helper class More...

#include <makevanillaswap.hpp>

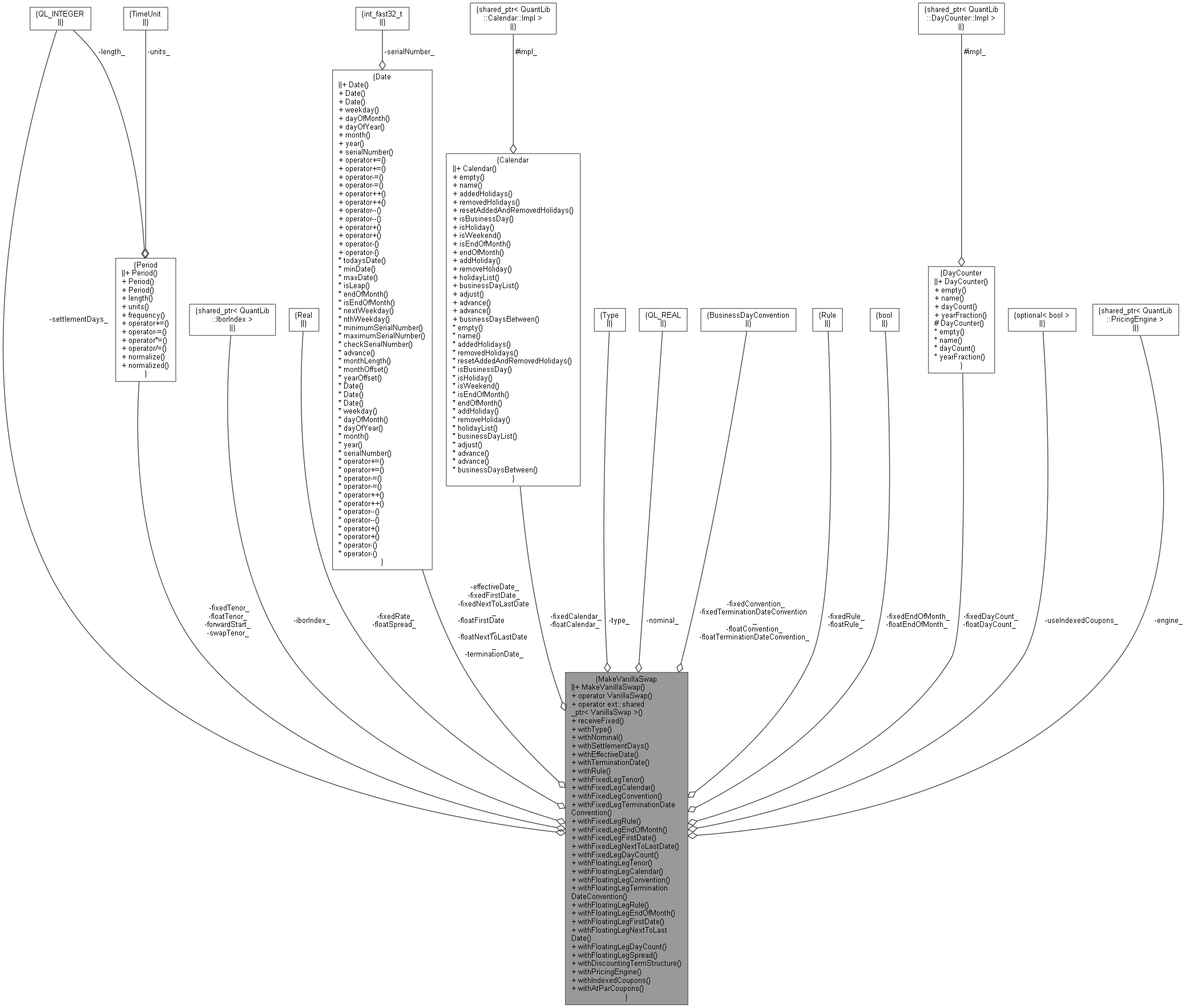

Collaboration diagram for MakeVanillaSwap:

Collaboration diagram for MakeVanillaSwap:

Detailed Description

helper class

This class provides a more comfortable way to instantiate standard market swap.

- Examples

- CVAIRS.cpp.

Definition at line 39 of file makevanillaswap.hpp.

