Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Abstract base class for the option stripper. More...

#include <qle/termstructures/eqcommoptionsurfacestripper.hpp>

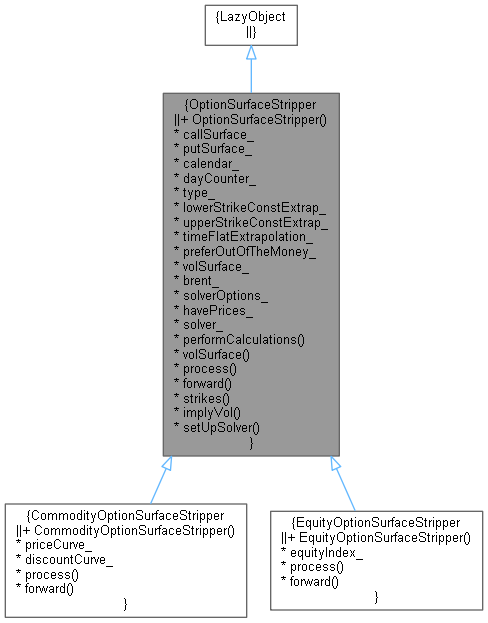

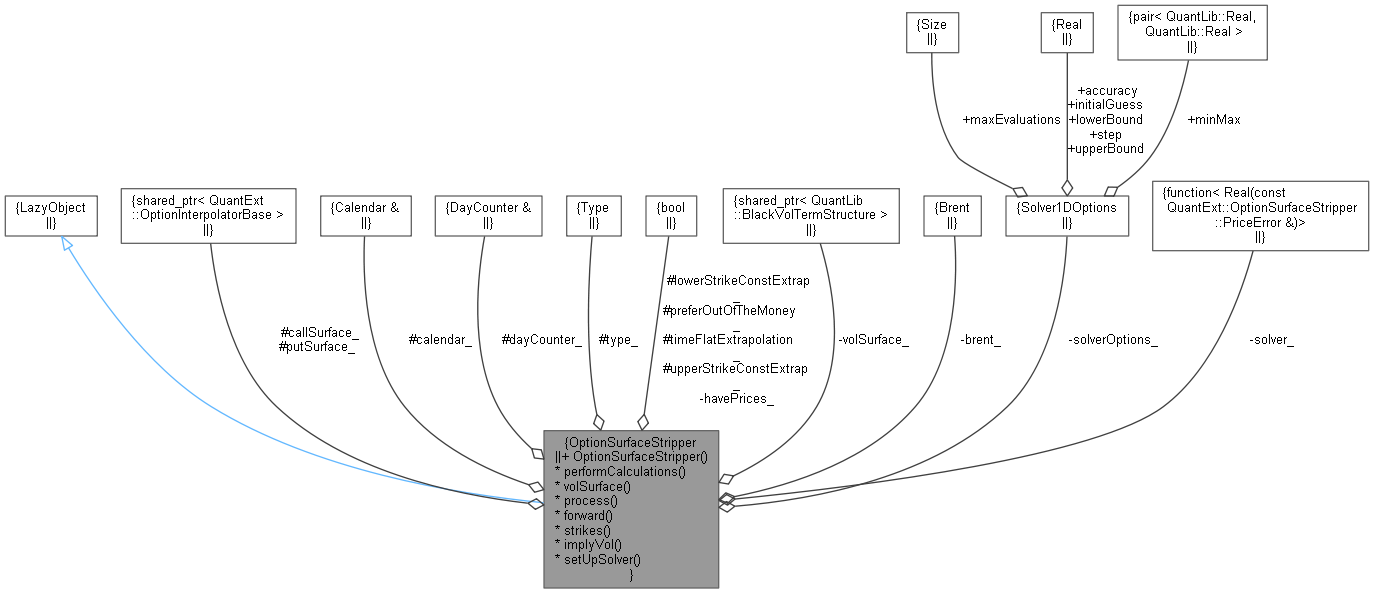

Inheritance diagram for OptionSurfaceStripper: Collaboration diagram for OptionSurfaceStripper:

Inheritance diagram for OptionSurfaceStripper: Collaboration diagram for OptionSurfaceStripper:Classes | |

| class | PriceError |

| Function object used in solving. More... | |

Public Member Functions | |

| OptionSurfaceStripper (const QuantLib::ext::shared_ptr< OptionInterpolatorBase > &callSurface, const QuantLib::ext::shared_ptr< OptionInterpolatorBase > &putSurface, const QuantLib::Calendar &calendar, const QuantLib::DayCounter &dayCounter, QuantLib::Exercise::Type type=QuantLib::Exercise::European, bool lowerStrikeConstExtrap=true, bool upperStrikeConstExtrap=true, bool timeFlatExtrapolation=false, bool preferOutOfTheMoney=false, Solver1DOptions solverOptions={}) | |

