Tree approximating a single-factor diffusion More...

#include <tree.hpp>

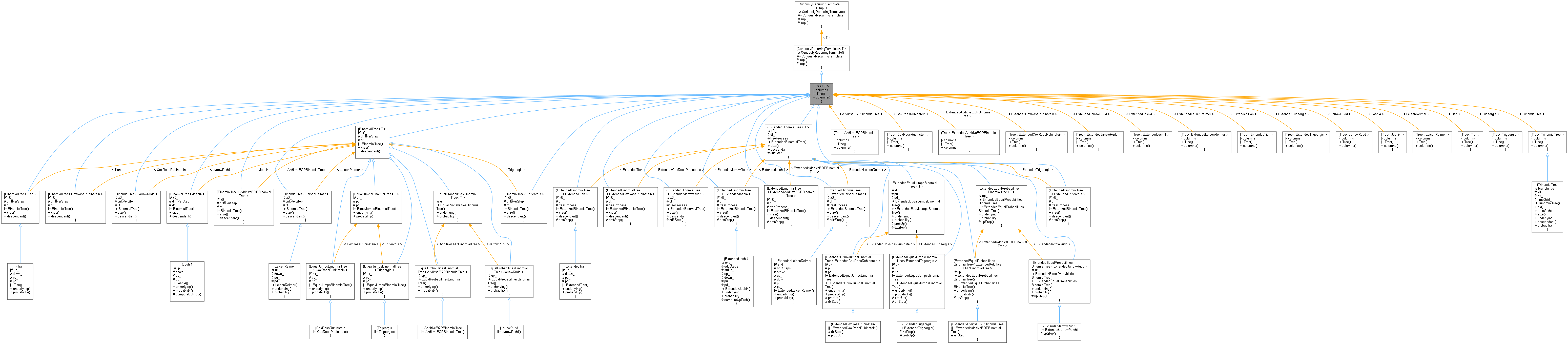

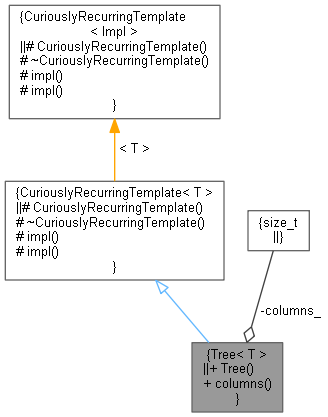

Inheritance diagram for Tree< T >:

Inheritance diagram for Tree< T >: Collaboration diagram for Tree< T >:

Collaboration diagram for Tree< T >:

Public Member Functions | |

| Tree (Size columns) | |

| Size | columns () const |

Private Attributes | |

| Size | columns_ |

Additional Inherited Members | |

| Protected Member Functions inherited from CuriouslyRecurringTemplate< T > | |

| CuriouslyRecurringTemplate ()=default | |

| ~CuriouslyRecurringTemplate ()=default | |

| T & | impl () |

| const T & | impl () const |

Detailed Description

template<class T>

class QuantLib::Tree< T >

class QuantLib::Tree< T >

Tree approximating a single-factor diffusion

Derived classes must implement the following interface:

public:

and provide a public enumeration

enum { branches = N };

where N is a suitable constant (2 for binomial, 3 for trinomial...)