Constructor & Destructor Documentation

◆ MakeVanillaSwap()

| MakeVanillaSwap | ( | const Period & | swapTenor, |

| const ext::shared_ptr< IborIndex > & | iborIndex, | ||

| Rate | fixedRate = Null<Rate>(), |

||

| const Period & | forwardStart = 0*Days |

||

| ) |

Definition at line 40 of file makevanillaswap.cpp.

Member Function Documentation

◆ operator VanillaSwap()

| operator VanillaSwap | ( | ) | const |

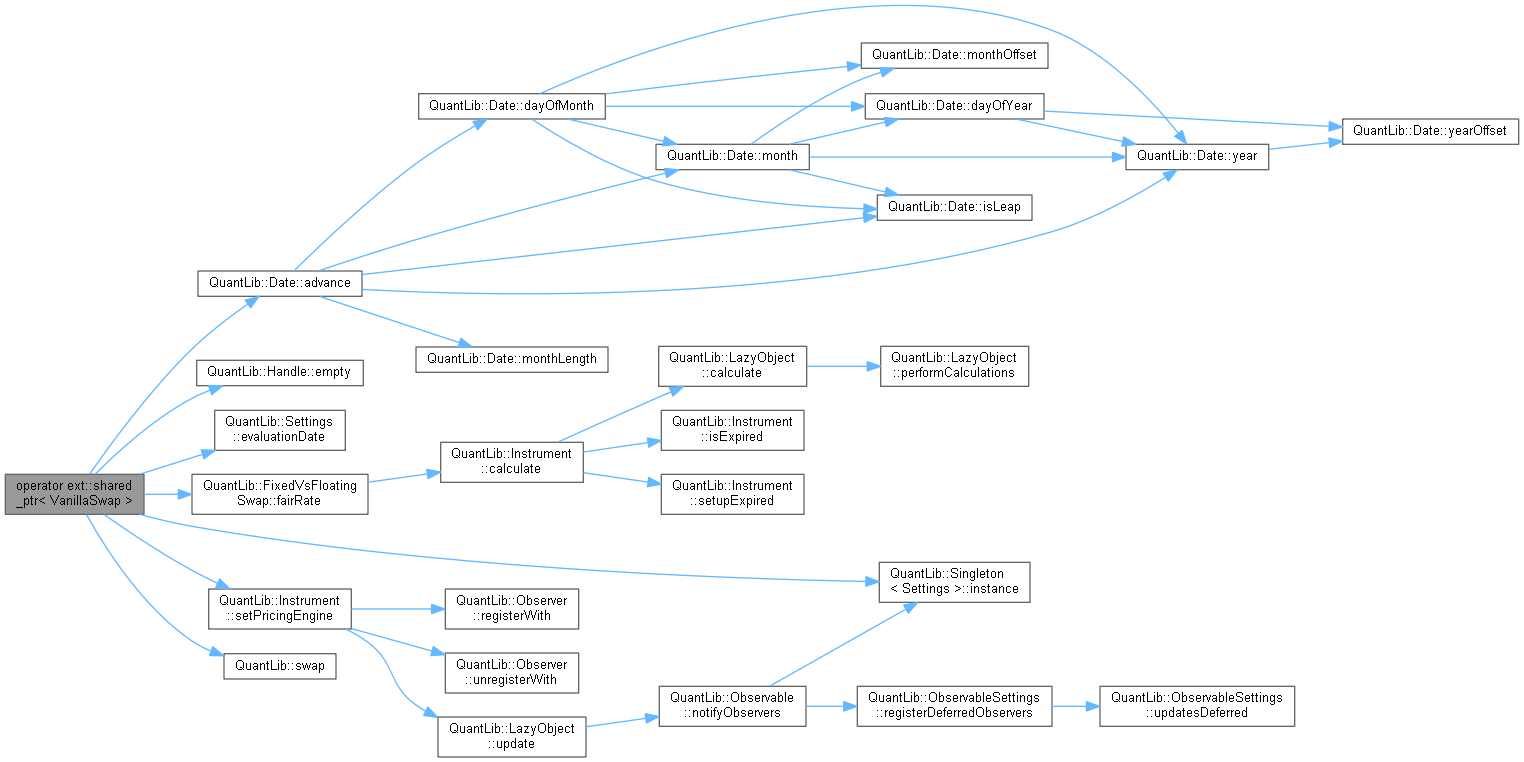

◆ operator ext::shared_ptr< VanillaSwap >()

| operator ext::shared_ptr< VanillaSwap > | ( | ) | const |

◆ receiveFixed()

| MakeVanillaSwap & receiveFixed | ( | bool | flag = true | ) |

Definition at line 190 of file makevanillaswap.cpp.

