Gamma function class. More...

#include <gammadistribution.hpp>

Collaboration diagram for GammaFunction:

Collaboration diagram for GammaFunction:

Public Member Functions | |

| Real | value (Real x) const |

| Real | logValue (Real x) const |

Static Private Attributes | |

| static const Real | c1_ = 76.18009172947146 |

| static const Real | c2_ = -86.50532032941677 |

| static const Real | c3_ = 24.01409824083091 |

| static const Real | c4_ = -1.231739572450155 |

| static const Real | c5_ = 0.1208650973866179e-2 |

| static const Real | c6_ = -0.5395239384953e-5 |

Detailed Description

Gamma function class.

This is a function defined by

\[ \Gamma(z) = \int_0^{\infty}t^{z-1}e^{-t}dt \]

The implementation of the algorithm was inspired by "Numerical Recipes in C", 2nd edition, Press, Teukolsky, Vetterling, Flannery, chapter 6

- Tests:

- the correctness of the returned value is tested by checking it against known good results.

Definition at line 56 of file gammadistribution.hpp.

Member Function Documentation

◆ value()

Definition at line 84 of file gammadistribution.cpp.

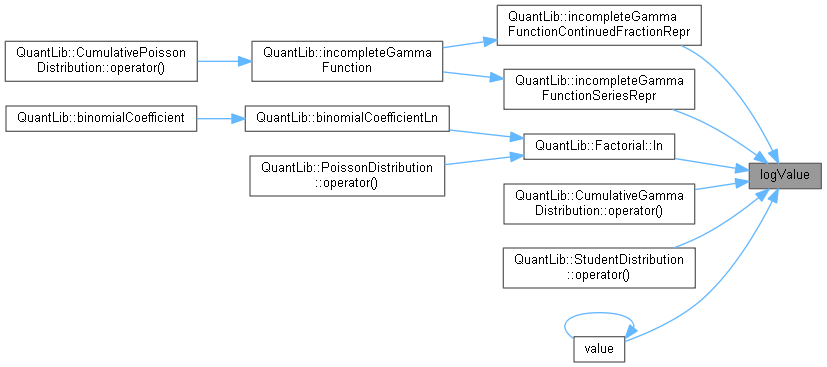

Here is the call graph for this function: Here is the caller graph for this function:

Here is the caller graph for this function:

◆ logValue()

Member Data Documentation

◆ c1_

|

staticprivate |

Definition at line 61 of file gammadistribution.hpp.

◆ c2_

|

staticprivate |

Definition at line 61 of file gammadistribution.hpp.

◆ c3_

|

staticprivate |

Definition at line 61 of file gammadistribution.hpp.

◆ c4_

|

staticprivate |

Definition at line 61 of file gammadistribution.hpp.

◆ c5_

|

staticprivate |

Definition at line 61 of file gammadistribution.hpp.

◆ c6_

|

staticprivate |

Definition at line 61 of file gammadistribution.hpp.