Main cycle of the Australian Securities Exchange (a.k.a. ASX) months. More...

#include <asx.hpp>

Collaboration diagram for ASX:

Collaboration diagram for ASX:

Public Types | |

| enum | Month { F = 1 , G = 2 , H = 3 , J = 4 , K = 5 , M = 6 , N = 7 , Q = 8 , U = 9 , V = 10 , X = 11 , Z = 12 } |

Static Public Member Functions | |

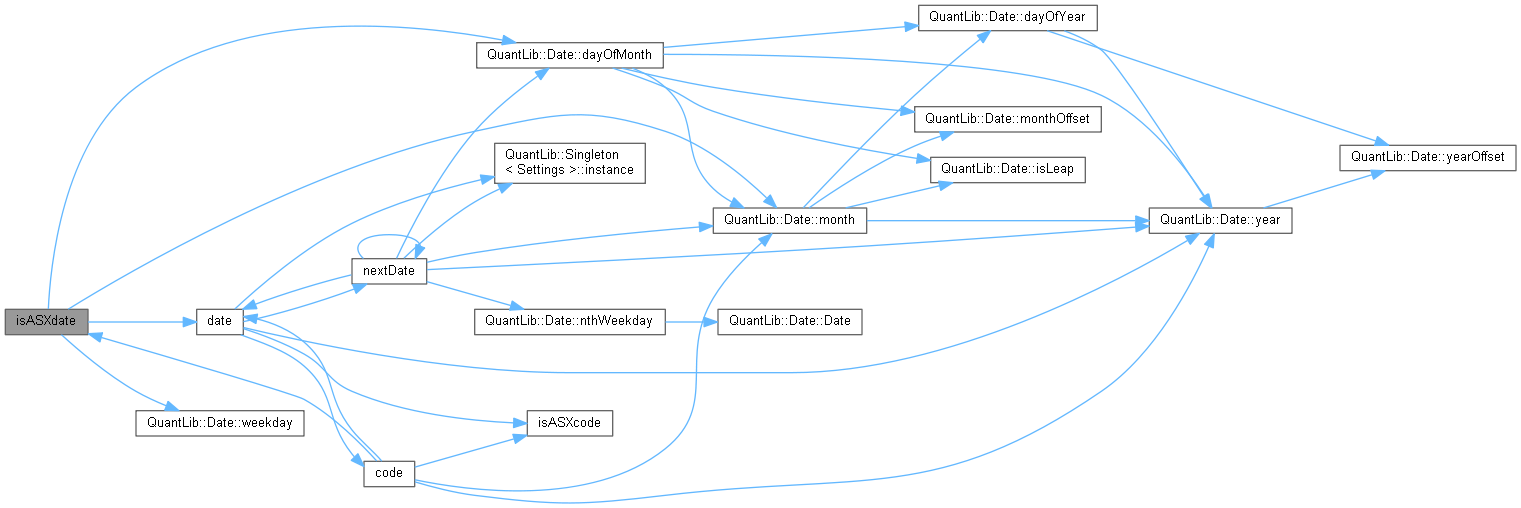

| static bool | isASXdate (const Date &d, bool mainCycle=true) |

