#include <firstderivativeop.hpp>

Inheritance diagram for FirstDerivativeOp:

Inheritance diagram for FirstDerivativeOp: Collaboration diagram for FirstDerivativeOp:

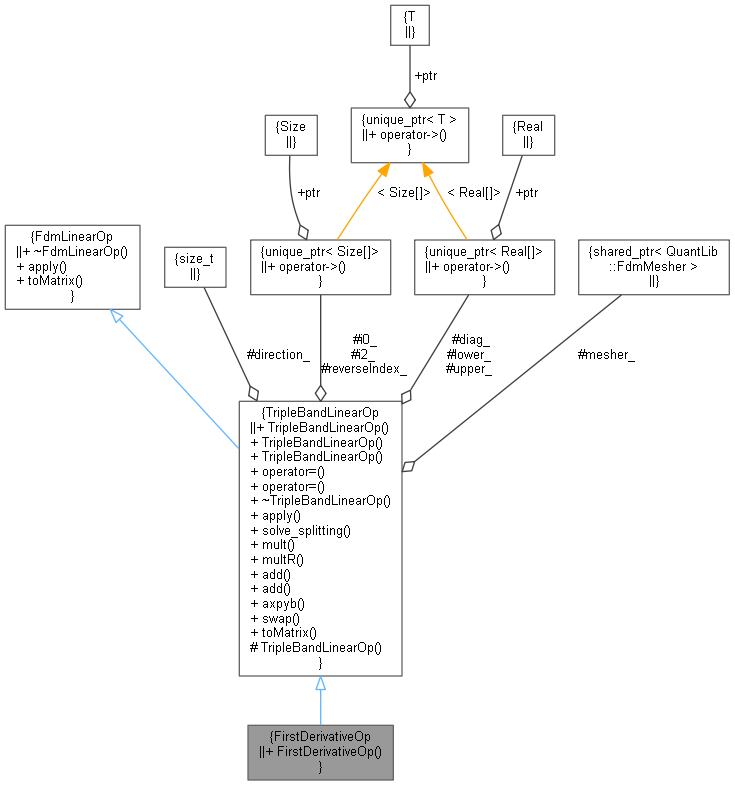

Collaboration diagram for FirstDerivativeOp:

Additional Inherited Members | |

| Public Types inherited from FdmLinearOp | |

| typedef Array | array_type |

| Protected Member Functions inherited from TripleBandLinearOp | |

| TripleBandLinearOp ()=default | |

| Protected Attributes inherited from TripleBandLinearOp | |

| Size | direction_ |

| std::unique_ptr< Size[]> | i0_ |

| std::unique_ptr< Size[]> | i2_ |

| std::unique_ptr< Size[]> | reverseIndex_ |

| std::unique_ptr< Real[]> | lower_ |

| std::unique_ptr< Real[]> | diag_ |

| std::unique_ptr< Real[]> | upper_ |

| ext::shared_ptr< FdmMesher > | mesher_ |

Detailed Description

Definition at line 33 of file firstderivativeop.hpp.

Constructor & Destructor Documentation

◆ FirstDerivativeOp()

| FirstDerivativeOp | ( | Size | direction, |

| const ext::shared_ptr< FdmMesher > & | mesher | ||

| ) |

Definition at line 28 of file firstderivativeop.cpp.