helper class building a sequence of overnight coupons More...

#include <overnightindexedcoupon.hpp>

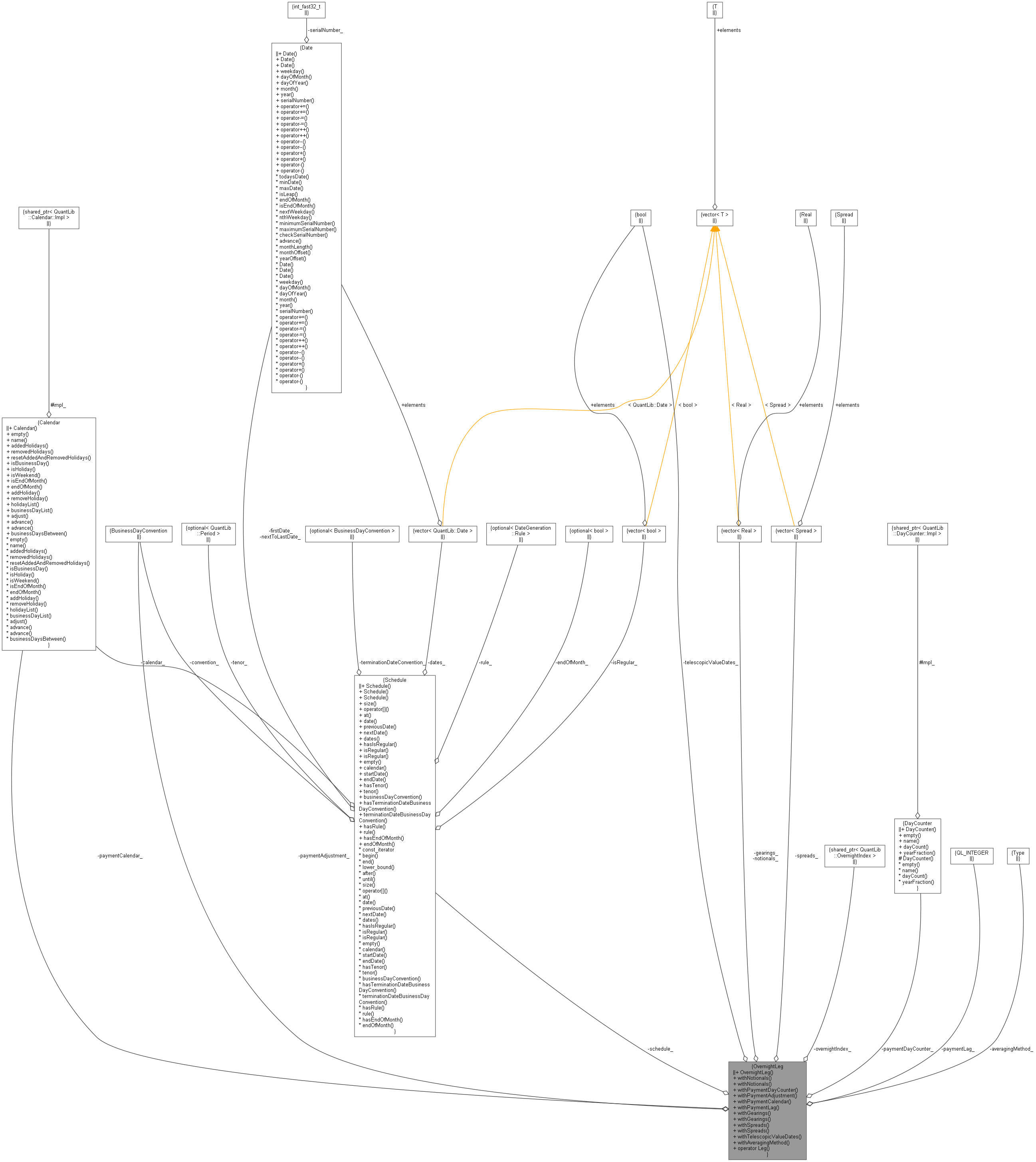

Collaboration diagram for OvernightLeg:

Collaboration diagram for OvernightLeg:

