#include <equitycashflow.hpp>

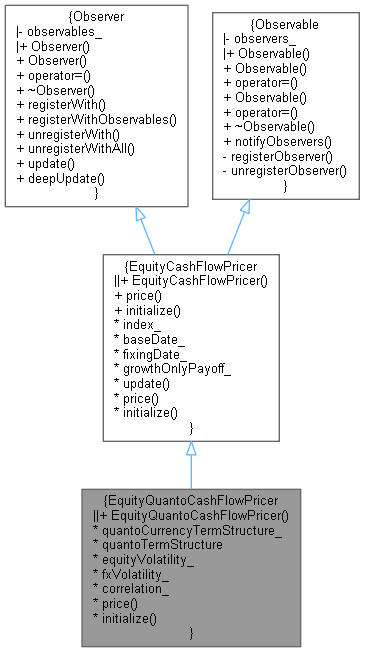

Inheritance diagram for EquityQuantoCashFlowPricer:

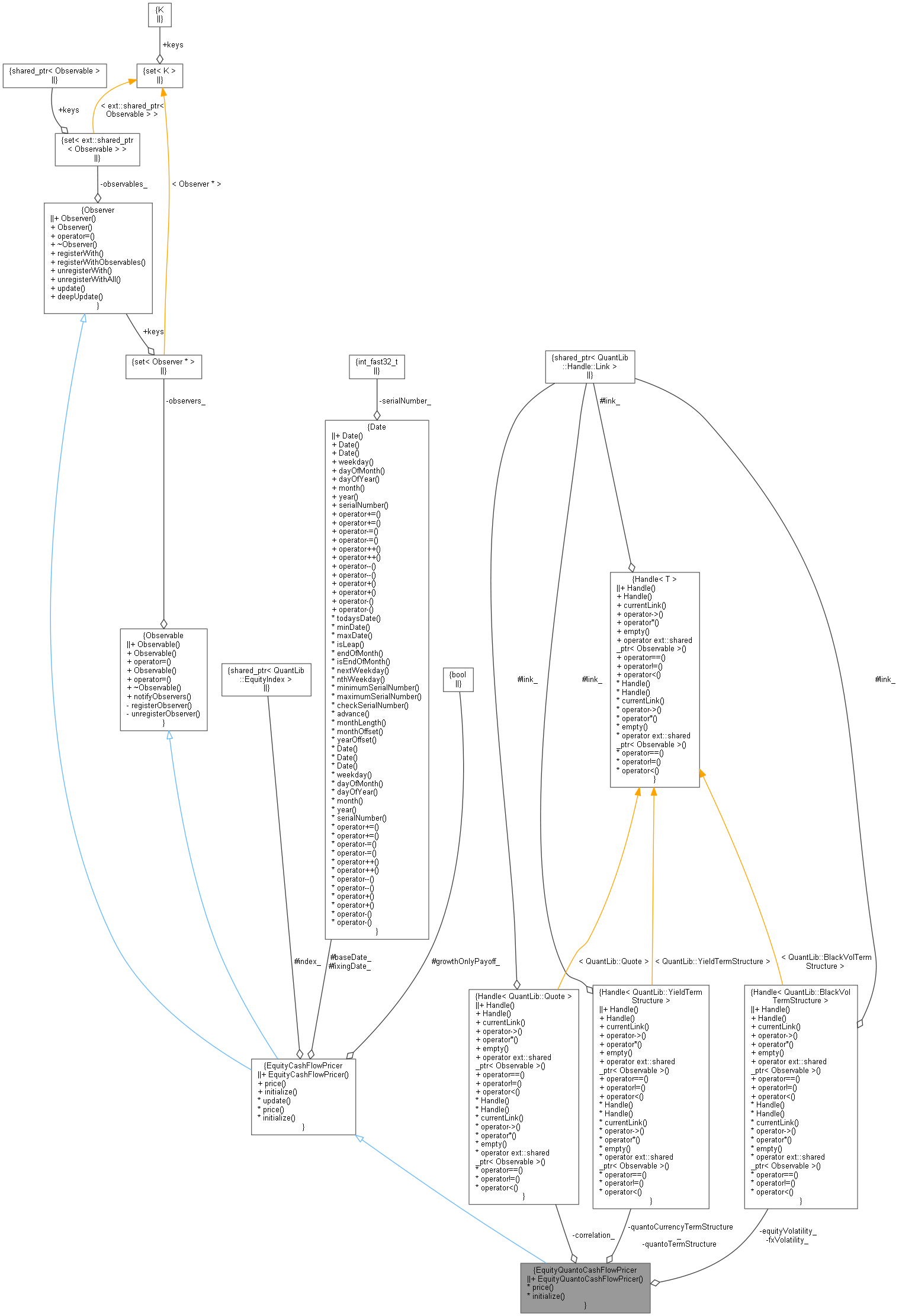

Inheritance diagram for EquityQuantoCashFlowPricer: Collaboration diagram for EquityQuantoCashFlowPricer:

Collaboration diagram for EquityQuantoCashFlowPricer:

Public Member Functions | |

| EquityQuantoCashFlowPricer (Handle< YieldTermStructure > quantoCurrencyTermStructure, Handle< BlackVolTermStructure > equityVolatility, Handle< BlackVolTermStructure > fxVolatility, Handle< Quote > correlation) | |

| Public Member Functions inherited from EquityCashFlowPricer | |

| EquityCashFlowPricer ()=default | |

| void | update () override |

| Public Member Functions inherited from Observer | |

| Observer ()=default | |

| Observer (const Observer &) | |

| Observer & | operator= (const Observer &) |

| virtual | ~Observer () |

| std::pair< iterator, bool > | registerWith (const ext::shared_ptr< Observable > &) |

| void | registerWithObservables (const ext::shared_ptr< Observer > &) |

| Size | unregisterWith (const ext::shared_ptr< Observable > &) |

| void | unregisterWithAll () |

| virtual void | update ()=0 |

| virtual void | deepUpdate () |

| Public Member Functions inherited from Observable | |

| Observable ()=default | |

| Observable (const Observable &) | |

| Observable & | operator= (const Observable &) |

| Observable (Observable &&)=delete | |

| Observable & | operator= (Observable &&)=delete |

| virtual | ~Observable ()=default |

| void | notifyObservers () |

Interface | |

| Handle< YieldTermStructure > | quantoCurrencyTermStructure_ |

| Handle< YieldTermStructure > | quantoTermStructure |

