Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <qle/termstructures/eqcommoptionsurfacestripper.hpp>

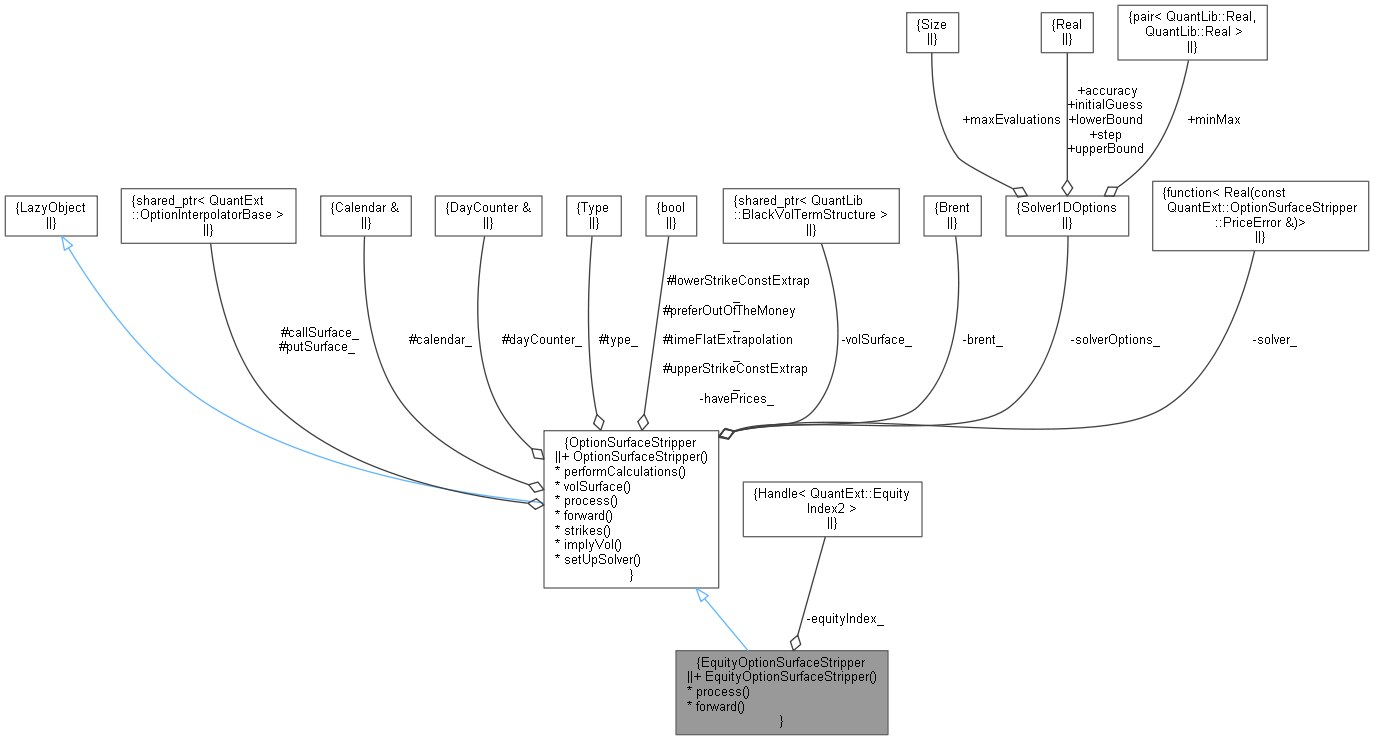

Inheritance diagram for EquityOptionSurfaceStripper: Collaboration diagram for EquityOptionSurfaceStripper:

