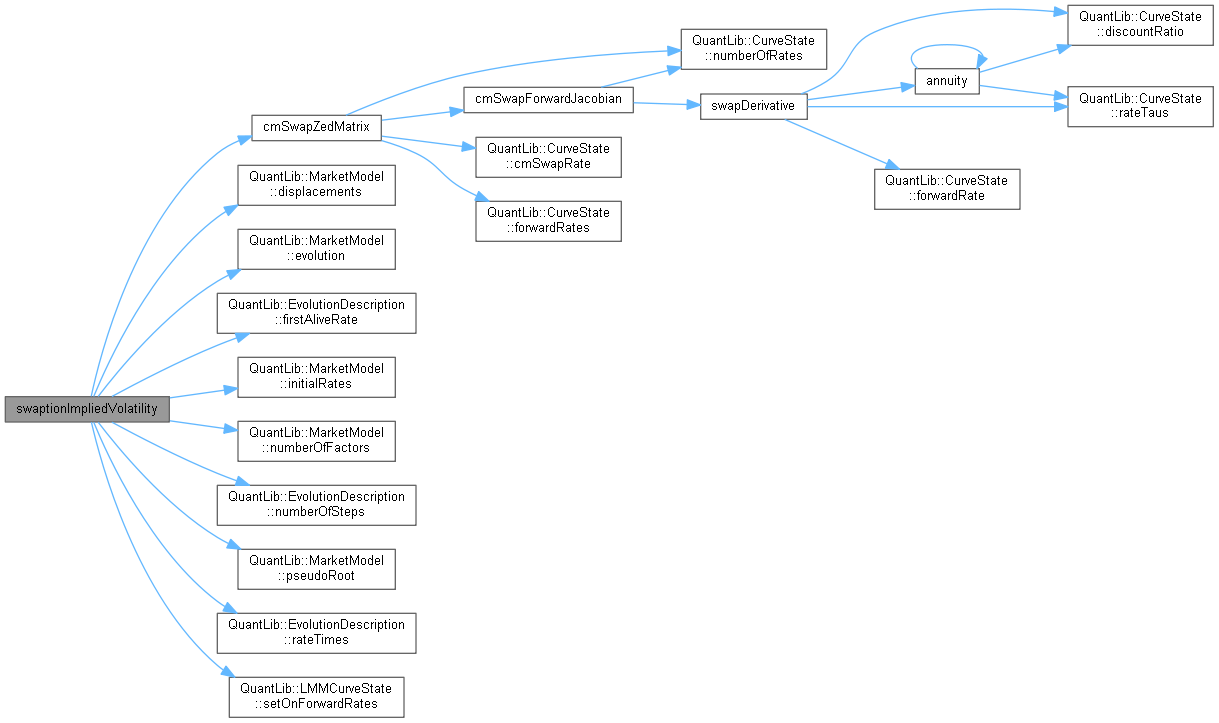

◆ swaptionImpliedVolatility()

|

static |

computes the implied vol of a swaption specified by two indices using the freezing coefficients methdodology. This routine is easy to use but not very efficient and if you want to do a lot of cases, then a different approach should be used.

Tested in SwapForwardMappingsTest::testSwaptionImpliedVolatility() in swapforwardmappings.cpp

Definition at line 175 of file swapforwardmappings.cpp.

Here is the call graph for this function: