#include <swaptionpseudojacobian.hpp>

Collaboration diagram for CapPseudoDerivative:

Collaboration diagram for CapPseudoDerivative:

Public Member Functions | |

| CapPseudoDerivative (const ext::shared_ptr< MarketModel > &inputModel, Real strike, Size startIndex, Size endIndex, Real firstDF) | |

| const Matrix & | volatilityDerivative (Size i) const |

| const Matrix & | priceDerivative (Size i) const |

| Real | impliedVolatility () const |

Private Attributes | |

| ext::shared_ptr< MarketModel > | inputModel_ |

| std::vector< Matrix > | volatilityDerivatives_ |

| std::vector< Matrix > | priceDerivatives_ |

| Real | impliedVolatility_ |

| Real | vega_ |

| Real | firstDF_ |

Detailed Description

In order to compute market vegas, we need a class that gives the derivative of a cap implied vol against changes in pseudo-root elements. This is that class.

The operation is non-trivial because the cap implied vol has a complicated relationship with the caplet implied vols.

This is tested in the pathwise vegas routine in MarketModels.cpp

Definition at line 78 of file swaptionpseudojacobian.hpp.

Constructor & Destructor Documentation

◆ CapPseudoDerivative()

| CapPseudoDerivative | ( | const ext::shared_ptr< MarketModel > & | inputModel, |

| Real | strike, | ||

| Size | startIndex, | ||

| Size | endIndex, | ||

| Real | firstDF | ||

| ) |

Definition at line 232 of file swaptionpseudojacobian.cpp.

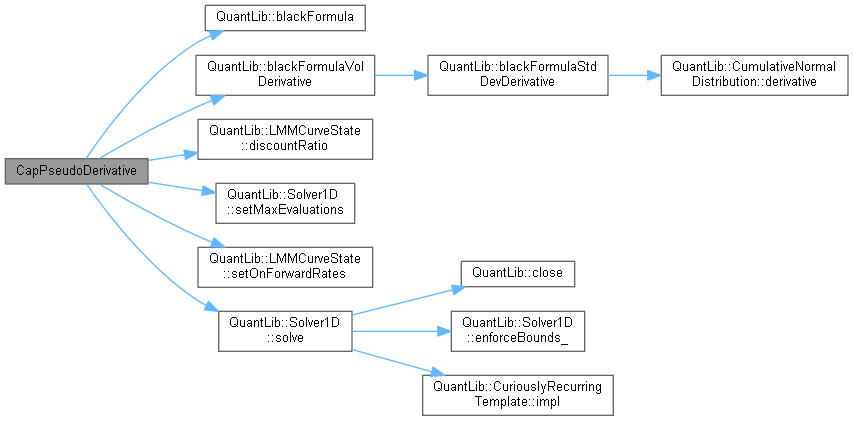

Here is the call graph for this function:

Member Function Documentation

◆ volatilityDerivative()

Definition at line 367 of file swaptionpseudojacobian.cpp.

Here is the caller graph for this function:

◆ priceDerivative()

Definition at line 362 of file swaptionpseudojacobian.cpp.

◆ impliedVolatility()

| Real impliedVolatility | ( | ) | const |

Definition at line 374 of file swaptionpseudojacobian.cpp.

Member Data Documentation

◆ inputModel_

|

private |

Definition at line 96 of file swaptionpseudojacobian.hpp.

◆ volatilityDerivatives_

|

private |

Definition at line 98 of file swaptionpseudojacobian.hpp.

◆ priceDerivatives_

|

private |

Definition at line 100 of file swaptionpseudojacobian.hpp.

◆ impliedVolatility_

|

private |

Definition at line 102 of file swaptionpseudojacobian.hpp.

◆ vega_

|

private |

Definition at line 103 of file swaptionpseudojacobian.hpp.

◆ firstDF_

|

private |

Definition at line 104 of file swaptionpseudojacobian.hpp.