helper class building a sequence of average BMA coupons More...

#include <averagebmacoupon.hpp>

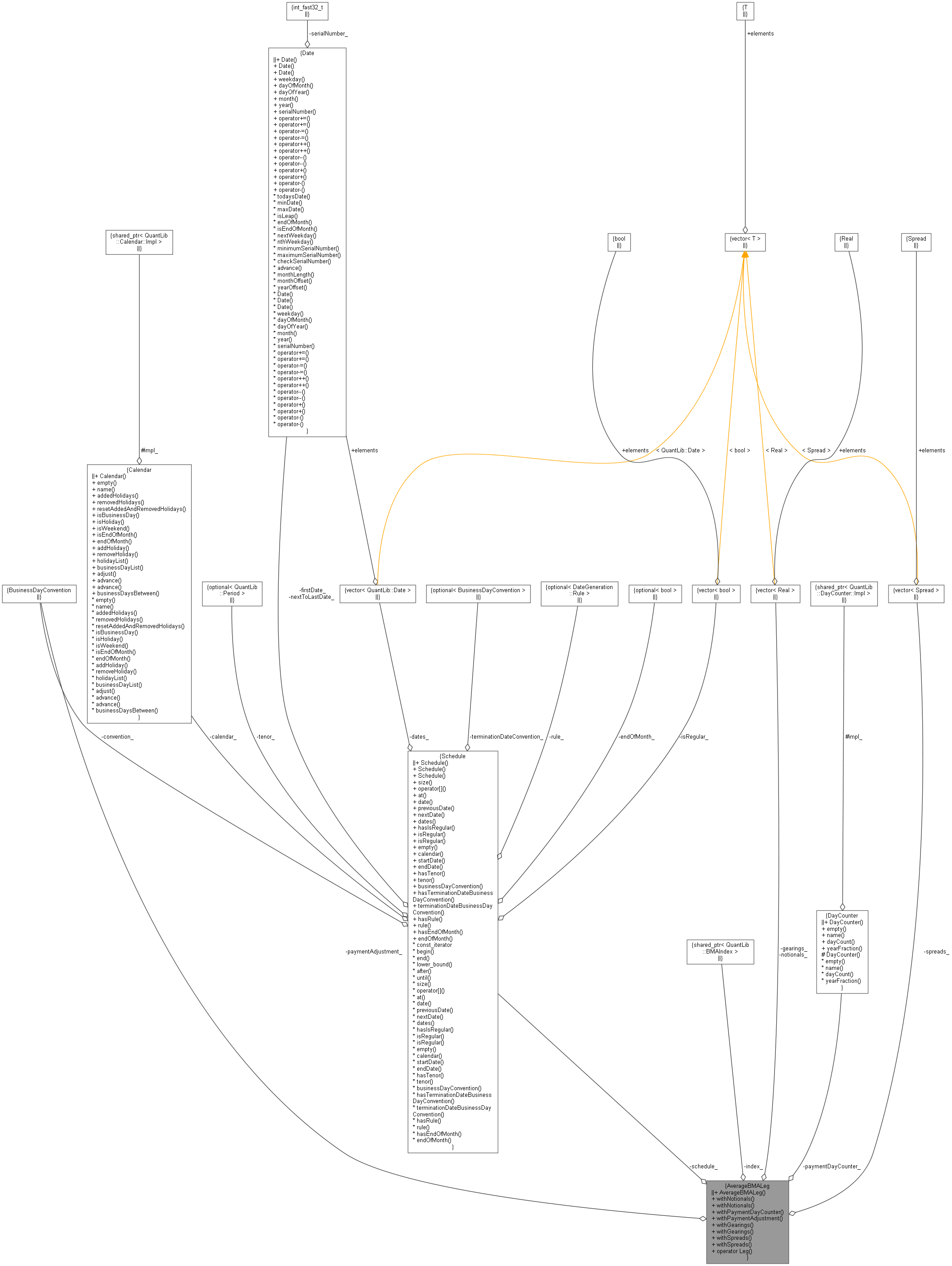

Collaboration diagram for AverageBMALeg:

Collaboration diagram for AverageBMALeg:

