base class for early exercise path pricers More...

#include <earlyexercisepathpricer.hpp>

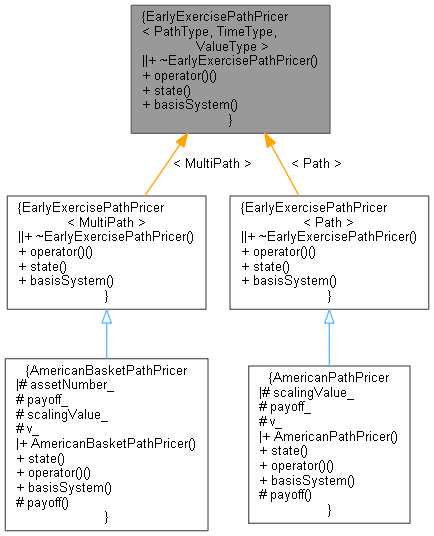

Inheritance diagram for EarlyExercisePathPricer< PathType, TimeType, ValueType >:

Inheritance diagram for EarlyExercisePathPricer< PathType, TimeType, ValueType >: Collaboration diagram for EarlyExercisePathPricer< PathType, TimeType, ValueType >:

Collaboration diagram for EarlyExercisePathPricer< PathType, TimeType, ValueType >:

Public Types | |

| typedef EarlyExerciseTraits< PathType >::StateType | StateType |

Public Member Functions | |

| virtual | ~EarlyExercisePathPricer ()=default |

| virtual ValueType | operator() (const PathType &path, TimeType t) const =0 |

| virtual StateType | state (const PathType &path, TimeType t) const =0 |

| virtual std::vector< std::function< ValueType(StateType)> > | basisSystem () const =0 |

Detailed Description

template<class PathType, class TimeType = Size, class ValueType = Real>

class QuantLib::EarlyExercisePathPricer< PathType, TimeType, ValueType >

class QuantLib::EarlyExercisePathPricer< PathType, TimeType, ValueType >

base class for early exercise path pricers

Returns the value of an option on a given path and given time.

Definition at line 64 of file earlyexercisepathpricer.hpp.

Member Typedef Documentation

◆ StateType

| typedef EarlyExerciseTraits<PathType>::StateType StateType |

Definition at line 66 of file earlyexercisepathpricer.hpp.

Constructor & Destructor Documentation

◆ ~EarlyExercisePathPricer()

|

virtualdefault |

Member Function Documentation

◆ operator()()

|

pure virtual |

Implemented in AmericanBasketPathPricer, and AmericanPathPricer.

◆ state()

|

pure virtual |

Implemented in AmericanBasketPathPricer, and AmericanPathPricer.

◆ basisSystem()

|

pure virtual |

Implemented in AmericanBasketPathPricer, and AmericanPathPricer.