#include <inflationindex.hpp>

Collaboration diagram for CPI:

Collaboration diagram for CPI:

Public Types | |

| enum | InterpolationType { AsIndex , Flat , Linear } |

| when you observe an index, how do you interpolate between fixings? More... | |

Static Public Member Functions | |

| static Real | laggedFixing (const ext::shared_ptr< ZeroInflationIndex > &index, const Date &date, const Period &observationLag, InterpolationType interpolationType) |

| interpolated inflation fixing More... | |

| static Real | laggedYoYRate (const ext::shared_ptr< YoYInflationIndex > &index, const Date &date, const Period &observationLag, InterpolationType interpolationType) |

| interpolated year-on-year inflation rate More... | |

Detailed Description

Definition at line 39 of file inflationindex.hpp.

Member Enumeration Documentation

◆ InterpolationType

| enum InterpolationType |

when you observe an index, how do you interpolate between fixings?

| Enumerator | |

|---|---|

| AsIndex | same interpolation as index |

| Flat | flat from previous fixing |

| Linear | linearly between bracketing fixings |

Definition at line 42 of file inflationindex.hpp.

Member Function Documentation

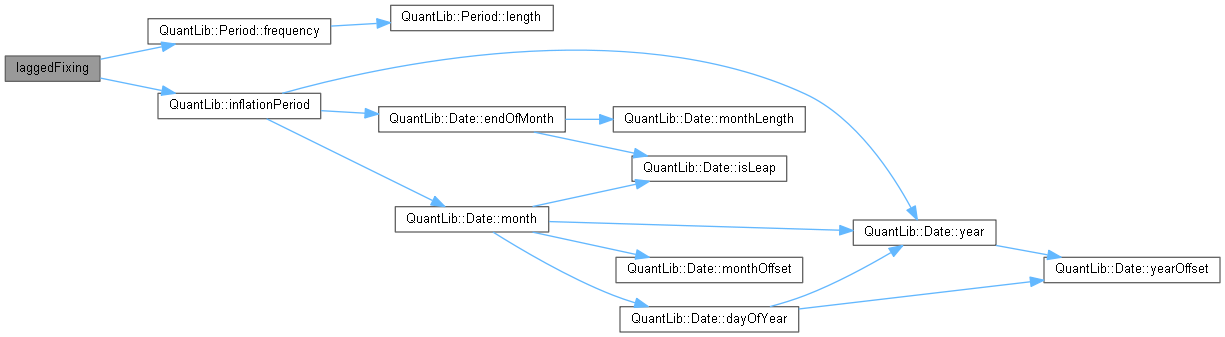

◆ laggedFixing()

|

static |

interpolated inflation fixing

- Parameters

-

index The index whose fixing should be retrieved date The date without lag; usually, the payment date for some inflation-based coupon. observationLag The observation lag to be subtracted from the passed date; for instance, if the passed date is in May and the lag is three months, the inflation fixing from February (and March, in case of interpolation) will be observed. interpolationType The interpolation type (flat or linear)

Definition at line 28 of file inflationindex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

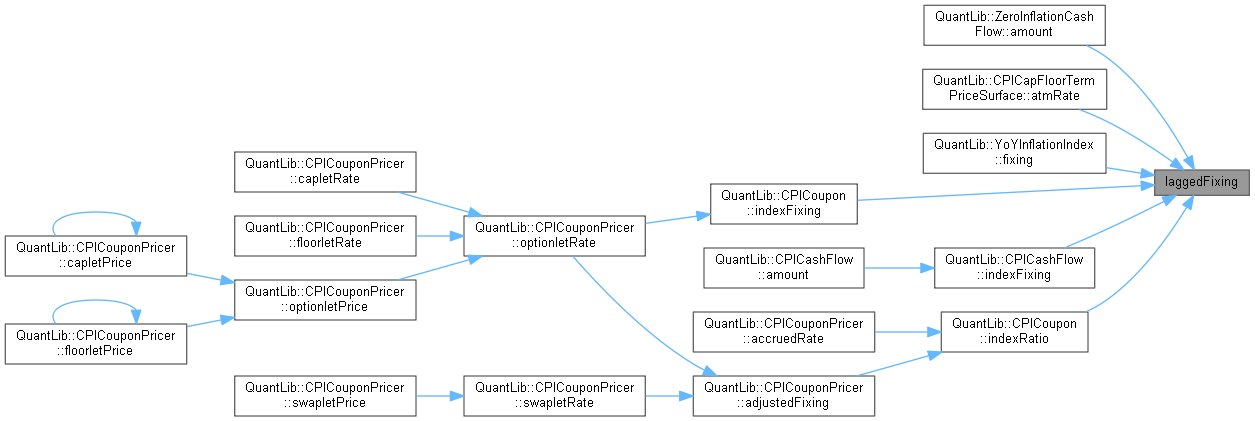

◆ laggedYoYRate()

|

static |

interpolated year-on-year inflation rate

- Parameters

-

index The index whose fixing should be retrieved date The date without lag; usually, the payment date for some inflation-based coupon. observationLag The observation lag to be subtracted from the passed date; for instance, if the passed date is in May and the lag is three months, the year-on-year rate from February (and March, in case of interpolation) will be observed. interpolationType The interpolation type (flat or linear)

Definition at line 65 of file inflationindex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function: