Drift computation for log-normal Libor market models. More...

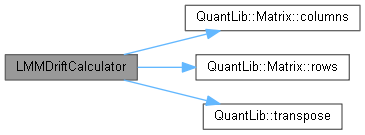

#include <lmmdriftcalculator.hpp>

Collaboration diagram for LMMDriftCalculator:

Collaboration diagram for LMMDriftCalculator:

Public Member Functions | |

| LMMDriftCalculator (const Matrix &pseudo, const std::vector< Spread > &displacements, const std::vector< Time > &taus, Size numeraire, Size alive) | |

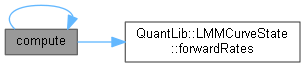

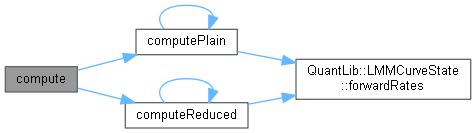

| void | compute (const LMMCurveState &cs, std::vector< Real > &drifts) const |

| Computes the drifts. More... | |

| void | compute (const std::vector< Rate > &fwds, std::vector< Real > &drifts) const |

| void | computePlain (const LMMCurveState &cs, std::vector< Real > &drifts) const |

| void | computePlain (const std::vector< Rate > &fwds, std::vector< Real > &drifts) const |

| void | computeReduced (const LMMCurveState &cs, std::vector< Real > &drifts) const |

| void | computeReduced (const std::vector< Rate > &fwds, std::vector< Real > &drifts) const |

Private Attributes | |

| Size | numberOfRates_ |

| Size | numberOfFactors_ |

| bool | isFullFactor_ |

| Size | numeraire_ |

| Size | alive_ |

| std::vector< Spread > | displacements_ |

| std::vector< Real > | oneOverTaus_ |

| Matrix | C_ |

| Matrix | pseudo_ |

| std::vector< Real > | tmp_ |

| Matrix | e_ |

| std::vector< Size > | downs_ |

| std::vector< Size > | ups_ |

Detailed Description

Drift computation for log-normal Libor market models.

Returns the drift \( \mu \Delta t \). See Mark Joshi, Rapid Computation of Drifts in a Reduced Factor Libor Market Model, Wilmott Magazine, May 2003.

Definition at line 40 of file lmmdriftcalculator.hpp.

Constructor & Destructor Documentation

◆ LMMDriftCalculator()

Member Function Documentation

◆ compute() [1/2]

| void compute | ( | const LMMCurveState & | cs, |

| std::vector< Real > & | drifts | ||

| ) | const |

Computes the drifts.

Definition at line 67 of file lmmdriftcalculator.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ compute() [2/2]

◆ computePlain() [1/2]

| void computePlain | ( | const LMMCurveState & | cs, |

| std::vector< Real > & | drifts | ||

| ) | const |

Computes the drifts without factor reduction as in eqs. 2, 4 of ref. [1] (uses the covariance matrix directly).

Definition at line 85 of file lmmdriftcalculator.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ computePlain() [2/2]

◆ computeReduced() [1/2]

| void computeReduced | ( | const LMMCurveState & | cs, |

| std::vector< Real > & | drifts | ||

| ) | const |

Computes the drifts with factor reduction as in eq. 7 of ref. [1] (uses pseudo square root of the covariance matrix).

Definition at line 112 of file lmmdriftcalculator.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ computeReduced() [2/2]

Definition at line 117 of file lmmdriftcalculator.cpp.

Member Data Documentation

◆ numberOfRates_

|

private |

Definition at line 68 of file lmmdriftcalculator.hpp.

◆ numberOfFactors_

|

private |

Definition at line 68 of file lmmdriftcalculator.hpp.

◆ isFullFactor_

|

private |

Definition at line 69 of file lmmdriftcalculator.hpp.

◆ numeraire_

|

private |

Definition at line 70 of file lmmdriftcalculator.hpp.

◆ alive_

|

private |

Definition at line 70 of file lmmdriftcalculator.hpp.

◆ displacements_

|

private |

Definition at line 71 of file lmmdriftcalculator.hpp.

◆ oneOverTaus_

|

private |

Definition at line 72 of file lmmdriftcalculator.hpp.

◆ C_

|

private |

Definition at line 73 of file lmmdriftcalculator.hpp.

◆ pseudo_

|

private |

Definition at line 73 of file lmmdriftcalculator.hpp.

◆ tmp_

|

mutableprivate |

Definition at line 75 of file lmmdriftcalculator.hpp.

◆ e_

|

mutableprivate |

Definition at line 76 of file lmmdriftcalculator.hpp.

◆ downs_

|

private |

Definition at line 77 of file lmmdriftcalculator.hpp.

◆ ups_

|

private |

Definition at line 77 of file lmmdriftcalculator.hpp.