| returns whether or not the given date is an ASX date More... | |

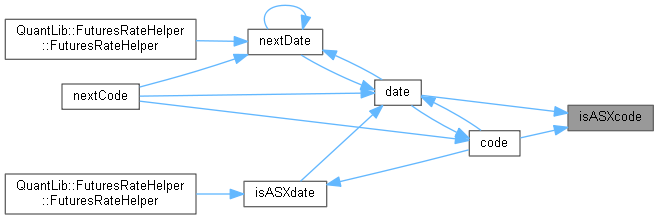

| static bool | isASXcode (const std::string &in, bool mainCycle=true) |

| returns whether or not the given string is an ASX code More... | |

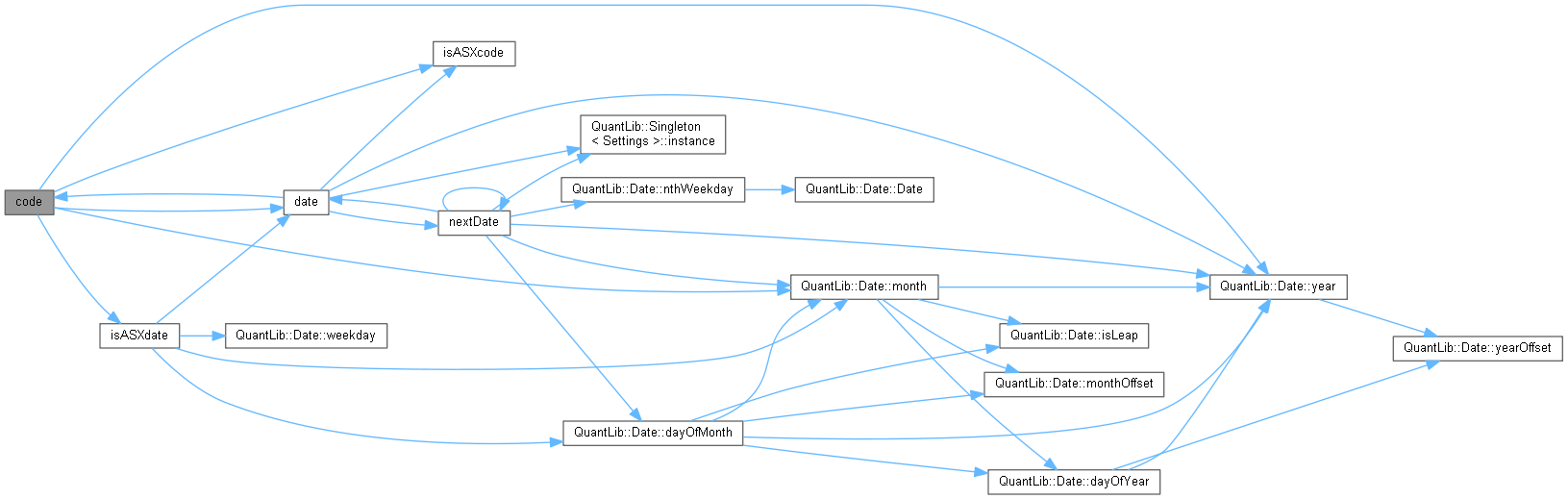

| static std::string | code (const Date &asxDate) |

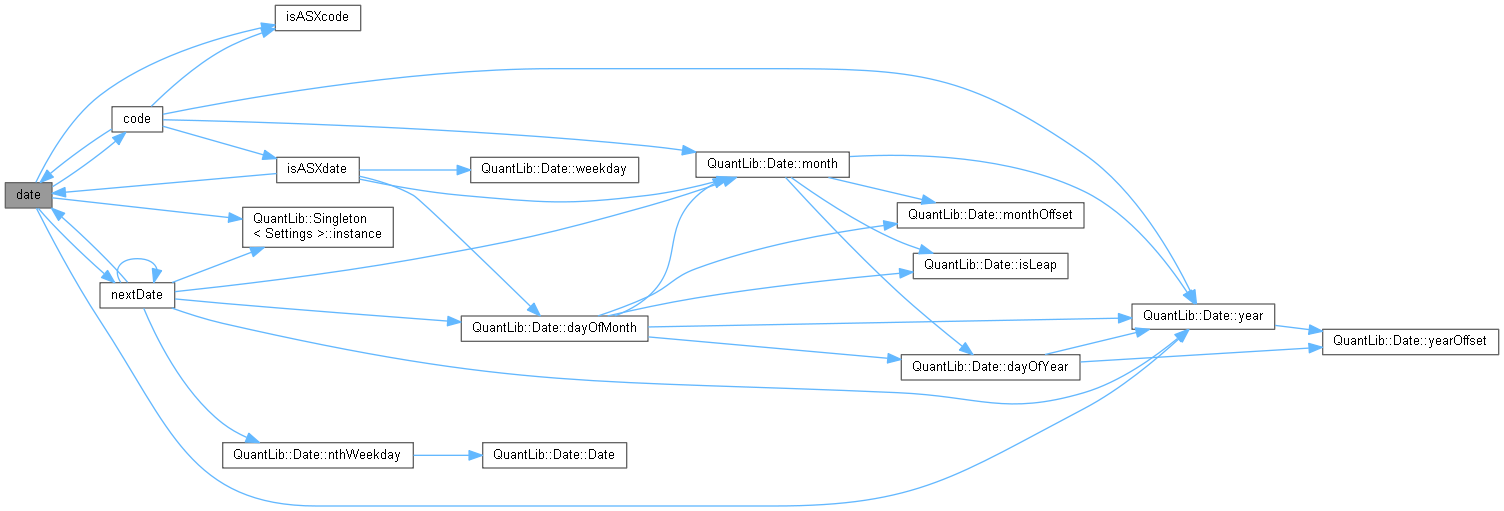

| static Date | date (const std::string &asxCode, const Date &referenceDate=Date()) |