Public Member Functions | |

| OvernightLeg (Schedule schedule, ext::shared_ptr< OvernightIndex > overnightIndex) | |

| OvernightLeg & | withNotionals (Real notional) |

| OvernightLeg & | withNotionals (const std::vector< Real > ¬ionals) |

| OvernightLeg & | withPaymentDayCounter (const DayCounter &) |

| OvernightLeg & | withPaymentAdjustment (BusinessDayConvention) |

| OvernightLeg & | withPaymentCalendar (const Calendar &) |

| OvernightLeg & | withPaymentLag (Integer lag) |

| OvernightLeg & | withGearings (Real gearing) |

| OvernightLeg & | withGearings (const std::vector< Real > &gearings) |

| OvernightLeg & | withSpreads (Spread spread) |

| OvernightLeg & | withSpreads (const std::vector< Spread > &spreads) |

| OvernightLeg & | withTelescopicValueDates (bool telescopicValueDates) |

| OvernightLeg & | withAveragingMethod (RateAveraging::Type averagingMethod) |

| OvernightLeg & | withLookbackDays (Natural lookbackDays) |

| OvernightLeg & | withLockoutDays (Natural lockoutDays) |

| OvernightLeg & | withObservationShift (bool applyObservationShift=true) |

| operator Leg () const | |

Private Attributes | |

| Schedule | schedule_ |

| ext::shared_ptr< OvernightIndex > | overnightIndex_ |

| std::vector< Real > | notionals_ |

| DayCounter | paymentDayCounter_ |

| Calendar | paymentCalendar_ |

| BusinessDayConvention | paymentAdjustment_ = Following |

| Integer | paymentLag_ = 0 |

| std::vector< Real > | gearings_ |

| std::vector< Spread > | spreads_ |

| bool | telescopicValueDates_ = false |

| RateAveraging::Type | averagingMethod_ = RateAveraging::Compound |

| Natural | lookbackDays_ = Null<Natural>() |

| Natural | lockoutDays_ = 0 |

| bool | applyObservationShift_ = false |

Detailed Description

helper class building a sequence of overnight coupons

Definition at line 121 of file overnightindexedcoupon.hpp.

Constructor & Destructor Documentation

◆ OvernightLeg()

| OvernightLeg | ( | Schedule | schedule, |

| ext::shared_ptr< OvernightIndex > | overnightIndex | ||

| ) |

Definition at line 225 of file overnightindexedcoupon.cpp.

Member Function Documentation

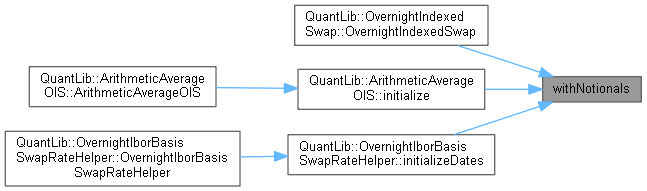

◆ withNotionals() [1/2]

| OvernightLeg & withNotionals | ( | Real | notional | ) |

Definition at line 230 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withNotionals() [2/2]

| OvernightLeg & withNotionals | ( | const std::vector< Real > & | notionals | ) |

Definition at line 235 of file overnightindexedcoupon.cpp.

◆ withPaymentDayCounter()

| OvernightLeg & withPaymentDayCounter | ( | const DayCounter & | dc | ) |

Definition at line 240 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withPaymentAdjustment()

| OvernightLeg & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

Definition at line 246 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withPaymentCalendar()

| OvernightLeg & withPaymentCalendar | ( | const Calendar & | cal | ) |

Definition at line 251 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withPaymentLag()

| OvernightLeg & withPaymentLag | ( | Integer | lag | ) |

Definition at line 256 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withGearings() [1/2]

| OvernightLeg & withGearings | ( | Real | gearing | ) |

Definition at line 261 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withGearings() [2/2]

| OvernightLeg & withGearings | ( | const std::vector< Real > & | gearings | ) |

Definition at line 266 of file overnightindexedcoupon.cpp.

◆ withSpreads() [1/2]

| OvernightLeg & withSpreads | ( | Spread | spread | ) |

Definition at line 271 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withSpreads() [2/2]

| OvernightLeg & withSpreads | ( | const std::vector< Spread > & | spreads | ) |

Definition at line 276 of file overnightindexedcoupon.cpp.