◆ withType()

| MakeVanillaSwap & withType | ( | Swap::Type | type | ) |

- Examples

- CVAIRS.cpp.

Definition at line 195 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withNominal()

| MakeVanillaSwap & withNominal | ( | Real | n | ) |

- Examples

- CVAIRS.cpp.

Definition at line 200 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withSettlementDays()

| MakeVanillaSwap & withSettlementDays | ( | Natural | settlementDays | ) |

- Examples

- CVAIRS.cpp.

Definition at line 205 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withEffectiveDate()

| MakeVanillaSwap & withEffectiveDate | ( | const Date & | effectiveDate | ) |

◆ withTerminationDate()

| MakeVanillaSwap & withTerminationDate | ( | const Date & | terminationDate | ) |

◆ withRule()

| MakeVanillaSwap & withRule | ( | DateGeneration::Rule | r | ) |

◆ withPaymentConvention()

| MakeVanillaSwap & withPaymentConvention | ( | BusinessDayConvention | bdc | ) |

Definition at line 231 of file makevanillaswap.cpp.

◆ withFixedLegTenor()

| MakeVanillaSwap & withFixedLegTenor | ( | const Period & | t | ) |

- Examples

- CVAIRS.cpp.

Definition at line 250 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withFixedLegCalendar()

| MakeVanillaSwap & withFixedLegCalendar | ( | const Calendar & | cal | ) |

- Examples

- CVAIRS.cpp.

Definition at line 256 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withFixedLegConvention()

| MakeVanillaSwap & withFixedLegConvention | ( | BusinessDayConvention | bdc | ) |

- Examples

- CVAIRS.cpp.

Definition at line 262 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withFixedLegTerminationDateConvention()

| MakeVanillaSwap & withFixedLegTerminationDateConvention | ( | BusinessDayConvention | bdc | ) |

- Examples

- CVAIRS.cpp.

Definition at line 268 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withFixedLegRule()

| MakeVanillaSwap & withFixedLegRule | ( | DateGeneration::Rule | r | ) |

Definition at line 273 of file makevanillaswap.cpp.

◆ withFixedLegEndOfMonth()

| MakeVanillaSwap & withFixedLegEndOfMonth | ( | bool | flag = true | ) |

◆ withFixedLegFirstDate()

| MakeVanillaSwap & withFixedLegFirstDate | ( | const Date & | d | ) |

Definition at line 283 of file makevanillaswap.cpp.

◆ withFixedLegNextToLastDate()

| MakeVanillaSwap & withFixedLegNextToLastDate | ( | const Date & | d | ) |

Definition at line 289 of file makevanillaswap.cpp.

◆ withFixedLegDayCount()

| MakeVanillaSwap & withFixedLegDayCount | ( | const DayCounter & | dc | ) |

- Examples

- CVAIRS.cpp.

Definition at line 295 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withFloatingLegTenor()

| MakeVanillaSwap & withFloatingLegTenor | ( | const Period & | t | ) |

◆ withFloatingLegCalendar()

| MakeVanillaSwap & withFloatingLegCalendar | ( | const Calendar & | cal | ) |

- Examples

- CVAIRS.cpp.

Definition at line 306 of file makevanillaswap.cpp.

Here is the caller graph for this function:

◆ withFloatingLegConvention()

| MakeVanillaSwap & withFloatingLegConvention | ( | BusinessDayConvention | bdc | ) |

◆ withFloatingLegTerminationDateConvention()

| MakeVanillaSwap & withFloatingLegTerminationDateConvention | ( | BusinessDayConvention | bdc | ) |

◆ withFloatingLegRule()

| MakeVanillaSwap & withFloatingLegRule | ( | DateGeneration::Rule | r | ) |

◆ withFloatingLegEndOfMonth()

| MakeVanillaSwap & withFloatingLegEndOfMonth | ( | bool | flag = true | ) |

◆ withFloatingLegFirstDate()

| MakeVanillaSwap & withFloatingLegFirstDate | ( | const Date & | d | ) |

◆ withFloatingLegNextToLastDate()

| MakeVanillaSwap & withFloatingLegNextToLastDate | ( | const Date & | d | ) |

◆ withFloatingLegDayCount()

| MakeVanillaSwap & withFloatingLegDayCount | ( | const DayCounter & | dc | ) |

◆ withFloatingLegSpread()

| MakeVanillaSwap & withFloatingLegSpread | ( | Spread | sp | ) |

Definition at line 351 of file makevanillaswap.cpp.