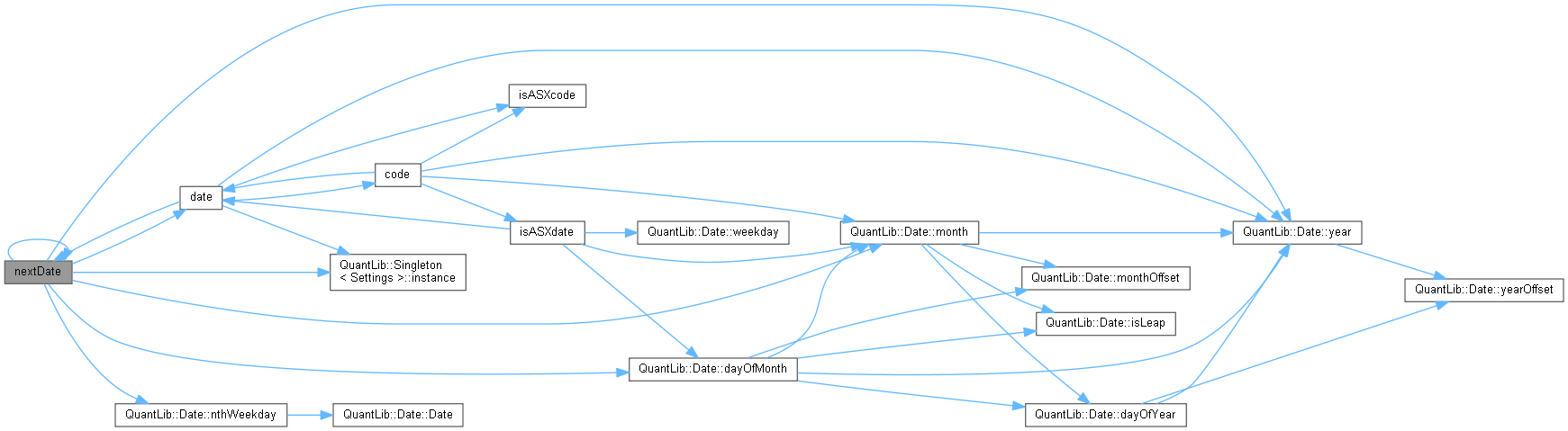

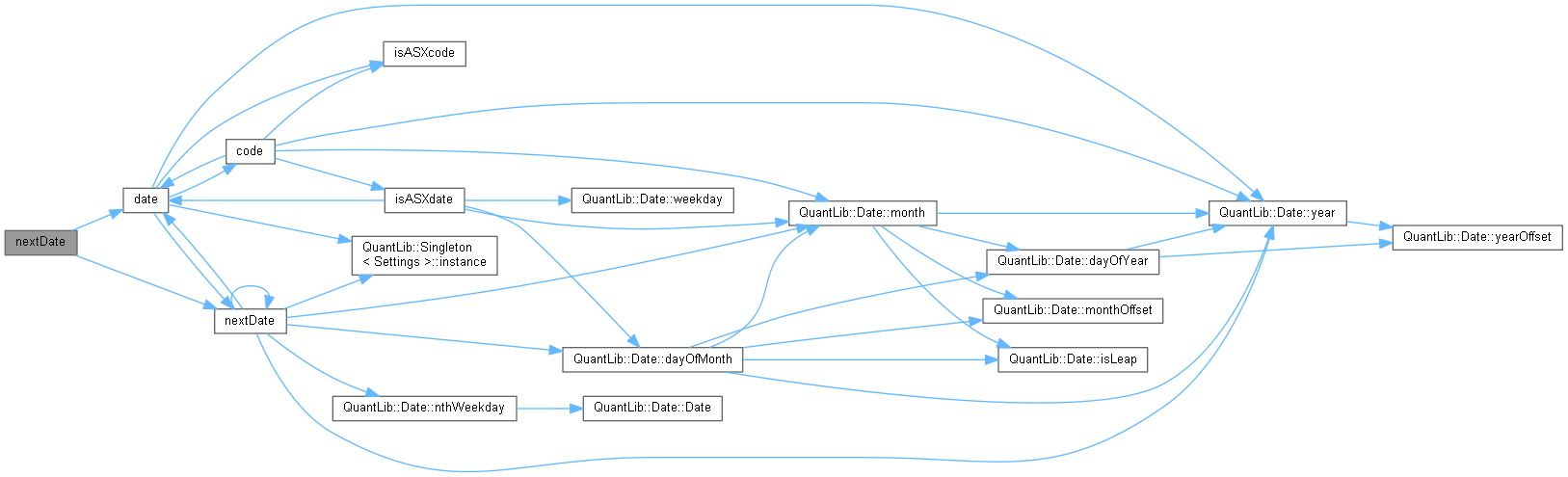

| static Date | nextDate (const Date &d=Date(), bool mainCycle=true) |

| next ASX date following the given date More... | |

| static Date | nextDate (const std::string &asxCode, bool mainCycle=true, const Date &referenceDate=Date()) |

