#include <fdmzabrop.hpp>

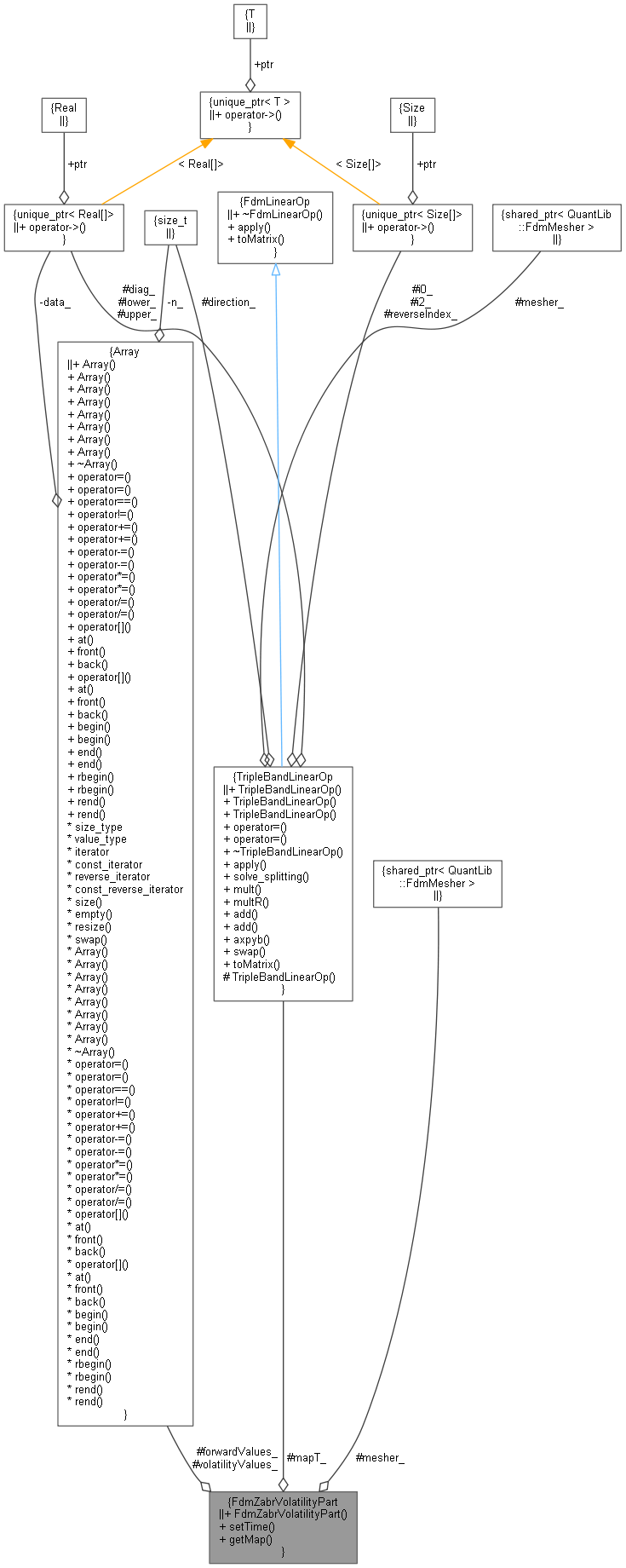

Collaboration diagram for FdmZabrVolatilityPart:

Collaboration diagram for FdmZabrVolatilityPart:

Public Member Functions | |

| FdmZabrVolatilityPart (const ext::shared_ptr< FdmMesher > &mesher, Real beta, Real nu, Real rho, Real gamma) | |

| void | setTime (Time t1, Time t2) |

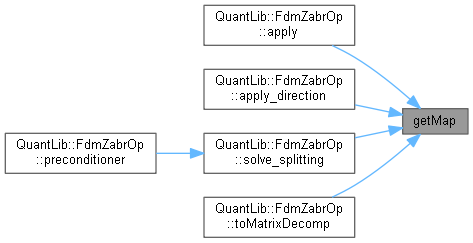

| const TripleBandLinearOp & | getMap () const |

Protected Attributes | |

| const Array | volatilityValues_ |

| const Array | forwardValues_ |

| TripleBandLinearOp | mapT_ |

| const ext::shared_ptr< FdmMesher > | mesher_ |

Detailed Description

Definition at line 51 of file fdmzabrop.hpp.

Constructor & Destructor Documentation

◆ FdmZabrVolatilityPart()

| FdmZabrVolatilityPart | ( | const ext::shared_ptr< FdmMesher > & | mesher, |

| Real | beta, | ||

| Real | nu, | ||

| Real | rho, | ||

| Real | gamma | ||

| ) |

Definition at line 42 of file fdmzabrop.cpp.

Member Function Documentation

◆ setTime()

◆ getMap()

| const TripleBandLinearOp & getMap | ( | ) | const |

Member Data Documentation

◆ volatilityValues_

|

protected |

Definition at line 60 of file fdmzabrop.hpp.

◆ forwardValues_

|

protected |

Definition at line 61 of file fdmzabrop.hpp.

◆ mapT_

|

protected |

Definition at line 62 of file fdmzabrop.hpp.

◆ mesher_

|

protected |

Definition at line 64 of file fdmzabrop.hpp.