◆ withDiscountingTermStructure()

| MakeVanillaSwap & withDiscountingTermStructure | ( | const Handle< YieldTermStructure > & | discountCurve | ) |

◆ withPricingEngine()

| MakeVanillaSwap & withPricingEngine | ( | const ext::shared_ptr< PricingEngine > & | engine | ) |

Definition at line 244 of file makevanillaswap.cpp.

◆ withIndexedCoupons()

| MakeVanillaSwap & withIndexedCoupons | ( | const ext::optional< bool > & | b = true | ) |

◆ withAtParCoupons()

| MakeVanillaSwap & withAtParCoupons | ( | bool | b = true | ) |

Definition at line 361 of file makevanillaswap.cpp.

Member Data Documentation

◆ swapTenor_

|

private |

Definition at line 89 of file makevanillaswap.hpp.

◆ iborIndex_

|

private |

Definition at line 90 of file makevanillaswap.hpp.

◆ fixedRate_

|

private |

Definition at line 91 of file makevanillaswap.hpp.

◆ forwardStart_

|

private |

Definition at line 92 of file makevanillaswap.hpp.

◆ settlementDays_

|

private |

Definition at line 94 of file makevanillaswap.hpp.

◆ effectiveDate_

|

private |

Definition at line 95 of file makevanillaswap.hpp.

◆ terminationDate_

|

private |

Definition at line 95 of file makevanillaswap.hpp.

◆ fixedCalendar_

|

private |

Definition at line 96 of file makevanillaswap.hpp.

◆ floatCalendar_

|

private |

Definition at line 96 of file makevanillaswap.hpp.

◆ type_

|

private |

Definition at line 98 of file makevanillaswap.hpp.

◆ nominal_

|

private |

Definition at line 99 of file makevanillaswap.hpp.

◆ fixedTenor_

|

private |

Definition at line 100 of file makevanillaswap.hpp.

◆ floatTenor_

|

private |

Definition at line 100 of file makevanillaswap.hpp.

◆ fixedConvention_

|

private |

Definition at line 101 of file makevanillaswap.hpp.

◆ fixedTerminationDateConvention_

|

private |

Definition at line 102 of file makevanillaswap.hpp.

◆ floatConvention_

|

private |

Definition at line 103 of file makevanillaswap.hpp.

◆ floatTerminationDateConvention_

|

private |

Definition at line 103 of file makevanillaswap.hpp.

◆ fixedRule_

|

private |

Definition at line 104 of file makevanillaswap.hpp.

◆ floatRule_

|

private |

Definition at line 105 of file makevanillaswap.hpp.

◆ fixedEndOfMonth_

|

private |

Definition at line 106 of file makevanillaswap.hpp.

◆ floatEndOfMonth_

|

private |

Definition at line 106 of file makevanillaswap.hpp.

◆ fixedFirstDate_

|

private |

Definition at line 107 of file makevanillaswap.hpp.

◆ fixedNextToLastDate_

|

private |

Definition at line 107 of file makevanillaswap.hpp.

◆ floatFirstDate_

|

private |

Definition at line 108 of file makevanillaswap.hpp.

◆ floatNextToLastDate_

|

private |

Definition at line 108 of file makevanillaswap.hpp.

◆ floatSpread_

|

private |

Definition at line 109 of file makevanillaswap.hpp.

◆ fixedDayCount_

|

private |

Definition at line 110 of file makevanillaswap.hpp.

◆ floatDayCount_

|

private |

Definition at line 110 of file makevanillaswap.hpp.

◆ useIndexedCoupons_

|

private |

Definition at line 111 of file makevanillaswap.hpp.

◆ paymentConvention_

|

private |

Definition at line 112 of file makevanillaswap.hpp.

◆ engine_

|

private |

Definition at line 114 of file makevanillaswap.hpp.