LazyObject interface | |

| QuantLib::ext::shared_ptr< OptionInterpolatorBase > | callSurface_ |

| QuantLib::ext::shared_ptr< OptionInterpolatorBase > | putSurface_ |

| const QuantLib::Calendar & | calendar_ |

| const QuantLib::DayCounter & | dayCounter_ |

| QuantLib::Exercise::Type | type_ |

| bool | lowerStrikeConstExtrap_ |

| bool | upperStrikeConstExtrap_ |

| bool | timeFlatExtrapolation_ |

| bool | preferOutOfTheMoney_ |

| QuantLib::ext::shared_ptr< QuantLib::BlackVolTermStructure > | volSurface_ |

| Brent | brent_ |

| Solver used when implying volatility from price. More... | |

| Solver1DOptions | solverOptions_ |

| bool | havePrices_ |

Set to true if we must strip volatilities from prices. More... | |

| std::function< Real(const PriceError &)> | solver_ |

| Store the function that will be called each time to solve for volatility. More... | |

| void | performCalculations () const override |

| QuantLib::ext::shared_ptr< QuantLib::BlackVolTermStructure > | volSurface () |

| Return the stripped volatility structure. More... | |

| virtual QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > | process (const QuantLib::ext::shared_ptr< QuantLib::SimpleQuote > &volatilityQuote) const =0 |

| Generate the relevant Black Scholes process for the underlying. More... | |

| virtual QuantLib::Real | forward (const QuantLib::Date &date) const =0 |

| Return the forward price at a given date. More... | |

| std::vector< QuantLib::Real > | strikes (const QuantLib::Date &expiry, bool isCall) const |

| Retrieve the vector of strikes at a given expiry date. More... | |

| QuantLib::Real | implyVol (QuantLib::Date expiry, QuantLib::Real strike, QuantLib::Option::Type type, QuantLib::ext::shared_ptr< QuantLib::PricingEngine > engine, QuantLib::SimpleQuote &volQuote) const |

| void | setUpSolver () |

Abstract base class for the option stripper.

Definition at line 64 of file eqcommoptionsurfacestripper.hpp.

| OptionSurfaceStripper | ( | const QuantLib::ext::shared_ptr< OptionInterpolatorBase > & | callSurface, |

| const QuantLib::ext::shared_ptr< OptionInterpolatorBase > & | putSurface, | ||

| const QuantLib::Calendar & | calendar, | ||

| const QuantLib::DayCounter & | dayCounter, | ||

| QuantLib::Exercise::Type | type = QuantLib::Exercise::European, |

||

| bool | lowerStrikeConstExtrap = true, |

||

| bool | upperStrikeConstExtrap = true, |

||

| bool | timeFlatExtrapolation = false, |

||

| bool | preferOutOfTheMoney = false, |

||

| Solver1DOptions | solverOptions = {} |

||

| ) |

Definition at line 84 of file eqcommoptionsurfacestripper.cpp.

Here is the call graph for this function:

|

override |

Definition at line 141 of file eqcommoptionsurfacestripper.cpp.

Here is the call graph for this function:| QuantLib::ext::shared_ptr< BlackVolTermStructure > volSurface | ( | ) |

Return the stripped volatility structure.

Definition at line 307 of file eqcommoptionsurfacestripper.cpp.

|

protectedpure virtual |

Generate the relevant Black Scholes process for the underlying.

Implemented in EquityOptionSurfaceStripper, and CommodityOptionSurfaceStripper.

Here is the caller graph for this function:

|

protectedpure virtual |

Return the forward price at a given date.

Implemented in EquityOptionSurfaceStripper, and CommodityOptionSurfaceStripper.

Here is the caller graph for this function:

|

private |

Retrieve the vector of strikes at a given expiry date.

Definition at line 219 of file eqcommoptionsurfacestripper.cpp.

|

private |

Imply the volatility at a given expiry and strike for the given option type. The exercise type is indicated by the member variable type_ and the target price is read off the relevant price surface i.e. either callSurface_ or putSurface_.

If the root finding fails, a Null<Real>() is returned.

Definition at line 233 of file eqcommoptionsurfacestripper.cpp.

Here is the caller graph for this function:

|

private |

Definition at line 264 of file eqcommoptionsurfacestripper.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

protected |

Definition at line 94 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 95 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 96 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 97 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 98 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 99 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 100 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 101 of file eqcommoptionsurfacestripper.hpp.

|

protected |

Definition at line 102 of file eqcommoptionsurfacestripper.hpp.

|

mutableprivate |

Definition at line 137 of file eqcommoptionsurfacestripper.hpp.

|

private |

Solver used when implying volatility from price.

Definition at line 140 of file eqcommoptionsurfacestripper.hpp.

|

private |

Definition at line 141 of file eqcommoptionsurfacestripper.hpp.

|

private |

Set to true if we must strip volatilities from prices.

Definition at line 144 of file eqcommoptionsurfacestripper.hpp.

|

private |

Store the function that will be called each time to solve for volatility.

Definition at line 147 of file eqcommoptionsurfacestripper.hpp.