#include <garmanklass.hpp>

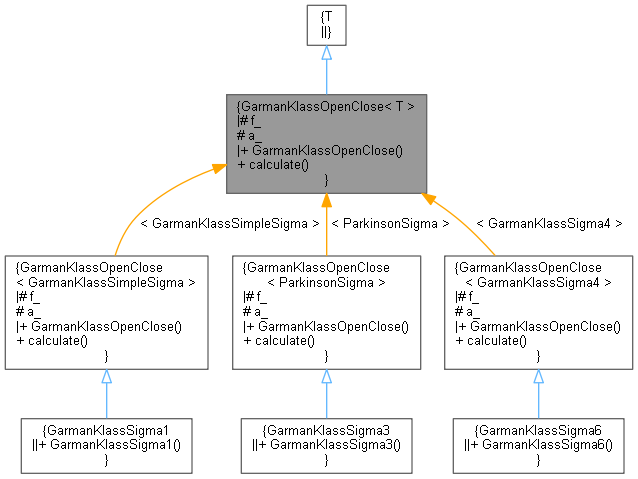

Inheritance diagram for GarmanKlassOpenClose< T >:

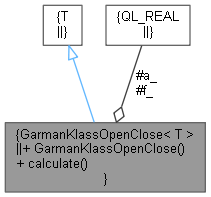

Inheritance diagram for GarmanKlassOpenClose< T >: Collaboration diagram for GarmanKlassOpenClose< T >:

Collaboration diagram for GarmanKlassOpenClose< T >:

Public Member Functions | |

| GarmanKlassOpenClose (Real y, Real marketOpenFraction, Real a) | |

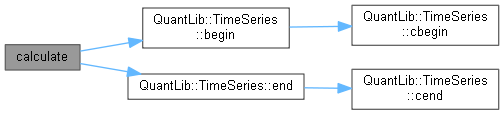

| TimeSeries< Volatility > | calculate (const TimeSeries< IntervalPrice > "eSeries) override |

Protected Attributes | |

| Real | f_ |

| Real | a_ |

Detailed Description

template<class T>

class QuantLib::GarmanKlassOpenClose< T >

class QuantLib::GarmanKlassOpenClose< T >

Definition at line 78 of file garmanklass.hpp.

Constructor & Destructor Documentation

◆ GarmanKlassOpenClose()

| GarmanKlassOpenClose | ( | Real | y, |

| Real | marketOpenFraction, | ||

| Real | a | ||

| ) |

Definition at line 83 of file garmanklass.hpp.

Member Function Documentation

◆ calculate()

|

override |

Member Data Documentation

◆ f_

|

protected |

Definition at line 80 of file garmanklass.hpp.

◆ a_

|

protected |

Definition at line 81 of file garmanklass.hpp.