Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

#include <orea/app/analytics/zerotoparshiftanalytic.hpp>

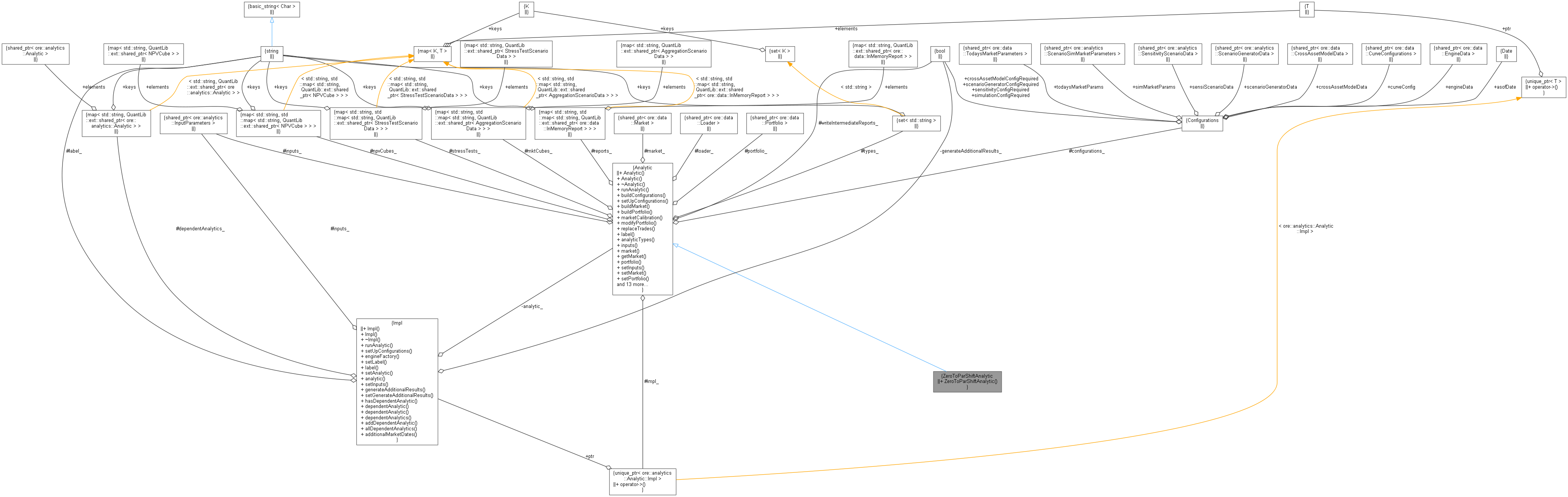

Inheritance diagram for ZeroToParShiftAnalytic: Collaboration diagram for ZeroToParShiftAnalytic:

Inheritance diagram for ZeroToParShiftAnalytic: Collaboration diagram for ZeroToParShiftAnalytic:Public Member Functions | |

| ZeroToParShiftAnalytic (const boost::shared_ptr< InputParameters > &inputs) | |

| Public Member Functions inherited from Analytic | |

| Analytic () | |

| Constructors. More... | |

| Analytic (std::unique_ptr< Impl > impl, const std::set< std::string > &analyticTypes, const QuantLib::ext::shared_ptr< InputParameters > &inputs, bool simulationConfig=false, bool sensitivityConfig=false, bool scenarioGeneratorConfig=false, bool crossAssetModelConfig=false) | |

| virtual | ~Analytic () |

| virtual void | runAnalytic (const QuantLib::ext::shared_ptr< ore::data::InMemoryLoader > &loader, const std::set< std::string > &runTypes={}) |

| Run only those analytic types that are inclcuded in the runTypes vector, run all if the runType vector is empty. More... | |

| virtual void | buildConfigurations (const bool=false) |

| virtual void | setUpConfigurations () |

| virtual void | buildMarket (const QuantLib::ext::shared_ptr< ore::data::InMemoryLoader > &loader, const bool marketRequired=true) |

| virtual void | buildPortfolio () |

| virtual void | marketCalibration (const QuantLib::ext::shared_ptr< MarketCalibrationReportBase > &mcr=nullptr) |

| virtual void | modifyPortfolio () |

| virtual void | replaceTrades () |

| const std::string | label () const |

| Inspectors. More... | |

| const std::set< std::string > & | analyticTypes () const |

| const QuantLib::ext::shared_ptr< InputParameters > & | inputs () const |

| const QuantLib::ext::shared_ptr< ore::data::Market > & | market () const |

| QuantLib::ext::shared_ptr< MarketImpl > | getMarket () const |

| const QuantLib::ext::shared_ptr< ore::data::Portfolio > & | portfolio () const |

| void | setInputs (const QuantLib::ext::shared_ptr< InputParameters > &inputs) |

| void | setMarket (const QuantLib::ext::shared_ptr< ore::data::Market > &market) |

| void | setPortfolio (const QuantLib::ext::shared_ptr< ore::data::Portfolio > &portfolio) |

| std::vector< QuantLib::ext::shared_ptr< ore::data::TodaysMarketParameters > > | todaysMarketParams () |

| const QuantLib::ext::shared_ptr< ore::data::Loader > & | loader () const |

| Configurations & | configurations () |

| analytic_reports & | reports () |

| Result reports. More... | |

| analytic_npvcubes & | npvCubes () |

| analytic_mktcubes & | mktCubes () |

| analytic_stresstests & | stressTests () |

| const bool | getWriteIntermediateReports () const |

| void | setWriteIntermediateReports (const bool flag) |

| bool | match (const std::set< std::string > &runTypes) |

| Check whether any of the requested run types is covered by this analytic. More... | |

| const std::unique_ptr< Impl > & | impl () |

| std::set< QuantLib::Date > | marketDates () const |

| std::vector< QuantLib::ext::shared_ptr< Analytic > > | allDependentAnalytics () const |

Additional Inherited Members | |

| Public Types inherited from Analytic | |

| typedef std::map< std::string, std::map< std::string, QuantLib::ext::shared_ptr< ore::data::InMemoryReport > > > | analytic_reports |

| typedef std::map< std::string, std::map< std::string, QuantLib::ext::shared_ptr< NPVCube > > > | analytic_npvcubes |

| typedef std::map< std::string, std::map< std::string, QuantLib::ext::shared_ptr< AggregationScenarioData > > > | analytic_mktcubes |

| typedef std::map< std::string, std::map< std::string, QuantLib::ext::shared_ptr< StressTestScenarioData > > > | analytic_stresstests |

| Protected Attributes inherited from Analytic | |

| std::unique_ptr< Impl > | impl_ |

| std::set< std::string > | types_ |

| list of analytic types run by this analytic More... | |

| QuantLib::ext::shared_ptr< InputParameters > | inputs_ |

| contains all the input parameters for the run More... | |

| Configurations | configurations_ |

| QuantLib::ext::shared_ptr< ore::data::Market > | market_ |

| QuantLib::ext::shared_ptr< ore::data::Loader > | loader_ |

| QuantLib::ext::shared_ptr< ore::data::Portfolio > | portfolio_ |

| analytic_reports | reports_ |

| analytic_npvcubes | npvCubes_ |

| analytic_mktcubes | mktCubes_ |

| analytic_stresstests | stressTests_ |

| bool | writeIntermediateReports_ = true |

Definition at line 43 of file zerotoparshiftanalytic.hpp.

| ZeroToParShiftAnalytic | ( | const boost::shared_ptr< InputParameters > & | inputs | ) |

Definition at line 109 of file zerotoparshiftanalytic.cpp.