#include <overnightindexedcouponpricer.hpp>

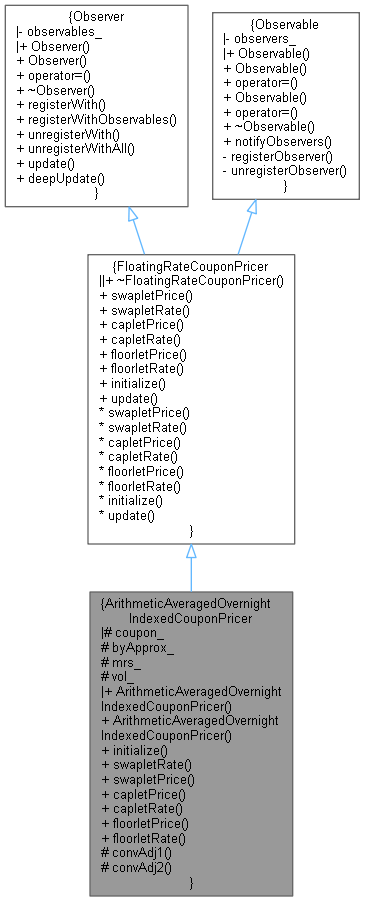

Inheritance diagram for ArithmeticAveragedOvernightIndexedCouponPricer:

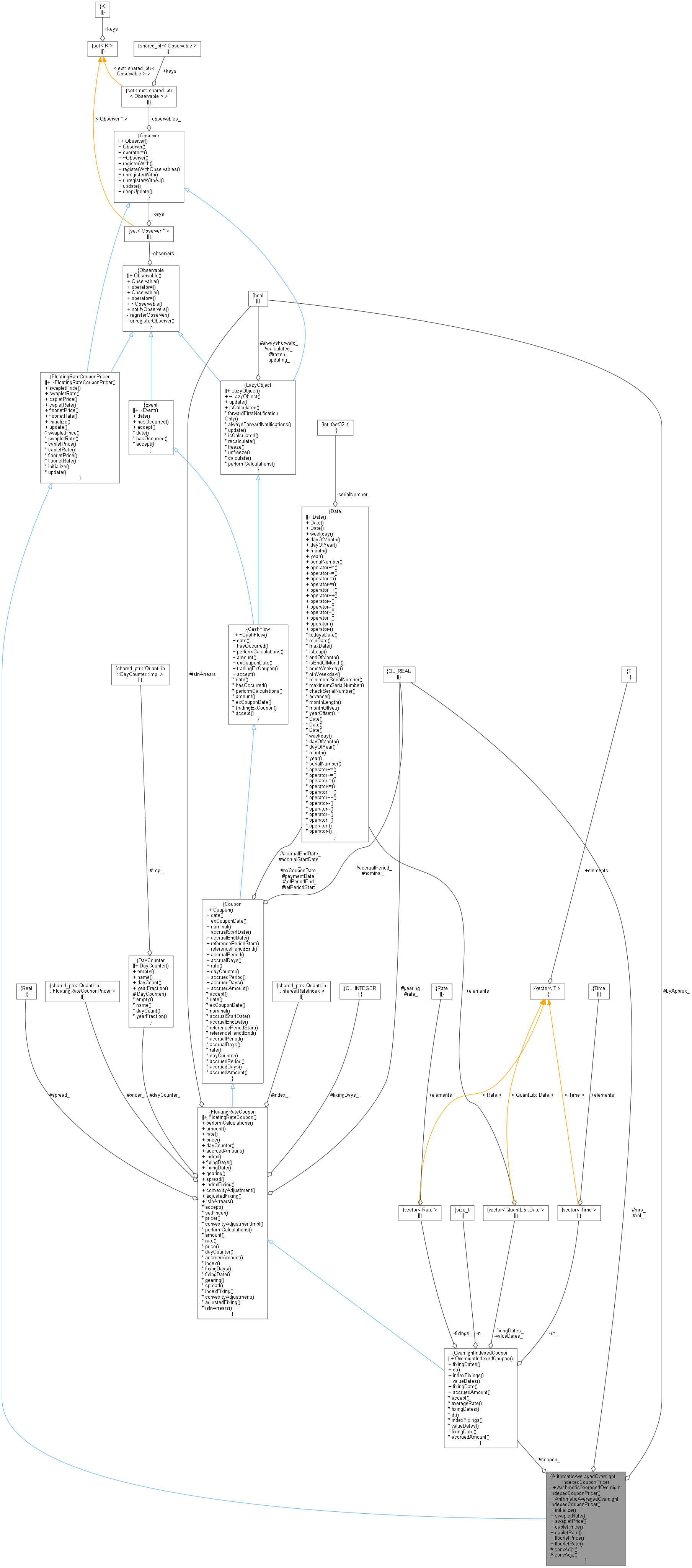

Inheritance diagram for ArithmeticAveragedOvernightIndexedCouponPricer: Collaboration diagram for ArithmeticAveragedOvernightIndexedCouponPricer:

Collaboration diagram for ArithmeticAveragedOvernightIndexedCouponPricer:

