#include <multipleresetscoupon.hpp>

Collaboration diagram for SubPeriodsLeg:

Collaboration diagram for SubPeriodsLeg:

Private Attributes | |

| Schedule | schedule_ |

| ext::shared_ptr< IborIndex > | index_ |

| std::vector< Real > | notionals_ |

| DayCounter | paymentDayCounter_ |

| Calendar | paymentCalendar_ |

| BusinessDayConvention | paymentAdjustment_ = Following |

| Integer | paymentLag_ = 0 |

| std::vector< Natural > | fixingDays_ |

| std::vector< Real > | gearings_ |

| std::vector< Spread > | couponSpreads_ |

| std::vector< Spread > | rateSpreads_ |

| RateAveraging::Type | averagingMethod_ = RateAveraging::Compound |

| Period | exCouponPeriod_ |

| Calendar | exCouponCalendar_ |

| BusinessDayConvention | exCouponAdjustment_ = Unadjusted |

| bool | exCouponEndOfMonth_ = false |

Detailed Description

- Deprecated:

- Use MultipleResetsLeg instead. Deprecated in version 1.37.

Definition at line 221 of file multipleresetscoupon.hpp.

Constructor & Destructor Documentation

◆ SubPeriodsLeg()

| QL_DEPRECATED_DISABLE_WARNING SubPeriodsLeg | ( | Schedule | schedule, |

| ext::shared_ptr< IborIndex > | index | ||

| ) |

Definition at line 351 of file multipleresetscoupon.cpp.

Member Function Documentation

◆ withNotionals() [1/2]

| SubPeriodsLeg & withNotionals | ( | Real | notional | ) |

Definition at line 356 of file multipleresetscoupon.cpp.

◆ withNotionals() [2/2]

| SubPeriodsLeg & withNotionals | ( | const std::vector< Real > & | notionals | ) |

Definition at line 361 of file multipleresetscoupon.cpp.

◆ withPaymentDayCounter()

| SubPeriodsLeg & withPaymentDayCounter | ( | const DayCounter & | dc | ) |

Definition at line 366 of file multipleresetscoupon.cpp.

◆ withPaymentAdjustment()

| SubPeriodsLeg & withPaymentAdjustment | ( | BusinessDayConvention | convention | ) |

Definition at line 371 of file multipleresetscoupon.cpp.

◆ withPaymentCalendar()

| SubPeriodsLeg & withPaymentCalendar | ( | const Calendar & | cal | ) |

Definition at line 376 of file multipleresetscoupon.cpp.

◆ withPaymentLag()

| SubPeriodsLeg & withPaymentLag | ( | Integer | lag | ) |

Definition at line 381 of file multipleresetscoupon.cpp.

◆ withFixingDays() [1/2]

| SubPeriodsLeg & withFixingDays | ( | Natural | fixingDays | ) |

Definition at line 386 of file multipleresetscoupon.cpp.

◆ withFixingDays() [2/2]

| SubPeriodsLeg & withFixingDays | ( | const std::vector< Natural > & | fixingDays | ) |

Definition at line 391 of file multipleresetscoupon.cpp.

◆ withGearings() [1/2]

| SubPeriodsLeg & withGearings | ( | Real | gearing | ) |

Definition at line 396 of file multipleresetscoupon.cpp.

◆ withGearings() [2/2]

| SubPeriodsLeg & withGearings | ( | const std::vector< Real > & | gearings | ) |

Definition at line 401 of file multipleresetscoupon.cpp.

◆ withCouponSpreads() [1/2]

| SubPeriodsLeg & withCouponSpreads | ( | Spread | spread | ) |

Definition at line 406 of file multipleresetscoupon.cpp.

◆ withCouponSpreads() [2/2]

| SubPeriodsLeg & withCouponSpreads | ( | const std::vector< Spread > & | spreads | ) |

Definition at line 411 of file multipleresetscoupon.cpp.

◆ withRateSpreads() [1/2]

| SubPeriodsLeg & withRateSpreads | ( | Spread | spread | ) |

Definition at line 416 of file multipleresetscoupon.cpp.

◆ withRateSpreads() [2/2]

| SubPeriodsLeg & withRateSpreads | ( | const std::vector< Spread > & | spreads | ) |

Definition at line 421 of file multipleresetscoupon.cpp.