Inheritance diagram for EquityOptionSurfaceStripper: Collaboration diagram for EquityOptionSurfaceStripper:Public Member Functions | |

| EquityOptionSurfaceStripper (const QuantLib::Handle< QuantExt::EquityIndex2 > &equityIndex, const QuantLib::ext::shared_ptr< OptionInterpolatorBase > &callSurface, const QuantLib::ext::shared_ptr< OptionInterpolatorBase > &putSurface, const QuantLib::Calendar &calendar, const QuantLib::DayCounter &dayCounter, QuantLib::Exercise::Type type=QuantLib::Exercise::European, bool lowerStrikeConstExtrap=true, bool upperStrikeConstExtrap=true, bool timeFlatExtrapolation=false, bool preferOutOfTheMoney=false, Solver1DOptions solverOptions={}) | |

| Public Member Functions inherited from OptionSurfaceStripper | |

| OptionSurfaceStripper (const QuantLib::ext::shared_ptr< OptionInterpolatorBase > &callSurface, const QuantLib::ext::shared_ptr< OptionInterpolatorBase > &putSurface, const QuantLib::Calendar &calendar, const QuantLib::DayCounter &dayCounter, QuantLib::Exercise::Type type=QuantLib::Exercise::European, bool lowerStrikeConstExtrap=true, bool upperStrikeConstExtrap=true, bool timeFlatExtrapolation=false, bool preferOutOfTheMoney=false, Solver1DOptions solverOptions={}) | |

| void | performCalculations () const override |

| QuantLib::ext::shared_ptr< QuantLib::BlackVolTermStructure > | volSurface () |

| Return the stripped volatility structure. More... | |

OptionSurfaceStripper interface | |

| QuantLib::Handle< QuantExt::EquityIndex2 > | equityIndex_ |

| QuantLib::ext::shared_ptr< QuantLib::GeneralizedBlackScholesProcess > | process (const QuantLib::ext::shared_ptr< QuantLib::SimpleQuote > &volatilityQuote) const override |

| Generate the relevant Black Scholes process for the underlying. More... | |

| QuantLib::Real | forward (const QuantLib::Date &date) const override |

| Return the forward price at a given date. More... | |

Additional Inherited Members | |

| Protected Member Functions inherited from OptionSurfaceStripper | |

| Protected Attributes inherited from OptionSurfaceStripper | |

| QuantLib::ext::shared_ptr< OptionInterpolatorBase > | callSurface_ |

| QuantLib::ext::shared_ptr< OptionInterpolatorBase > | putSurface_ |

| const QuantLib::Calendar & | calendar_ |

| const QuantLib::DayCounter & | dayCounter_ |

| QuantLib::Exercise::Type | type_ |

| bool | lowerStrikeConstExtrap_ |

| bool | upperStrikeConstExtrap_ |

| bool | timeFlatExtrapolation_ |

| bool | preferOutOfTheMoney_ |

Definition at line 150 of file eqcommoptionsurfacestripper.hpp.

| EquityOptionSurfaceStripper | ( | const QuantLib::Handle< QuantExt::EquityIndex2 > & | equityIndex, |

| const QuantLib::ext::shared_ptr< OptionInterpolatorBase > & | callSurface, | ||

| const QuantLib::ext::shared_ptr< OptionInterpolatorBase > & | putSurface, | ||

| const QuantLib::Calendar & | calendar, | ||

| const QuantLib::DayCounter & | dayCounter, | ||

| QuantLib::Exercise::Type | type = QuantLib::Exercise::European, |

||

| bool | lowerStrikeConstExtrap = true, |

||

| bool | upperStrikeConstExtrap = true, |

||

| bool | timeFlatExtrapolation = false, |

||

| bool | preferOutOfTheMoney = false, |

||

| Solver1DOptions | solverOptions = {} |

||

| ) |

Definition at line 312 of file eqcommoptionsurfacestripper.cpp.

|

overrideprotectedvirtual |

Generate the relevant Black Scholes process for the underlying.

Implements OptionSurfaceStripper.

Definition at line 329 of file eqcommoptionsurfacestripper.cpp.

|

overrideprotectedvirtual |

Return the forward price at a given date.

Implements OptionSurfaceStripper.

Definition at line 339 of file eqcommoptionsurfacestripper.cpp.

|

private |

Definition at line 175 of file eqcommoptionsurfacestripper.hpp.