Public Member Functions | |

| ArithmeticAveragedOvernightIndexedCouponPricer (Real meanReversion=0.03, Real volatility=0.00, bool byApprox=false) | |

| ArithmeticAveragedOvernightIndexedCouponPricer (bool byApprox) | |

| void | initialize (const FloatingRateCoupon &coupon) override |

| Rate | swapletRate () const override |

| Real | swapletPrice () const override |

| Real | capletPrice (Rate) const override |

| Rate | capletRate (Rate) const override |

| Real | floorletPrice (Rate) const override |

| Rate | floorletRate (Rate) const override |

| Public Member Functions inherited from FloatingRateCouponPricer | |

| ~FloatingRateCouponPricer () override=default | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Protected Member Functions | |

| Real | convAdj1 (Time ts, Time te) const |

| Real | convAdj2 (Time ts, Time te) const |

Protected Attributes | |

| const OvernightIndexedCoupon * | coupon_ |

| bool | byApprox_ |

| Real | mrs_ |

| Real | vol_ |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

Detailed Description

pricer for arithmetically averaged overnight indexed coupons Reference: Katsumi Takada 2011, Valuation of Arithmetically Average of Fed Funds Rates and Construction of the US Dollar Swap Yield Curve

Definition at line 61 of file overnightindexedcouponpricer.hpp.

Constructor & Destructor Documentation

◆ ArithmeticAveragedOvernightIndexedCouponPricer() [1/2]

|

explicit |

Definition at line 63 of file overnightindexedcouponpricer.hpp.

◆ ArithmeticAveragedOvernightIndexedCouponPricer() [2/2]

|

explicit |

Definition at line 69 of file overnightindexedcouponpricer.hpp.

Member Function Documentation

◆ initialize()

|

overridevirtual |

Implements FloatingRateCouponPricer.

Definition at line 180 of file overnightindexedcouponpricer.cpp.

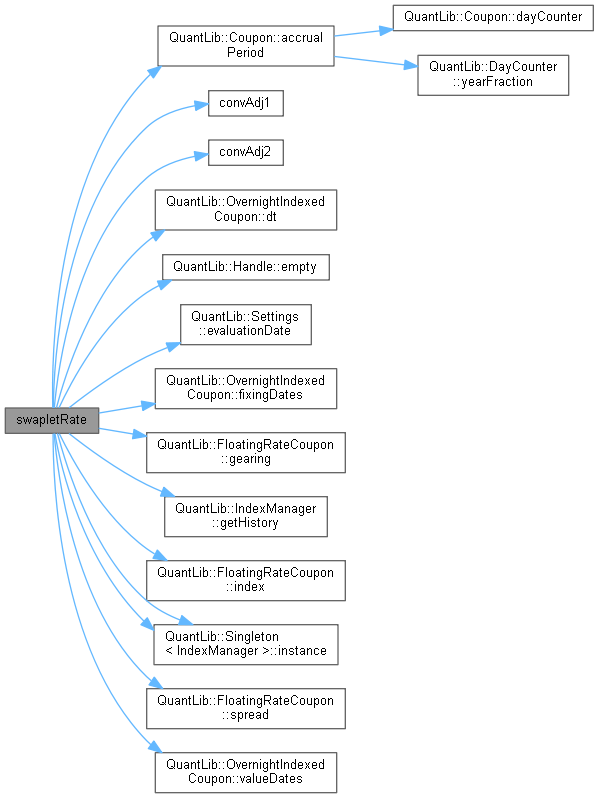

◆ swapletRate()

|

overridevirtual |

Implements FloatingRateCouponPricer.

Definition at line 185 of file overnightindexedcouponpricer.cpp.

Here is the call graph for this function:

◆ swapletPrice()

|

overridevirtual |

Implements FloatingRateCouponPricer.

Definition at line 75 of file overnightindexedcouponpricer.hpp.

◆ capletPrice()

Implements FloatingRateCouponPricer.

Definition at line 76 of file overnightindexedcouponpricer.hpp.

◆ capletRate()

Implements FloatingRateCouponPricer.

Definition at line 77 of file overnightindexedcouponpricer.hpp.

◆ floorletPrice()

Implements FloatingRateCouponPricer.

Definition at line 78 of file overnightindexedcouponpricer.hpp.

◆ floorletRate()

Implements FloatingRateCouponPricer.

Definition at line 79 of file overnightindexedcouponpricer.hpp.

◆ convAdj1()

Definition at line 270 of file overnightindexedcouponpricer.cpp.

Here is the caller graph for this function:

◆ convAdj2()

Definition at line 275 of file overnightindexedcouponpricer.cpp.

Here is the caller graph for this function:

Member Data Documentation

◆ coupon_

|

protected |

Definition at line 84 of file overnightindexedcouponpricer.hpp.

◆ byApprox_

|

protected |

Definition at line 85 of file overnightindexedcouponpricer.hpp.

◆ mrs_

|

protected |

Definition at line 86 of file overnightindexedcouponpricer.hpp.

◆ vol_

|

protected |

Definition at line 87 of file overnightindexedcouponpricer.hpp.