◆ withExCouponPeriod()

| SubPeriodsLeg & withExCouponPeriod | ( | const Period & | period, |

| const Calendar & | cal, | ||

| BusinessDayConvention | convention, | ||

| bool | endOfMonth = false |

||

| ) |

Definition at line 431 of file multipleresetscoupon.cpp.

◆ withAveragingMethod()

| SubPeriodsLeg & withAveragingMethod | ( | RateAveraging::Type | averagingMethod | ) |

Definition at line 426 of file multipleresetscoupon.cpp.

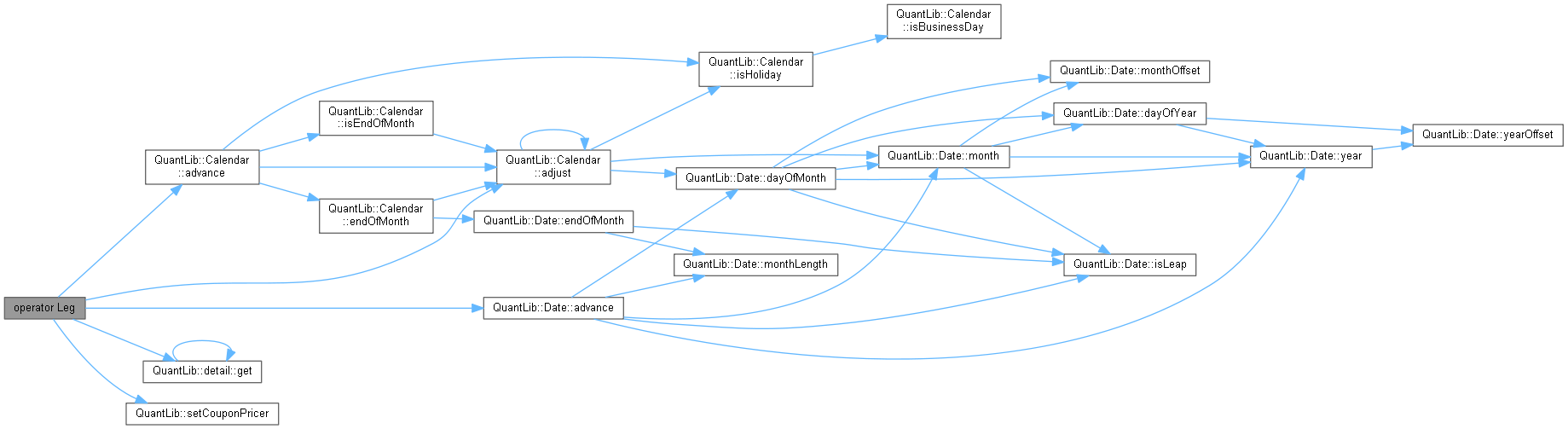

◆ operator Leg()

| operator Leg | ( | ) | const |

Member Data Documentation

◆ schedule_

|

private |

Definition at line 246 of file multipleresetscoupon.hpp.

◆ index_

|

private |

Definition at line 247 of file multipleresetscoupon.hpp.

◆ notionals_

|

private |

Definition at line 248 of file multipleresetscoupon.hpp.

◆ paymentDayCounter_

|

private |

Definition at line 249 of file multipleresetscoupon.hpp.

◆ paymentCalendar_

|

private |

Definition at line 250 of file multipleresetscoupon.hpp.

◆ paymentAdjustment_

|

private |

Definition at line 251 of file multipleresetscoupon.hpp.

◆ paymentLag_

|

private |

Definition at line 252 of file multipleresetscoupon.hpp.

◆ fixingDays_

|

private |

Definition at line 253 of file multipleresetscoupon.hpp.

◆ gearings_

|

private |

Definition at line 254 of file multipleresetscoupon.hpp.

◆ couponSpreads_

|

private |

Definition at line 255 of file multipleresetscoupon.hpp.

◆ rateSpreads_

|

private |

Definition at line 256 of file multipleresetscoupon.hpp.

◆ averagingMethod_

|

private |

Definition at line 257 of file multipleresetscoupon.hpp.

◆ exCouponPeriod_

|

private |

Definition at line 258 of file multipleresetscoupon.hpp.

◆ exCouponCalendar_

|

private |

Definition at line 259 of file multipleresetscoupon.hpp.

◆ exCouponAdjustment_

|

private |

Definition at line 260 of file multipleresetscoupon.hpp.

◆ exCouponEndOfMonth_

|

private |

Definition at line 261 of file multipleresetscoupon.hpp.