| Handle< BlackVolTermStructure > | equityVolatility_ |

| Handle< BlackVolTermStructure > | fxVolatility_ |

| Handle< Quote > | correlation_ |

| Real | price () const override |

| void | initialize (const EquityCashFlow &) override |

Additional Inherited Members | |

| Public Types inherited from Observer | |

| typedef set_type::iterator | iterator |

| Protected Attributes inherited from EquityCashFlowPricer | |

| ext::shared_ptr< EquityIndex > | index_ |

| Date | baseDate_ |

| Date | fixingDate_ |

| bool | growthOnlyPayoff_ |

Detailed Description

Definition at line 89 of file equitycashflow.hpp.

Constructor & Destructor Documentation

◆ EquityQuantoCashFlowPricer()

| EquityQuantoCashFlowPricer | ( | Handle< YieldTermStructure > | quantoCurrencyTermStructure, |

| Handle< BlackVolTermStructure > | equityVolatility, | ||

| Handle< BlackVolTermStructure > | fxVolatility, | ||

| Handle< Quote > | correlation | ||

| ) |

Member Function Documentation

◆ price()

|

overridevirtual |

Implements EquityCashFlowPricer.

Definition at line 116 of file equitycashflow.cpp.

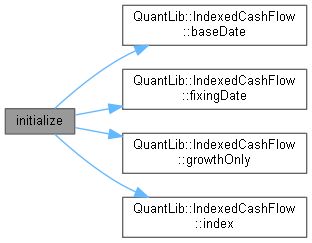

◆ initialize()

|

overridevirtual |

Implements EquityCashFlowPricer.

Definition at line 91 of file equitycashflow.cpp.

Here is the call graph for this function:

Member Data Documentation

◆ quantoCurrencyTermStructure_

|

private |

Definition at line 101 of file equitycashflow.hpp.

◆ quantoTermStructure

|

private |

Definition at line 101 of file equitycashflow.hpp.

◆ equityVolatility_

|

private |

Definition at line 102 of file equitycashflow.hpp.

◆ fxVolatility_

|

private |

Definition at line 102 of file equitycashflow.hpp.

◆ correlation_

Definition at line 103 of file equitycashflow.hpp.