| next ASX date following the given ASX code More... | |

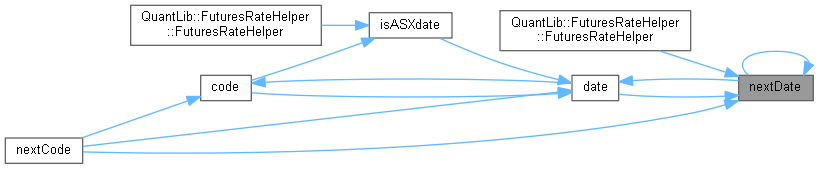

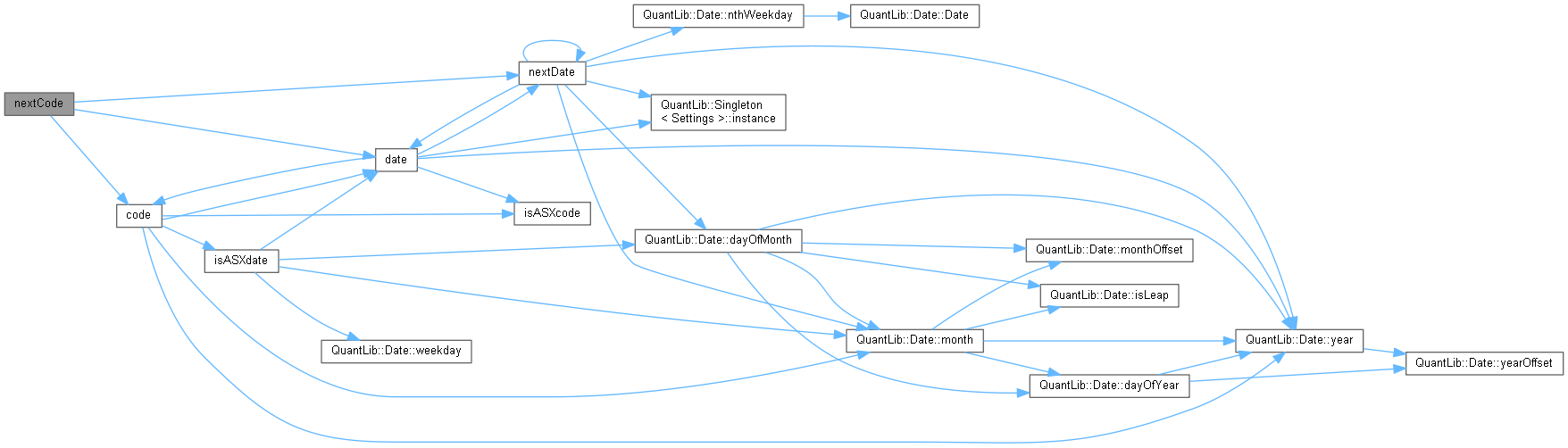

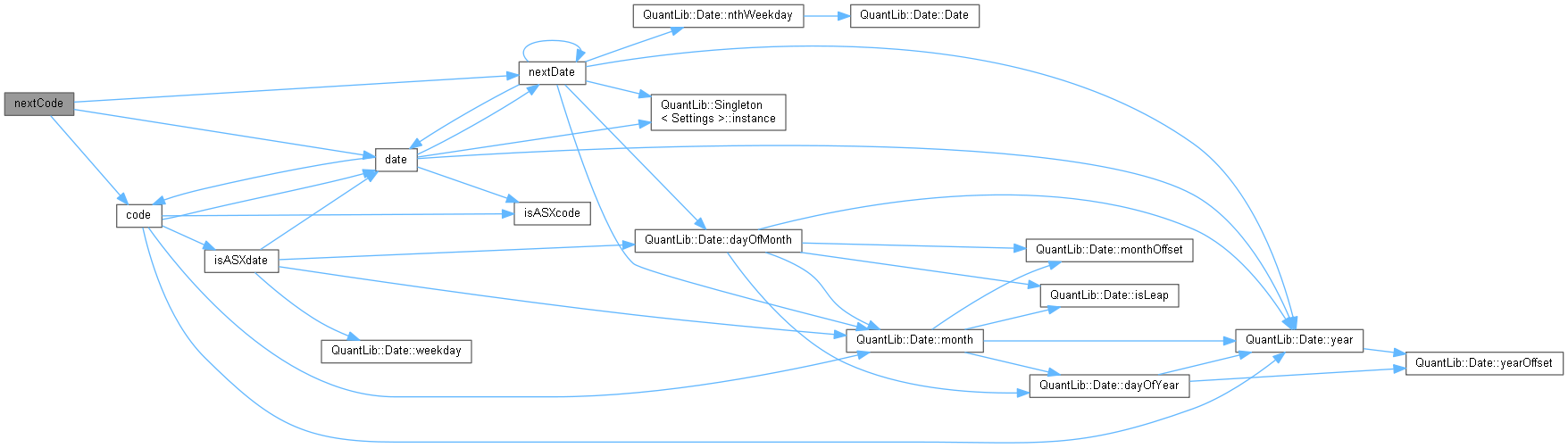

| static std::string | nextCode (const Date &d=Date(), bool mainCycle=true) |

| next ASX code following the given date More... | |

| static std::string | nextCode (const std::string &asxCode, bool mainCycle=true, const Date &referenceDate=Date()) |

| next ASX code following the given code More... | |

Detailed Description

Main cycle of the Australian Securities Exchange (a.k.a. ASX) months.

Member Enumeration Documentation

◆ Month

Member Function Documentation

◆ isASXdate()

◆ isASXcode()

◆ code()

|

static |