Public Member Functions | |

| AverageBMALeg (Schedule schedule, ext::shared_ptr< BMAIndex > index) | |

| AverageBMALeg & | withNotionals (Real notional) |

| AverageBMALeg & | withNotionals (const std::vector< Real > ¬ionals) |

| AverageBMALeg & | withPaymentDayCounter (const DayCounter &) |

| AverageBMALeg & | withPaymentAdjustment (BusinessDayConvention) |

| AverageBMALeg & | withGearings (Real gearing) |

| AverageBMALeg & | withGearings (const std::vector< Real > &gearings) |

| AverageBMALeg & | withSpreads (Spread spread) |

| AverageBMALeg & | withSpreads (const std::vector< Spread > &spreads) |

| operator Leg () const | |

Private Attributes | |

| Schedule | schedule_ |

| ext::shared_ptr< BMAIndex > | index_ |

| std::vector< Real > | notionals_ |

| DayCounter | paymentDayCounter_ |

| BusinessDayConvention | paymentAdjustment_ = Following |

| std::vector< Real > | gearings_ |

| std::vector< Spread > | spreads_ |

Detailed Description

helper class building a sequence of average BMA coupons

Definition at line 83 of file averagebmacoupon.hpp.

Constructor & Destructor Documentation

◆ AverageBMALeg()

| AverageBMALeg | ( | Schedule | schedule, |

| ext::shared_ptr< BMAIndex > | index | ||

| ) |

Definition at line 165 of file averagebmacoupon.cpp.

Member Function Documentation

◆ withNotionals() [1/2]

| AverageBMALeg & withNotionals | ( | Real | notional | ) |

◆ withNotionals() [2/2]

| AverageBMALeg & withNotionals | ( | const std::vector< Real > & | notionals | ) |

Definition at line 173 of file averagebmacoupon.cpp.

◆ withPaymentDayCounter()

| AverageBMALeg & withPaymentDayCounter | ( | const DayCounter & | dayCounter | ) |

◆ withPaymentAdjustment()

| AverageBMALeg & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

◆ withGearings() [1/2]

| AverageBMALeg & withGearings | ( | Real | gearing | ) |

Definition at line 191 of file averagebmacoupon.cpp.

◆ withGearings() [2/2]

| AverageBMALeg & withGearings | ( | const std::vector< Real > & | gearings | ) |

Definition at line 196 of file averagebmacoupon.cpp.

◆ withSpreads() [1/2]

| AverageBMALeg & withSpreads | ( | Spread | spread | ) |

Definition at line 202 of file averagebmacoupon.cpp.

◆ withSpreads() [2/2]

| AverageBMALeg & withSpreads | ( | const std::vector< Spread > & | spreads | ) |

Definition at line 207 of file averagebmacoupon.cpp.

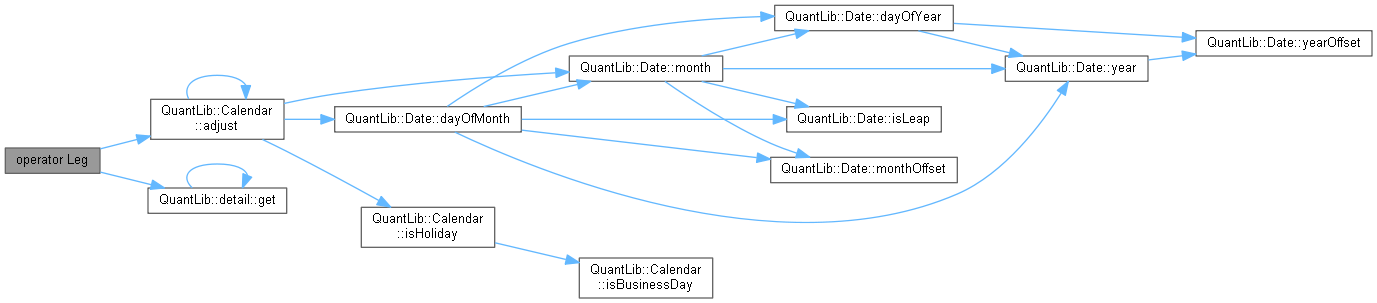

◆ operator Leg()

| operator Leg | ( | ) | const |

Member Data Documentation

◆ schedule_

|

private |

Definition at line 96 of file averagebmacoupon.hpp.

◆ index_

|

private |

Definition at line 97 of file averagebmacoupon.hpp.

◆ notionals_

|

private |

Definition at line 98 of file averagebmacoupon.hpp.

◆ paymentDayCounter_

|

private |

Definition at line 99 of file averagebmacoupon.hpp.

◆ paymentAdjustment_

|

private |

Definition at line 100 of file averagebmacoupon.hpp.

◆ gearings_

|

private |

Definition at line 101 of file averagebmacoupon.hpp.

◆ spreads_

|

private |

Definition at line 102 of file averagebmacoupon.hpp.