◆ withTelescopicValueDates()

| OvernightLeg & withTelescopicValueDates | ( | bool | telescopicValueDates | ) |

Definition at line 281 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withAveragingMethod()

| OvernightLeg & withAveragingMethod | ( | RateAveraging::Type | averagingMethod | ) |

Definition at line 286 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withLookbackDays()

| OvernightLeg & withLookbackDays | ( | Natural | lookbackDays | ) |

Definition at line 291 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withLockoutDays()

| OvernightLeg & withLockoutDays | ( | Natural | lockoutDays | ) |

Definition at line 295 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

◆ withObservationShift()

| OvernightLeg & withObservationShift | ( | bool | applyObservationShift = true | ) |

Definition at line 299 of file overnightindexedcoupon.cpp.

Here is the caller graph for this function:

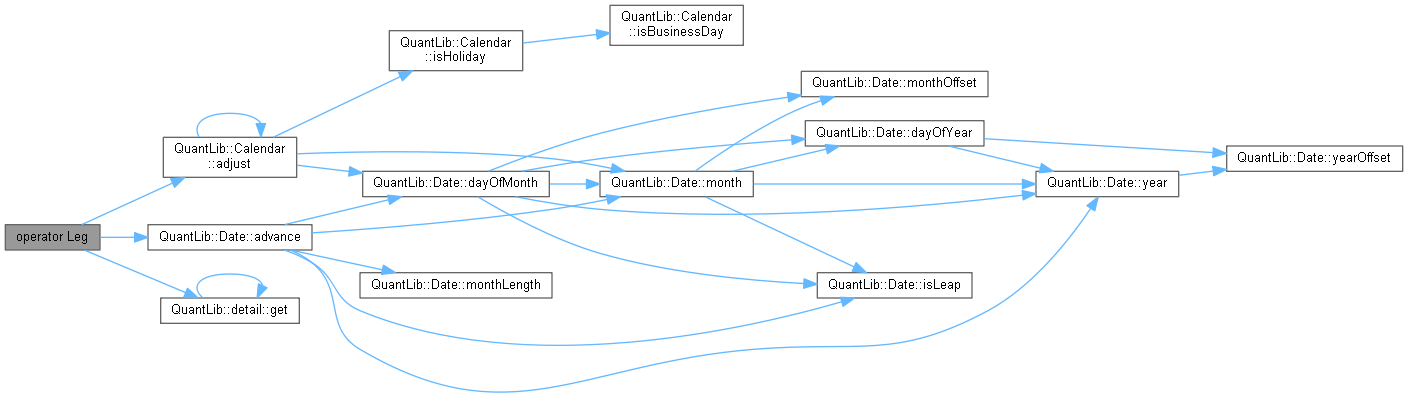

◆ operator Leg()

| operator Leg | ( | ) | const |

Definition at line 304 of file overnightindexedcoupon.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ schedule_

|

private |

Definition at line 141 of file overnightindexedcoupon.hpp.

◆ overnightIndex_

|

private |

Definition at line 142 of file overnightindexedcoupon.hpp.

◆ notionals_

|

private |

Definition at line 143 of file overnightindexedcoupon.hpp.

◆ paymentDayCounter_

|

private |

Definition at line 144 of file overnightindexedcoupon.hpp.

◆ paymentCalendar_

|

private |

Definition at line 145 of file overnightindexedcoupon.hpp.

◆ paymentAdjustment_

|

private |

Definition at line 146 of file overnightindexedcoupon.hpp.

◆ paymentLag_

|

private |

Definition at line 147 of file overnightindexedcoupon.hpp.

◆ gearings_

|

private |

Definition at line 148 of file overnightindexedcoupon.hpp.

◆ spreads_

|

private |

Definition at line 149 of file overnightindexedcoupon.hpp.

◆ telescopicValueDates_

|

private |

Definition at line 150 of file overnightindexedcoupon.hpp.

◆ averagingMethod_

|

private |

Definition at line 151 of file overnightindexedcoupon.hpp.

◆ lookbackDays_

Definition at line 152 of file overnightindexedcoupon.hpp.

◆ lockoutDays_

|

private |

Definition at line 153 of file overnightindexedcoupon.hpp.

◆ applyObservationShift_

|

private |

Definition at line 154 of file overnightindexedcoupon.hpp.